Authors

Publication

Metrics

Quick Actions

Quick Answers

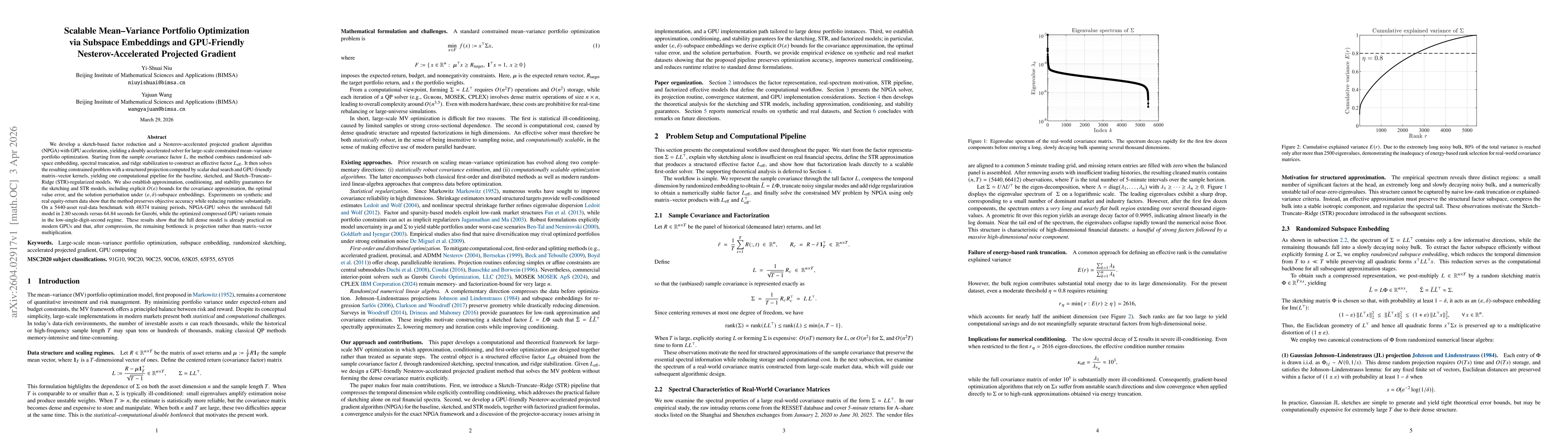

What methodology did the authors use?

The study develops a sketch‑based factor reduction combined with a Nesterov‑accelerated projected gradient algorithm (NPGA) that is GPU‑friendly. It uses randomized subspace embeddings, spectral truncation, and ridge stabilization to build an effective factor L_eff, then solves the constrained mean‑variance problem with a structured projection via scalar dual search and GPU‑optimized matrix‑vector kernels. More in Methodology →

What are the key results?

NPGA‑GPU solves a 5440‑asset full model in 2.80 s versus 64.84 s for Gurobi, while compressed GPU variants run in low‑single‑digit seconds. — Sketching and truncation provide a controllable accuracy‑conditioning trade‑off; moderate sketches keep objective gaps below a few percent and ridge regularization stabilizes low‑rank surrogates. More in Key Results →

Why is this work significant?

This work demonstrates that large‑scale mean‑variance portfolio optimization can be performed efficiently on GPUs with provable accuracy guarantees, making dense quadratic programming tractable for thousands of assets and opening the door to real‑time portfolio management. More in Significance →

What are the main limitations?

After compression the projection operation becomes the computational bottleneck, limiting further GPU speed‑ups. — The framework has been evaluated mainly on dense covariance matrices; performance on sparse or multi‑factor models remains to be explored. More in Limitations →

Paper Preview

Abstract

We develop a sketch-based factor reduction and a Nesterov-accelerated projected gradient algorithm (NPGA) with GPU acceleration, yielding a doubly accelerated solver for large-scale constrained mean-variance portfolio optimization. Starting from the sample covariance factor $L$, the method combines randomized subspace embedding, spectral truncation, and ridge stabilization to construct an effective factor $L_{eff}$. It then solves the resulting constrained problem with a structured projection computed by scalar dual search and GPU-friendly matrix-vector kernels, yielding one computational pipeline for the baseline, sketched, and Sketch-Truncate-Ridge (STR)-regularized models. We also establish approximation, conditioning, and stability guarantees for the sketching and STR models, including explicit $O(\varepsilon)$ bounds for the covariance approximation, the optimal value error, and the solution perturbation under $(\varepsilon,δ)$-subspace embeddings. Experiments on synthetic and real equity-return data show that the method preserves objective accuracy while reducing runtime substantially. On a 5440-asset real-data benchmark with 48374 training periods, NPGA-GPU solves the unreduced full model in 2.80 seconds versus 64.84 seconds for Gurobi, while the optimized compressed GPU variants remain in the low-single-digit-second regime. These results show that the full dense model is already practical on modern GPUs and that, after compression, the remaining bottleneck is projection rather than matrix-vector multiplication.

