Publication

Metrics

Quick Actions

AI Quick Summary

This paper explores block diagonal and hierarchical nested stochastic multivariate Gaussian models through high-dimensional sample cross-correlation matrices, comparing rotationally invariant and hierarchical clustering estimators. It concludes that hierarchical clustering estimators often outperform rotationally invariant estimators for large sample sizes, and the best results for block and nested block models come from two-step estimators combining shrinkage models with hierarchical clustering techniques.

Paper Preview

Abstract

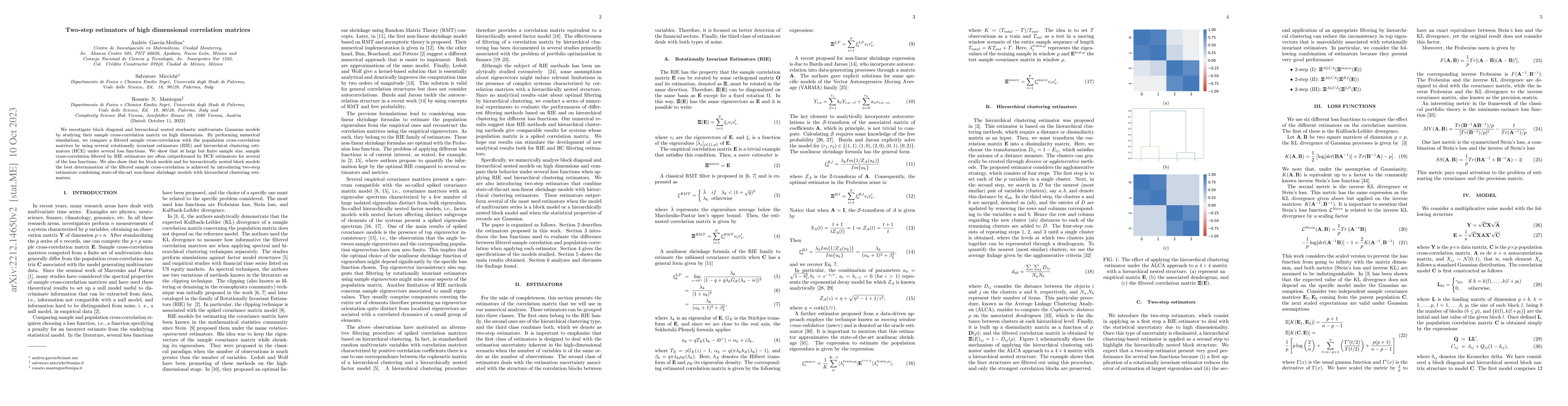

We investigate block diagonal and hierarchical nested stochastic multivariate Gaussian models by studying their sample cross-correlation matrix on high dimensions. By performing numerical simulations, we compare a filtered sample cross-correlation with the population cross-correlation matrices by using several rotationally invariant estimators (RIE) and hierarchical clustering estimators (HCE) under several loss functions. We show that at large but finite sample size, sample cross-correlation filtered by RIE estimators are often outperformed by HCE estimators for several of the loss functions. We also show that for block models and for hierarchically nested block models the best determination of the filtered sample cross-correlation is achieved by introducing two-step estimators combining state-of-the-art non-linear shrinkage models with hierarchical clustering estimators.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, and significance.

Paper Details

How to Cite This Paper

@article{garcíamedina2024two,

title = {Two-step estimators of high dimensional correlation matrices},

author = {García-Medina, Andrés and Mantegna, Rosario N. and Miccichè, Salvatore},

year = {2024},

eprint = {2212.14650},

archivePrefix = {arXiv},

primaryClass = {stat.ME},

doi = {10.1103/PhysRevE.108.044137},

}García-Medina, A., Mantegna, R., & Miccichè, S. (2024). Two-step estimators of high dimensional correlation matrices. arXiv. https://doi.org/10.1103/PhysRevE.108.044137García-Medina, Andrés, et al. "Two-step estimators of high dimensional correlation matrices." arXiv, 2024, doi.org/10.1103/PhysRevE.108.044137.PDF Preview

Key Terms

Citation Network

Current paper (gray), citations (green), references (blue)

Display is limited for performance on very large graphs.

Similar Papers

Found 4 papersSpectral properties of high dimensional rescaled sample correlation matrices

Weijiang Chen, Shurong Zheng, Tingting Zou

No citations found for this paper.

Comments (0)