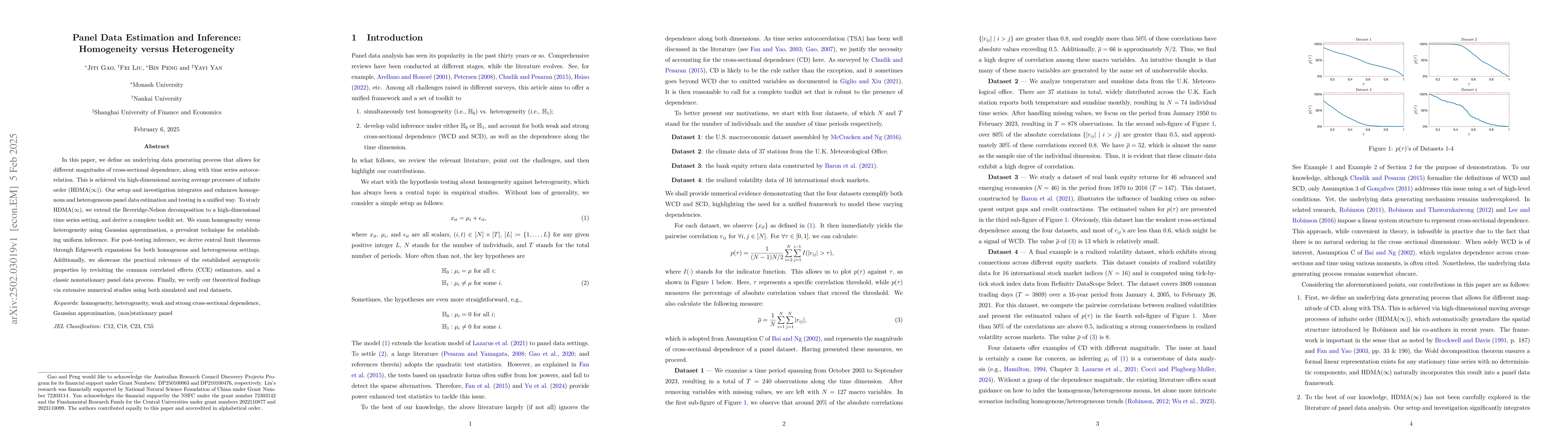

In this paper, we define an underlying data generating process that allows

for different magnitudes of cross-sectional dependence, along with time series

autocorrelation. This is achieved via high-dimensional moving average processes

of infinite order (HDMA($\infty$)). Our setup and investigation integrates and

enhances homogenous and heterogeneous panel data estimation and testing in a

unified way. To study HDMA($\infty$), we extend the Beveridge-Nelson

decomposition to a high-dimensional time series setting, and derive a complete

toolkit set. We exam homogeneity versus heterogeneity using Gaussian

approximation, a prevalent technique for establishing uniform inference. For

post-testing inference, we derive central limit theorems through Edgeworth

expansions for both homogenous and heterogeneous settings. Additionally, we

showcase the practical relevance of the established asymptotic properties by

revisiting the common correlated effects (CCE) estimators, and a classic

nonstationary panel data process. Finally, we verify our theoretical findings

via extensive numerical studies using both simulated and real datasets.

Discussion 0