Academic Profile

Statistics

Similar Authors

Papers on arXiv

AIAltMed is a cutting-edge platform designed for drug discovery and repurposing. It utilizes Tanimoto similarity to identify structurally similar non-medicinal compounds to known medicinal ones. Thi...

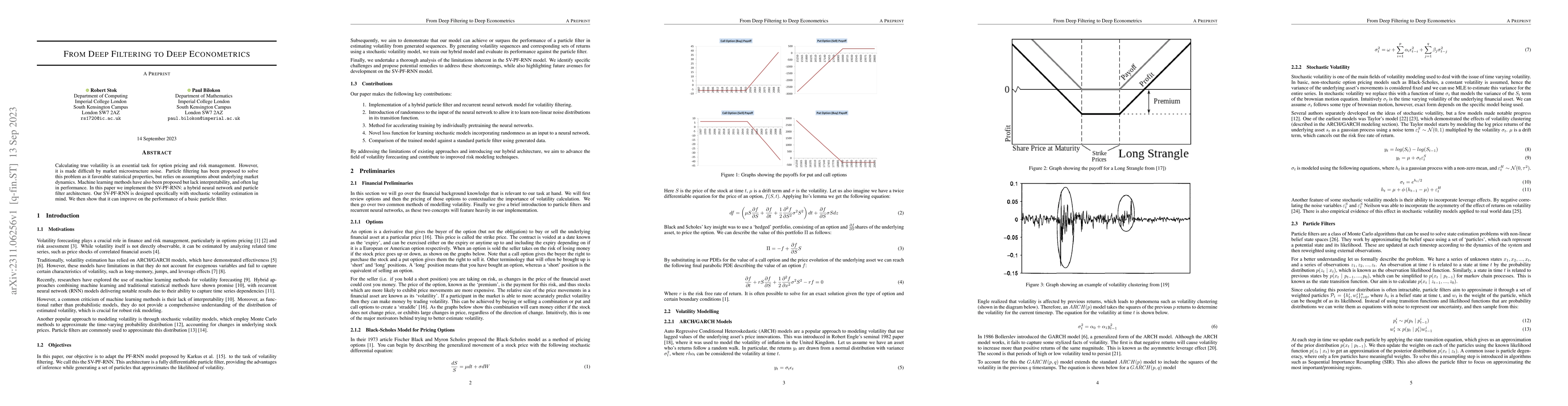

Calculating true volatility is an essential task for option pricing and risk management. However, it is made difficult by market microstructure noise. Particle filtering has been proposed to solve t...

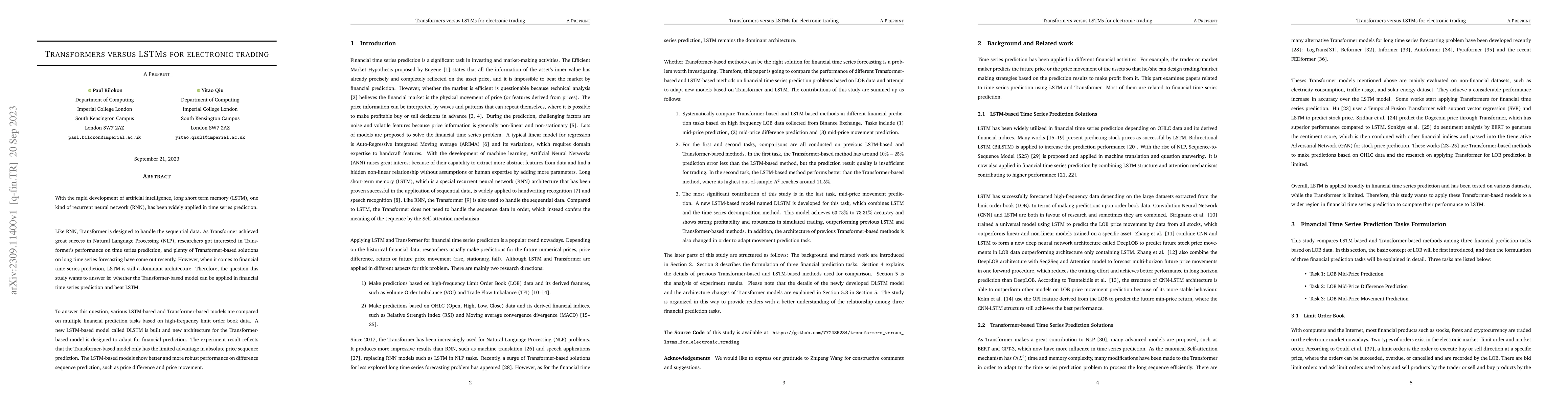

With the rapid development of artificial intelligence, long short term memory (LSTM), one kind of recurrent neural network (RNN), has been widely applied in time series prediction. Like RNN, Trans...

