Sparse Portfolio Selection via Non-convex Fraction Function

Publication

Metrics

AI Quick Summary

This paper proposes a non-convex promoting sparsity fraction function for sparse portfolio selection models, with and without short-selling constraints. It develops an iterative fraction penalty thresholding algorithm (IFPT) and proves the limitations on the regularization parameter $\lambda$. Empirical results indicate effective performance in identifying sparse portfolio weights.

Paper Preview

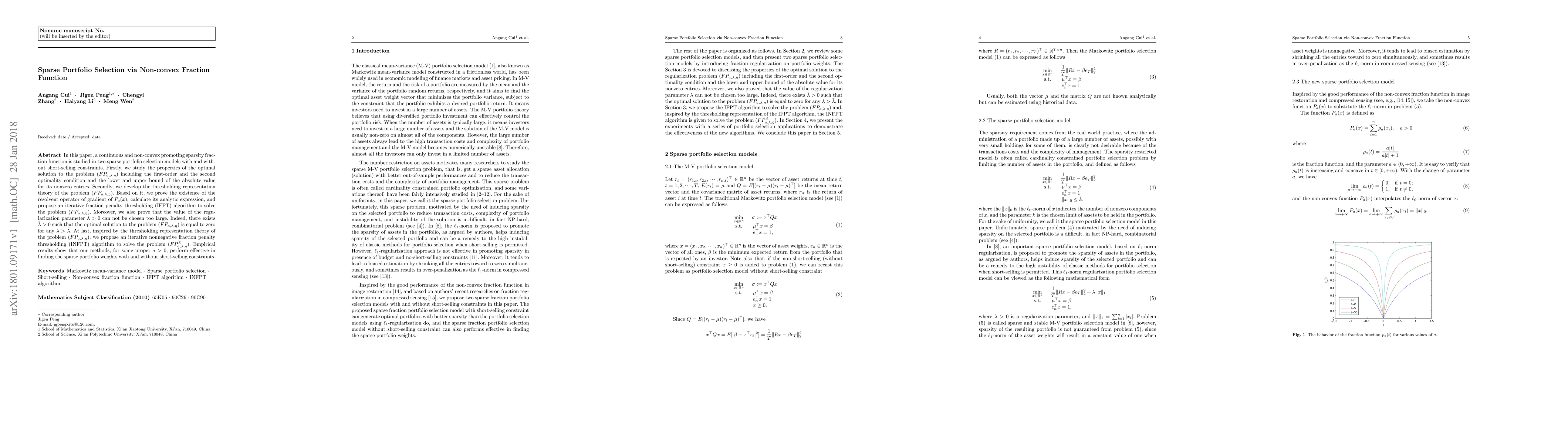

Abstract

In this paper, a continuous and non-convex promoting sparsity fraction function is studied in two sparse portfolio selection models with and without short-selling constraints. Firstly, we study the properties of the optimal solution to the problem $(FP_{a,\lambda,\eta})$ including the first-order and the second optimality condition and the lower and upper bound of the absolute value for its nonzero entries. Secondly, we develop the thresholding representation theory of the problem $(FP_{a,\lambda,\eta})$. Based on it, we prove the existence of the resolvent operator of gradient of $P_{a}(x)$, calculate its analytic expression, and propose an iterative fraction penalty thresholding (IFPT) algorithm to solve the problem $(FP_{a,\lambda,\eta})$. Moreover, we also prove that the value of the regularization parameter $\lambda>0$ can not be chosen too large. Indeed, there exists $\bar{\lambda}>0$ such that the optimal solution to the problem $(FP_{a,\lambda,\eta})$ is equal to zero for any $\lambda>\bar{\lambda}$. At last, inspired by the thresholding representation theory of the problem $(FP_{a,\lambda,\eta})$, we propose an iterative nonnegative fraction penalty thresholding (INFPT) algorithm to solve the problem $(FP_{a,\lambda,\eta}^{\geq})$. Empirical results show that our methods, for some proper $a>0$, perform effective in finding the sparse portfolio weights with and without short-selling constraints.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Impact

Paper Details

PDF Preview

Key Terms

Citation Network

Current paper (gray), citations (green), references (blue)

Display is limited for performance on very large graphs.

Discussion 0