01

MethodologyHow they did it

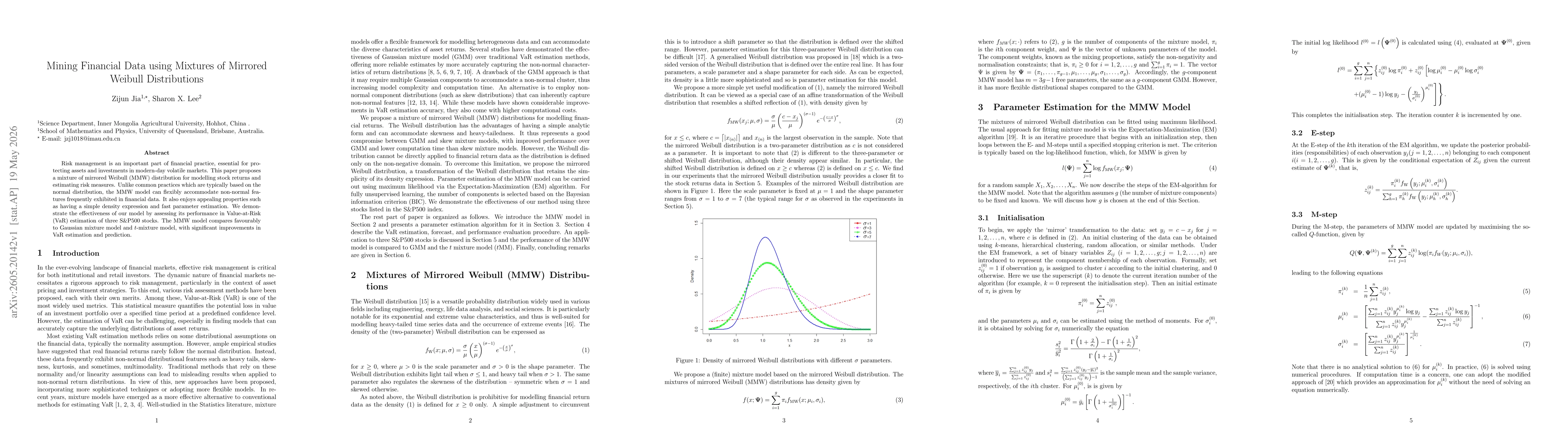

The paper introduces a mixture of mirrored Weibull (MMW) distributions to model stock returns, enabling skewness and heavy tails. Parameter estimation is performed via maximum likelihood using the EM algorithm, with component number selected by BIC for fully unsupervised learning. The approach is evaluated through VaR estimation on three S&P 500 stocks, comparing MMW to Gaussian mixture models and t-mixture models.

Discussion 0