Publication

Metrics

Paper Preview

Abstract

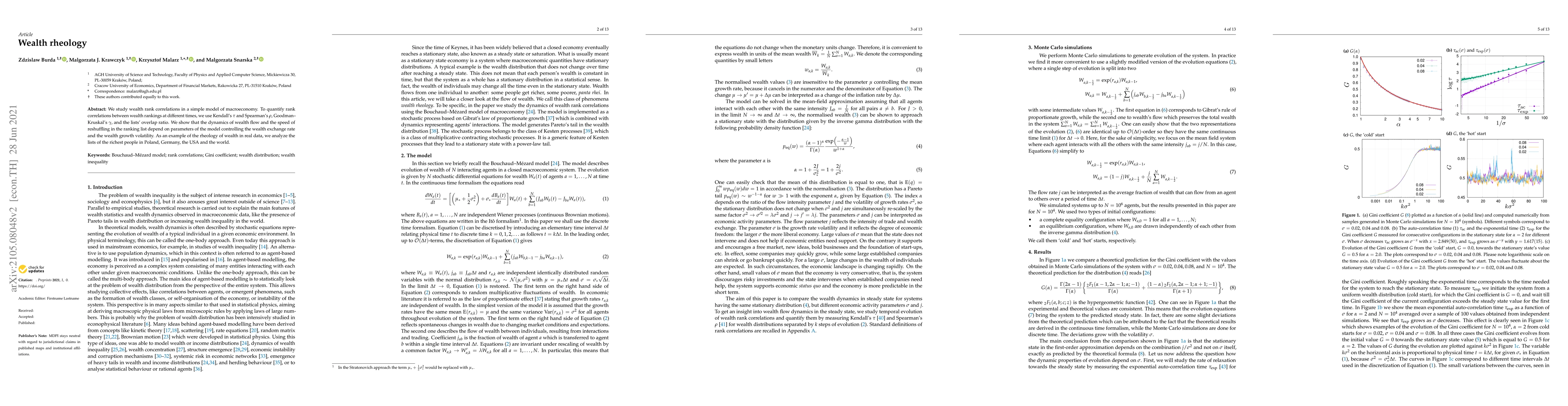

We study wealth rank correlations in a simple model of macro-economy. To quantify rank correlations between wealth rankings at different times, we use Kendall's $\tau$ and Spearman's $\rho$, Goodman--Kruskal's $\gamma$, and the lists' overlap ratio. We show that the dynamics of wealth flow and the speed of reshuffling in the ranking list depend on parameters of the model controlling the wealth exchange rate and the wealth growth volatility. As an example of the rheology of wealth in real data, we analyze the lists of the richest people in Poland, Germany, the USA and the world.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Impact

Paper Details

Authors

PDF Preview

Key Terms

Citation Network

Current paper (gray), citations (green), references (blue)

Display is limited for performance on very large graphs.

Discussion 0