01

MethodologyHow they did it

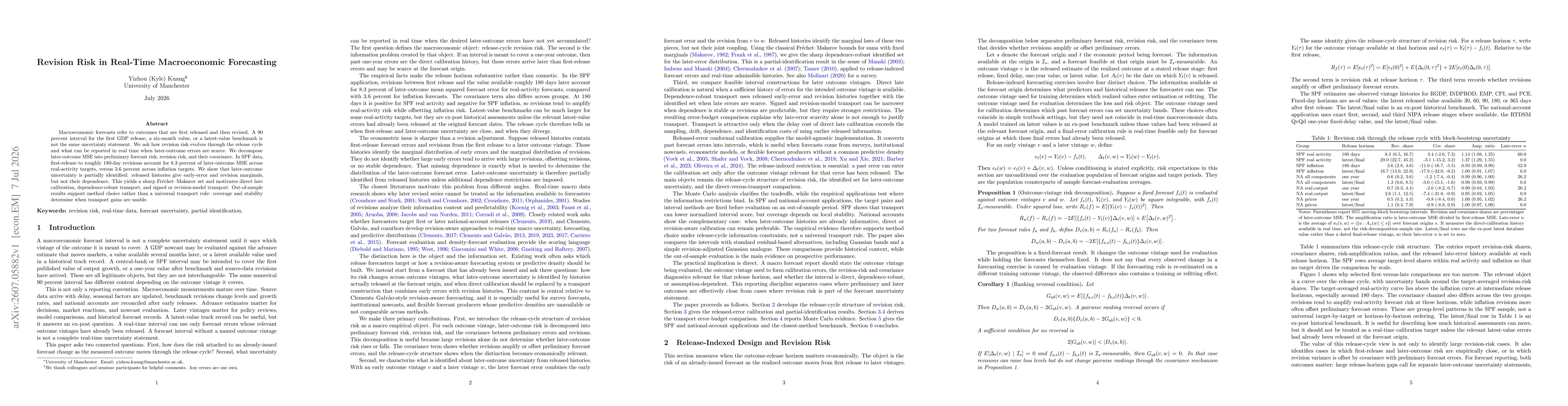

The paper decomposes later-outcome MSE into preliminary forecast risk, revision risk, and their covariance for each outcome vintage, using released histories to identify marginal distributions of early errors and revisions while noting the dependence is not identified; it then derives a sharp Frechet–Makarov set to bound later-outcome uncertainty and explores dependence-robust transport and calibration strategies.

Discussion 0