01

MethodologyHow they did it

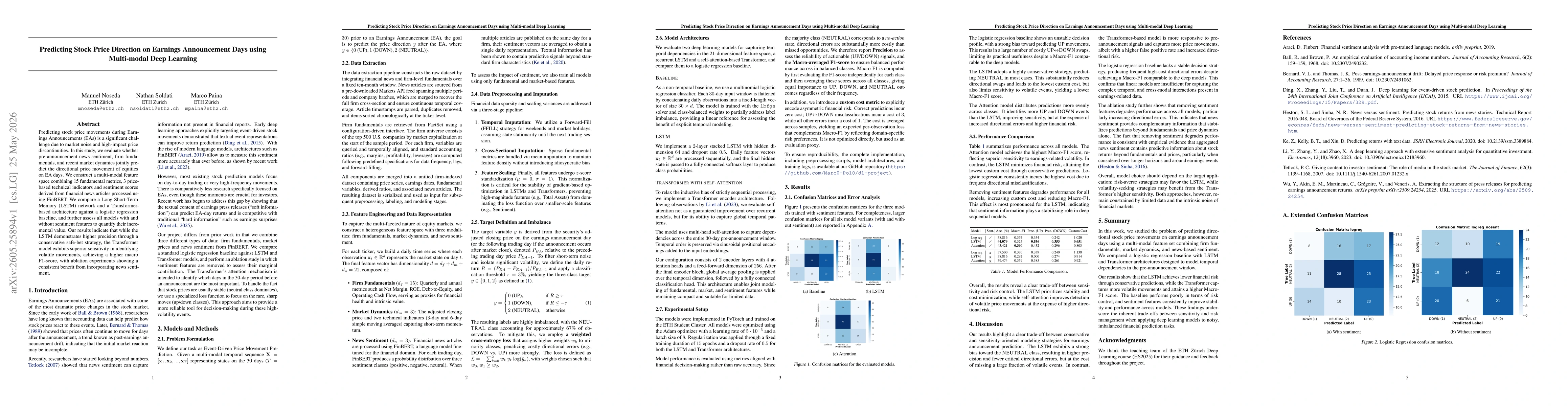

The study constructs a multi-modal feature space combining 15 firm fundamentals, 3 market dynamics indicators, and 3 sentiment features from FinBERT, applied to 30-day pre-EA sequences. Models compared include Logistic Regression, LSTM, and Transformer architectures, with and without sentiment features, using specialized loss to address class imbalance and a forward-fill/cross-sectional imputation pipeline for preprocessing.

Discussion 0