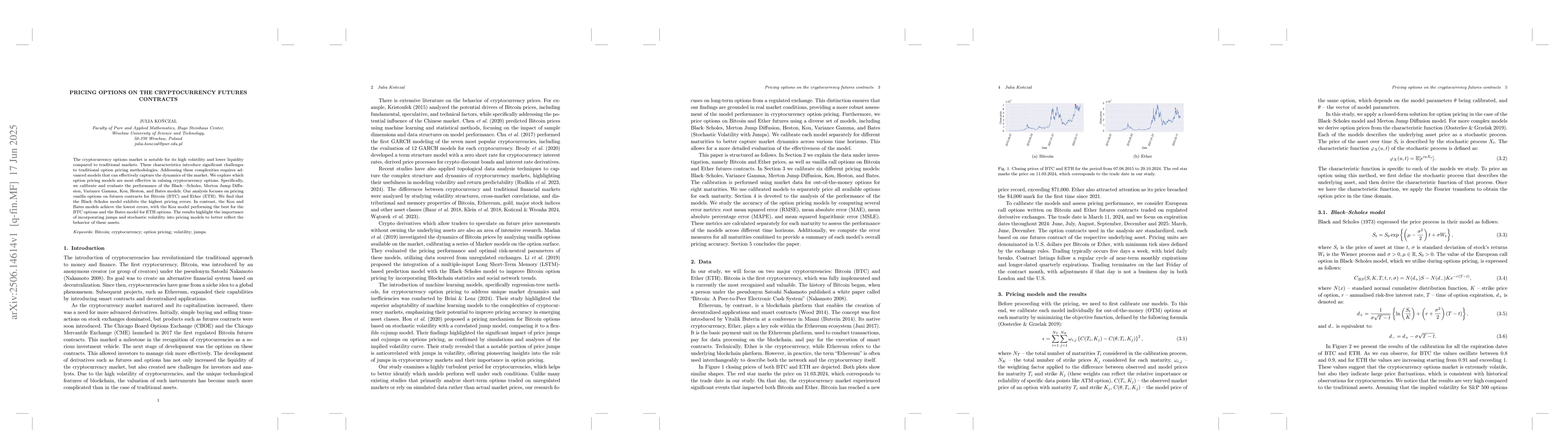

The cryptocurrency options market is notable for its high volatility and

lower liquidity compared to traditional markets. These characteristics

introduce significant challenges to traditional option pricing methodologies.

Addressing these complexities requires advanced models that can effectively

capture the dynamics of the market. We explore which option pricing models are

most effective in valuing cryptocurrency options. Specifically, we calibrate

and evaluate the performance of the Black-Scholes, Merton Jump Diffusion,

Variance Gamma, Kou, Heston, and Bates models. Our analysis focuses on pricing

vanilla options on futures contracts for Bitcoin (BTC) and Ether (ETH). We find

that the Black-Scholes model exhibits the highest pricing errors. In contrast,

the Kou and Bates models achieve the lowest errors, with the Kou model

performing the best for the BTC options and the Bates model for ETH options.

The results highlight the importance of incorporating jumps and stochastic

volatility into pricing models to better reflect the behavior of these assets.

Discussion 0