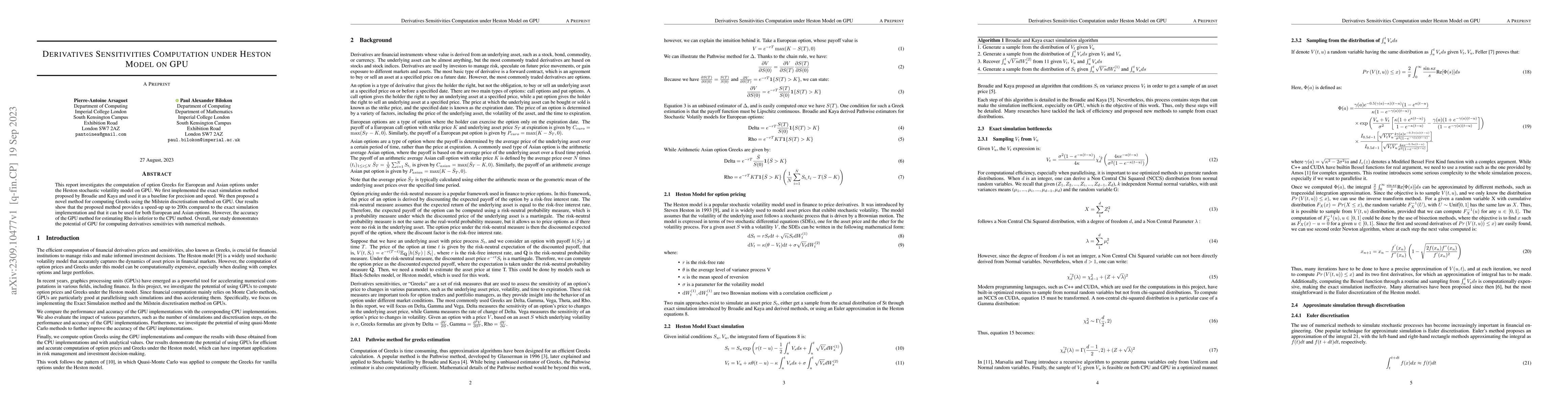

This report investigates the computation of option Greeks for European and Asian options under the Heston stochastic volatility model on GPU. We first implemented the exact simulation method propose...

