Solving The Dynamic Volatility Fitting Problem: A Deep Reinforcement Learning Approach

Publication

Metrics

AI Quick Summary

This research proposes using Deep Reinforcement Learning (DRL) to solve the dynamic volatility fitting problem in equity derivatives, demonstrating that DDPG and SAC variants perform at least as well as traditional methods, while offering superior adaptability to market shifts and complex objective functions.

Paper Preview

Abstract

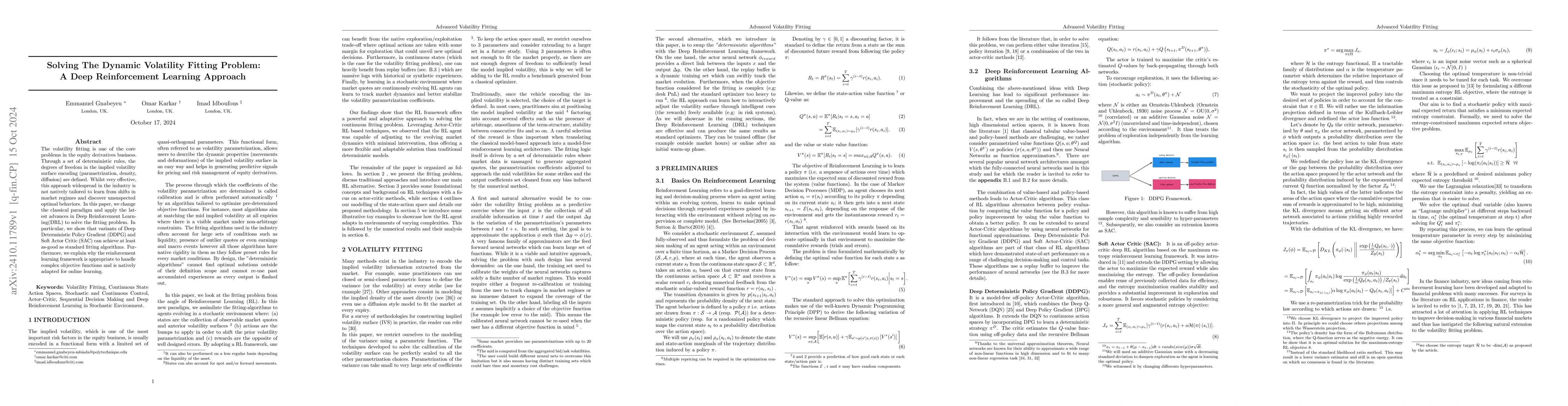

The volatility fitting is one of the core problems in the equity derivatives business. Through a set of deterministic rules, the degrees of freedom in the implied volatility surface encoding (parametrization, density, diffusion) are defined. Whilst very effective, this approach widespread in the industry is not natively tailored to learn from shifts in market regimes and discover unsuspected optimal behaviors. In this paper, we change the classical paradigm and apply the latest advances in Deep Reinforcement Learning(DRL) to solve the fitting problem. In particular, we show that variants of Deep Deterministic Policy Gradient (DDPG) and Soft Actor Critic (SAC) can achieve at least as good as standard fitting algorithms. Furthermore, we explain why the reinforcement learning framework is appropriate to handle complex objective functions and is natively adapted for online learning.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Impact

Paper Details

Authors

PDF Preview

Citation Network

Current paper (gray), citations (green), references (blue)

Display is limited for performance on very large graphs.

Discussion 0