Academic Profile

Statistics

Similar Authors

Papers on arXiv

In this paper, we propose an easy-to-implement residual-based specification testing procedure for detecting structural changes in factor models, which is powerful against both smooth and abrupt stru...

In this paper, we propose a robust estimation and inferential method for high-dimensional panel data models. Specifically, (1) we investigate the case where the number of regressors can grow faster ...

In this paper, we consider estimation and inference for the unknown parameters and function involved in a class of generalized hierarchical models. Such models are of great interest in the literatur...

This paper considers a time-varying vector error-correction model that allows for different time series behaviours (e.g., unit-root and locally stationary processes) to interact with each other to c...

In this paper, we consider a wide class of time-varying multivariate causal processes which nests many classic and new examples as special cases. We first prove the existence of a weakly dependent s...

In this paper, we propose a simple inferential method for a wide class of panel data models with a focus on such cases that have both serial correlation and cross-sectional dependence. In order to e...

Vector autoregressive (VAR) models are widely used in practical studies, e.g., forecasting, modelling policy transmission mechanism, and measuring connection of economic agents. To better capture th...

In this paper, we investigate binary response models for heterogeneous panel data with interactive fixed effects by allowing both the cross-sectional dimension and the temporal dimension to diverge....

Multivariate dynamic time series models are widely encountered in practical studies, e.g., modelling policy transmission mechanism and measuring connectedness between economic agents. To better capt...

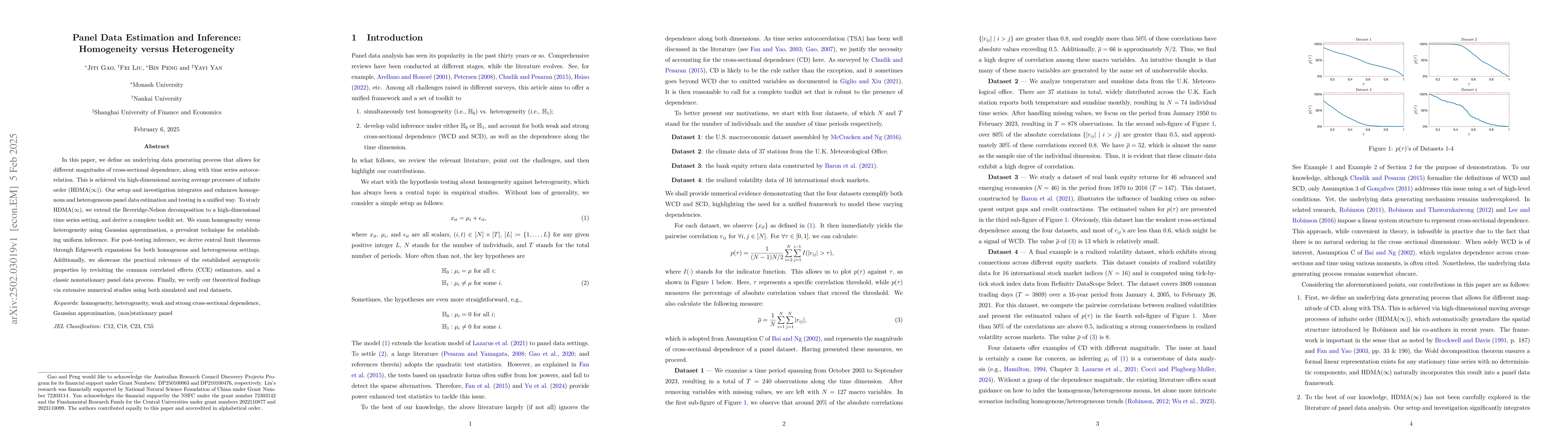

In this paper, we define an underlying data generating process that allows for different magnitudes of cross-sectional dependence, along with time series autocorrelation. This is achieved via high-dim...

In this paper, we consider the nonstationary matrix-valued time series with common stochastic trends. Unlike the traditional factor analysis which flattens matrix observations into vectors, we adopt a...