Academic Profile

Statistics

Similar Authors

Papers on arXiv

We develop a fast variational approximation scheme for Gaussian process (GP) regression, where the spectrum of the covariance function is subjected to a sparse approximation. Our approach enables un...

In this paper we consider the filtering problem associated to partially observed McKean-Vlasov stochastic differential equations (SDEs). The model consists of data that are observed at regular and d...

In this paper, we present a new antithetic multilevel Monte Carlo (MLMC) method for the estimation of expectations with respect to laws of diffusion processes that can be elliptic or hypo-elliptic. ...

In this article we consider the filtering problem associated to partially observed diffusions, with observations following a marked point process. In the model, the data form a point process with ob...

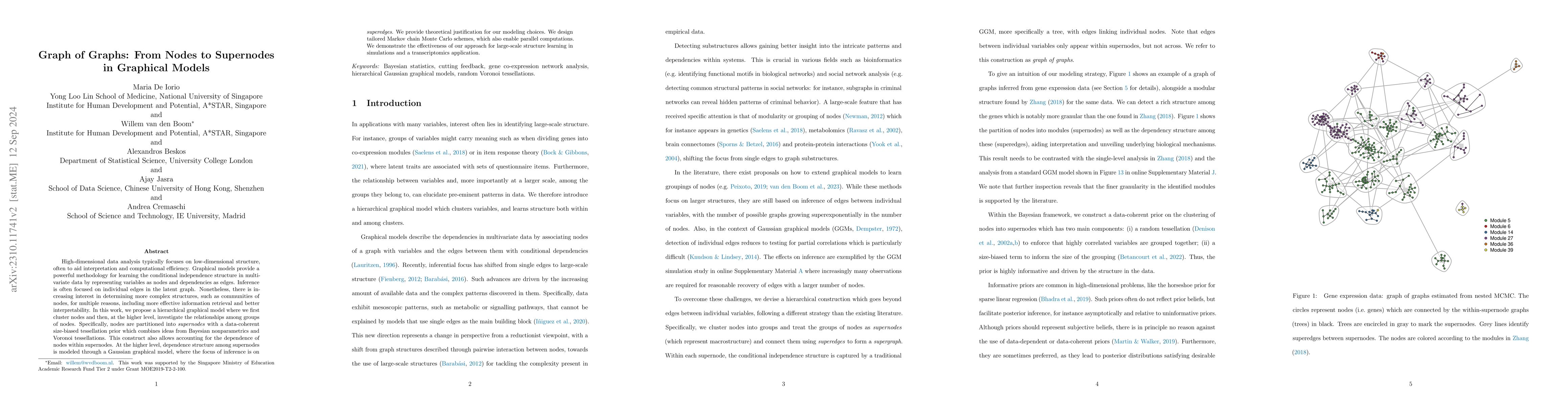

High-dimensional data analysis typically focuses on low-dimensional structure, often to aid interpretation and computational efficiency. Graphical models provide a powerful methodology for learning ...

In this paper we consider Bayesian parameter inference associated to a class of partially observed stochastic differential equations (SDE) driven by jump processes. Such type of models can be routin...

We consider the long time behavior of Wong-Zakai approximations of stochastic differential equations. These piecewise smooth diffusion approximations are of great importance in many areas, such as t...

In this article we consider Bayesian parameter inference for a type of partially observed stochastic Volterra equation (SVE). SVEs are found in many areas such as physics and mathematical finance. I...

We consider the problem of Bayesian estimation of static parameters associated to a partially and discretely observed diffusion process. We assume that the exact transition dynamics of the diffusion...

In this article we consider the estimation of static parameters for partially observed diffusion process with discrete-time observations over a fixed time interval. In particular, we assume that one...

In this paper we consider the filtering of a class of partially observed piecewise deterministic Markov processes (PDMPs). In particular, we assume that an ordinary differential equation (ODE) drive...

We consider a class of high-dimensional spatial filtering problems, where the spatial locations of observations are unknown and driven by the partially observed hidden signal. This problem is except...

In this paper we consider the filtering of partially observed multi-dimensional diffusion processes that are observed regularly at discrete times. We assume that, for numerical reasons, one has to t...

In this paper we consider the filtering of partially observed multi-dimensional diffusion processes that are observed regularly at discrete times. This is a challenging problem which requires the us...