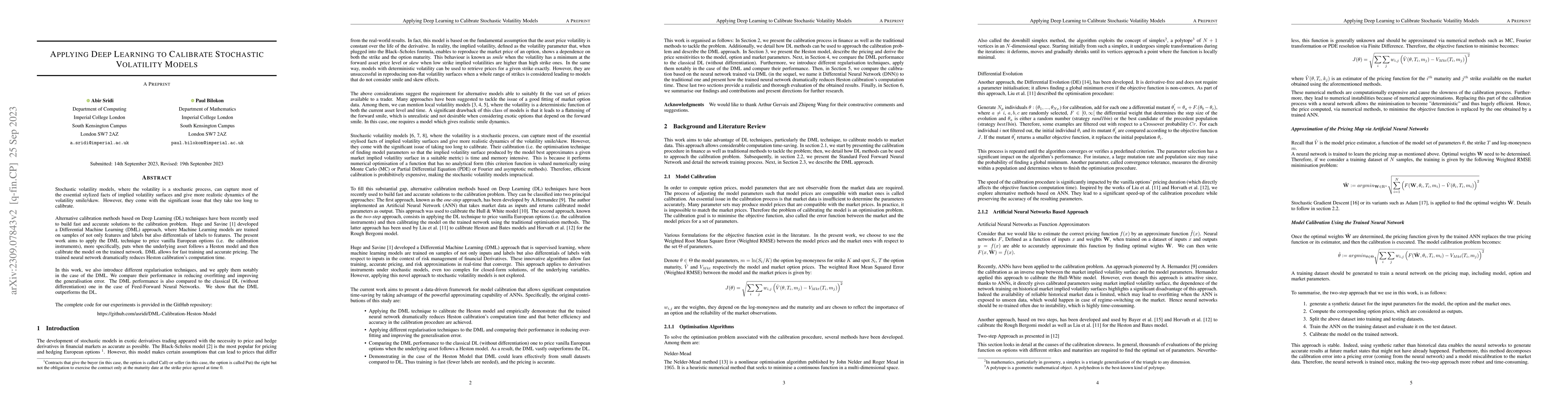

Stochastic volatility models, where the volatility is a stochastic process, can capture most of the essential stylized facts of implied volatility surfaces and give more realistic dynamics of the vo...

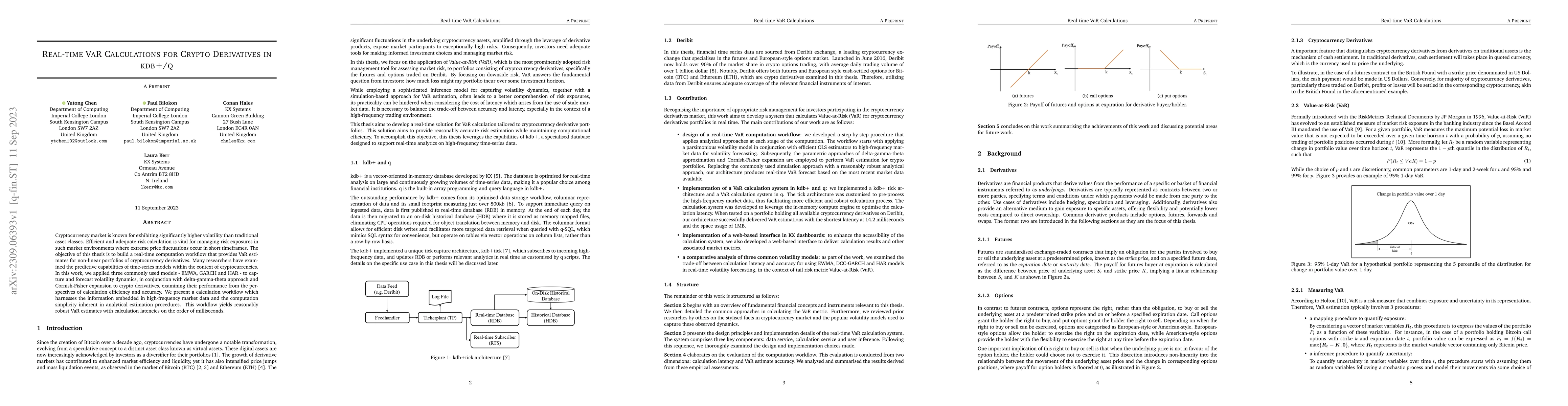

Cryptocurrency market is known for exhibiting significantly higher volatility than traditional asset classes. Efficient and adequate risk calculation is vital for managing risk exposures in such mar...

Recent advances in data science, machine learning, and artificial intelligence, such as the emergence of large language models, are leading to an increasing demand for data that can be processed by ...

This work aims to bridge the existing knowledge gap in the optimisation of latency-critical code, specifically focusing on high-frequency trading (HFT) systems. The research culminates in three main...

This paper explores the novel deep learning Transformers architectures for high-frequency Bitcoin-USDT log-return forecasting and compares them to the traditional Long Short-Term Memory models. A hy...