AI Key Findings

Generated Apr 06, 2026

Methodology — What approach did the authors take?

The study develops a sketch‑based factor reduction combined with a Nesterov‑accelerated projected gradient algorithm (NPGA) that is GPU‑friendly. It uses randomized subspace embeddings, spectral truncation, and ridge stabilization to build an effective factor L_eff, then solves the constrained mean‑variance problem with a structured projection via scalar dual search and GPU‑optimized matrix‑vector kernels.

Key Results — What are the main findings?

- NPGA‑GPU solves a 5440‑asset full model in 2.80 s versus 64.84 s for Gurobi, while compressed GPU variants run in low‑single‑digit seconds.

- Sketching and truncation provide a controllable accuracy‑conditioning trade‑off; moderate sketches keep objective gaps below a few percent and ridge regularization stabilizes low‑rank surrogates.

- Theoretical analysis yields O(ε) bounds for covariance approximation, optimal value error, and solution perturbation under (ε,δ)‑subspace embeddings, and shows conditioning improvement via STR.

- Experiments on synthetic and real 5‑minute Chinese A‑share data confirm that the full dense model is practical on modern GPUs and that after compression the projection step dominates runtime.

Significance — Why does this research matter?

This work demonstrates that large‑scale mean‑variance portfolio optimization can be performed efficiently on GPUs with provable accuracy guarantees, making dense quadratic programming tractable for thousands of assets and opening the door to real‑time portfolio management.

Technical Contribution — What is the technical contribution?

A unified, scalable pipeline that integrates subspace embeddings, L‑z factorization, and a Nesterov‑accelerated projected gradient solver with explicit smoothness and curvature constants derived from the factor representation, providing O(ε) approximation, conditioning, and stability guarantees for sketching and STR models.

Novelty — What is new about this work?

First to combine sketch‑based factor reduction, ridge‑regularized truncation, and GPU‑friendly accelerated projected gradient into a single, provably accurate solver, and to demonstrate its practical feasibility on a 5440‑asset real‑world dataset.

Limitations — What are the limitations of this study?

- After compression the projection operation becomes the computational bottleneck, limiting further GPU speed‑ups.

- The framework has been evaluated mainly on dense covariance matrices; performance on sparse or multi‑factor models remains to be explored.

Future Work — What did the authors propose for future work?

- Design stronger GPU projection kernels and reduce synchronization overhead to fully exploit GPU acceleration.

- Extend the framework to multi‑factor or sparse portfolio models, online/streaming settings, and dynamic state‑estimation frameworks such as Yau–Yau filtering.

Paper Details

How to Cite This Paper

@article{wang2026scalable,

title = {Scalable Mean-Variance Portfolio Optimization via Subspace Embeddings and GPU-Friendly Nesterov-Accelerated Projected Gradient},

author = {Wang, Yajuan and Niu, Yi-Shuai},

year = {2026},

eprint = {2604.02917},

archivePrefix = {arXiv},

primaryClass = {math.OC},

}Wang, Y., & Niu, Y. (2026). Scalable Mean-Variance Portfolio Optimization via Subspace Embeddings and GPU-Friendly Nesterov-Accelerated Projected Gradient. arXiv. https://arxiv.org/abs/2604.02917Wang, Yajuan, and Yi-Shuai Niu. "Scalable Mean-Variance Portfolio Optimization via Subspace Embeddings and GPU-Friendly Nesterov-Accelerated Projected Gradient." arXiv, 2026, arxiv.org/abs/2604.02917.PDF Preview

Similar Papers

Found 4 papersRandomized Subspace Nesterov Accelerated Gradient

Gaku Omiya, Pierre-Louis Poirion, Akiko Takeda

Nesterov Accelerated Shuffling Gradient Method for Convex Optimization

Lam M. Nguyen, Trang H. Tran, Katya Scheinberg

A Scalable Gradient-Based Optimization Framework for Sparse Minimum-Variance Portfolio Selection

Sarat Moka, Matias Quiroz, Vali Asimit et al.

FlashFolio: A GPU-Accelerated Solver for Portfolio Optimization

Yilun Jiang, Haihao Lu, Zedong Peng et al.

Comments (0)