In this paper we consider Bayesian parameter inference for partially observed fractional Brownian motion (fBM) models. The approach we follow is to time-discretize the hidden process and then to des...

In this article we consider the development of an unbiased estimator for the ensemble Kalman--Bucy filter (EnKBF). The EnKBF is a continuous-time filtering methodology which can be viewed as a conti...

In this work we consider the unbiased estimation of expectations w.r.t.~probability measures that have non-negative Lebesgue density, and which are known point-wise up-to a normalizing constant. We ...

In this article we consider Bayesian inference associated to deep neural networks (DNNs) and in particular, trace-class neural network (TNN) priors which were proposed by Sell et al. [39]. Such prio...

We consider the problem of estimating expectations with respect to a target distribution with an unknown normalizing constant, and where even the unnormalized target needs to be approximated at fini...

When implementing Markov Chain Monte Carlo (MCMC) algorithms, perturbation caused by numerical errors is sometimes inevitable. This paper studies how perturbation of MCMC affects the convergence spe...

We study the problem of unbiased estimation of expectations with respect to (w.r.t.) $\pi$ a given, general probability measure on $(\mathbb{R}^d,\mathcal{B}(\mathbb{R}^d))$ that is absolutely conti...

We consider the problem of static Bayesian inference for partially observed Levy-process models. We develop a methodology which allows one to infer static parameters and some states of the process, ...

The stability and contraction properties of positive integral semigroups on Polish spaces are investigated. Our novel analysis is based on the extension of V-norm contraction methods, associated to ...

We consider the problem of high-dimensional filtering of state-space models (SSMs) at discrete times. This problem is particularly challenging as analytical solutions are typically not available and...

In this article we consider the development of unbiased estimators of the Hessian, of the log-likelihood function with respect to parameters, for partially observed diffusion processes. These proces...

In this article we consider the application of multilevel Monte Carlo, for the estimation of normalizing constants. In particular we will make use of the filtering algorithm, the ensemble Kalman-Buc...

Multilevel Monte Carlo (MLMC) has become an important methodology in applied mathematics for reducing the computational cost of weak approximations. For many problems, it is well-known that strong p...

This position paper summarizes a recently developed research program focused on inference in the context of data centric science and engineering applications, and forecasts its trajectory forward ov...

We consider the problem of statistical inference for a class of partially-observed diffusion processes, with discretely-observed data and finite-dimensional parameters. We construct unbiased estimat...

Markov chain Monte Carlo (MCMC) is a powerful methodology for the approximation of posterior distributions. However, the iterative nature of MCMC does not naturally facilitate its use with modern hi...

In this article, we consider computing expectations w.r.t. probability measures which are subject to discretization error. Examples include partially observed diffusion processes or inverse problems...

In this article we consider the estimation of the log-normalization constant associated to a class of continuous-time filtering models. In particular, we consider ensemble Kalman-Bucy filter based e...

In this article we consider the linear filtering problem in continuous-time. We develop and apply multilevel Monte Carlo (MLMC) strategies for ensemble Kalman-Bucy filters (EnKBFs). These filters ca...

A novel solution to the smoothing problem for multi-object dynamical systems is proposed and evaluated. The systems of interest contain an unknown and varying number of dynamical objects that are pa...

In this paper, we consider the filtering problem for partially observed diffusions, which are regularly observed at discrete times. We are concerned with the case when one must resort to time-discre...

Bayesian inference is a powerful paradigm for quantum state tomography, treating uncertainty in meaningful and informative ways. Yet the numerical challenges associated with sampling from complex pr...

In this article we consider a Monte Carlo-based method to filter partially observed diffusions observed at regular and discrete times. Given access only to Euler discretizations of the diffusion pro...

In the following article we consider the non-linear filtering problem in continuous-time and in particular the solution to Zakai's equation or the normalizing constant. We develop a methodology to p...