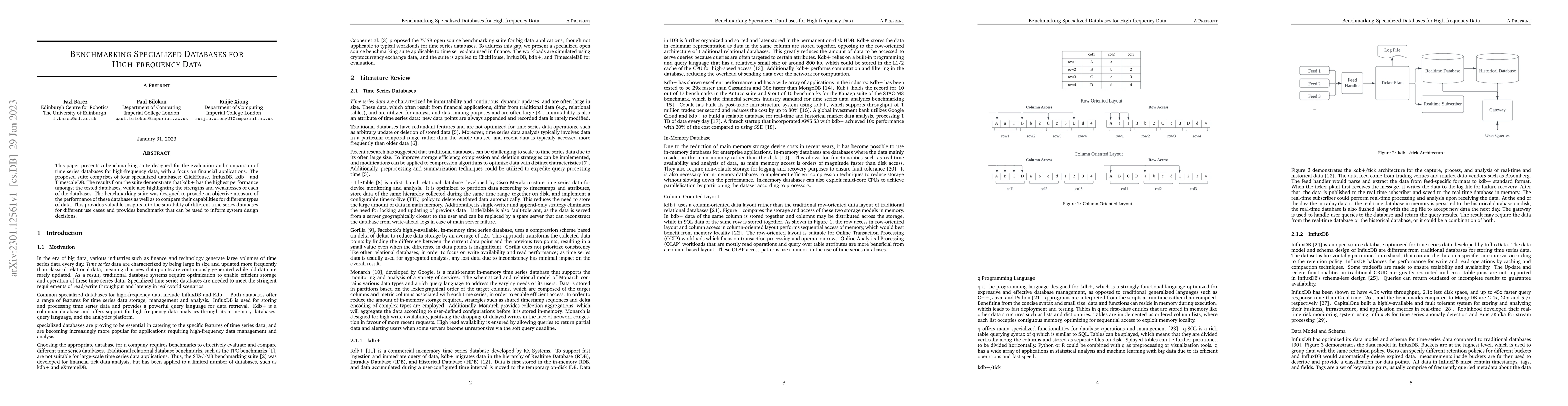

This paper presents a benchmarking suite designed for the evaluation and comparison of time series databases for high-frequency data, with a focus on financial applications. The proposed suite compr...

The calculation of option Greeks is vital for risk management. Traditional pathwise and finite-difference methods work poorly for higher-order Greeks and options with discontinuous payoff functions....

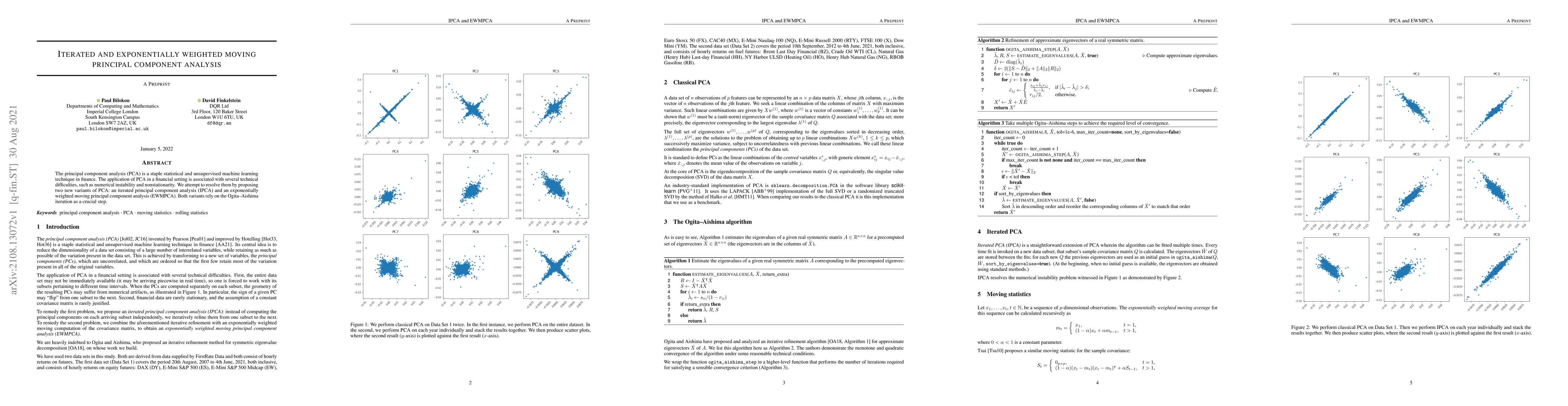

The principal component analysis (PCA) is a staple statistical and unsupervised machine learning technique in finance. The application of PCA in a financial setting is associated with several techni...

Drug repurposing provides an opportunity to redeploy drugs, which ideally are already approved for use in humans, for the treatment of other diseases. For example, the repurposing of dexamethasone a...

We provide a data-driven algorithm to classify market regimes for time series. We utilise the path signature, encoding time series into easy-to-describe objects, and provide a metric structure which...