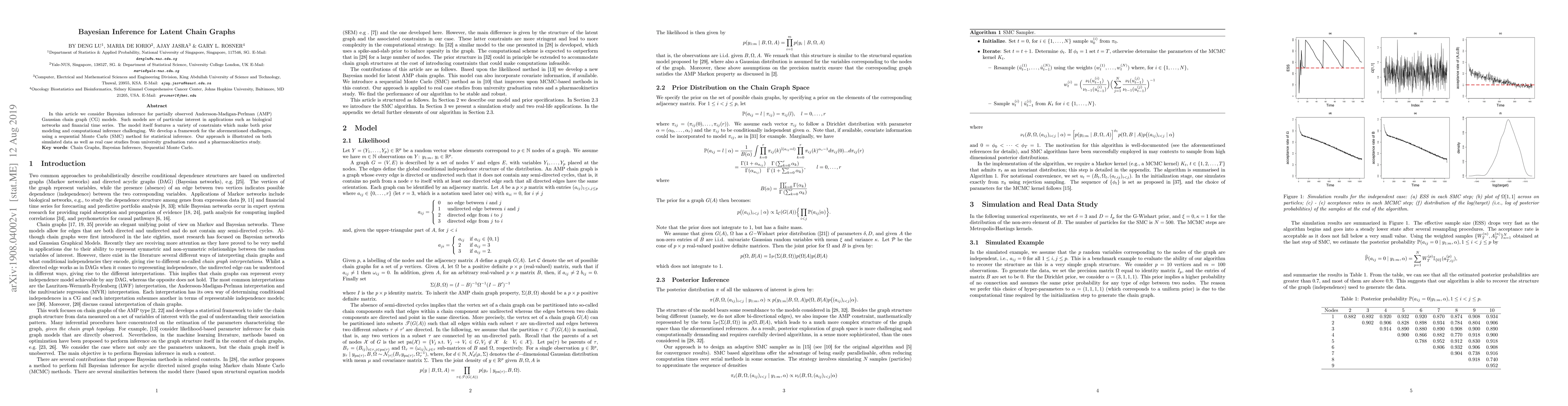

In this article we consider Bayesian inference for partially observed Andersson-Madigan-Perlman (AMP) Gaussian chain graph (CG) models. Such models are of particular interest in applications such as...

We consider a class of finite time horizon nonlinear stochastic optimal control problem, where the control acts additively on the dynamics and the control cost is quadratic. This framework is flexib...

In this article we prove a new central limit theorem (CLT) for coupled particle filters (CPFs). CPFs are used for the sequential estimation of the difference of expectations w.r.t. filters which are...

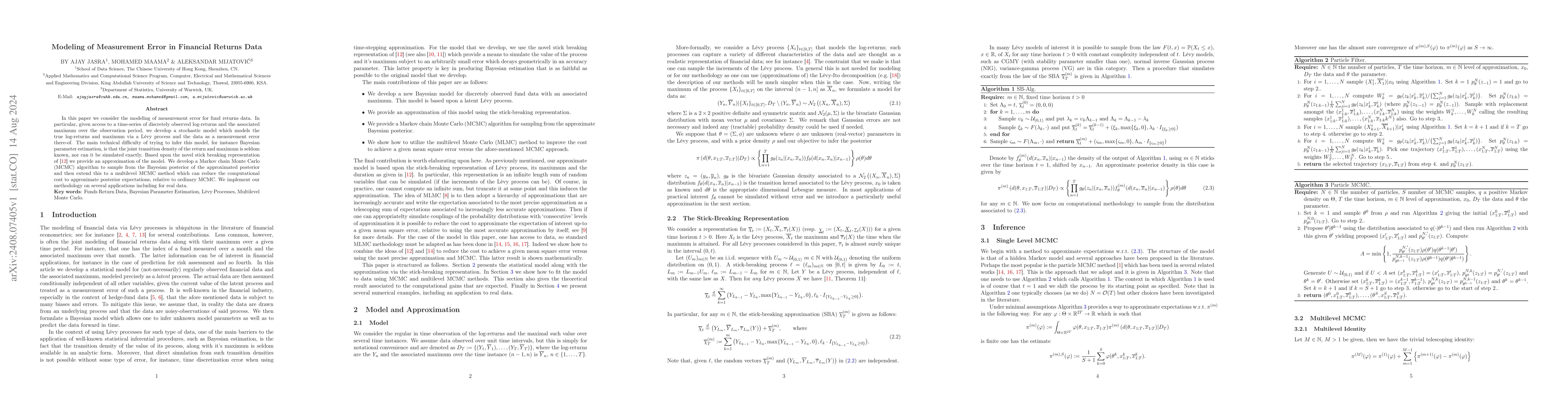

In this paper we consider the modeling of measurement error for fund returns data. In particular, given access to a time-series of discretely observed log-returns and the associated maximum over the o...

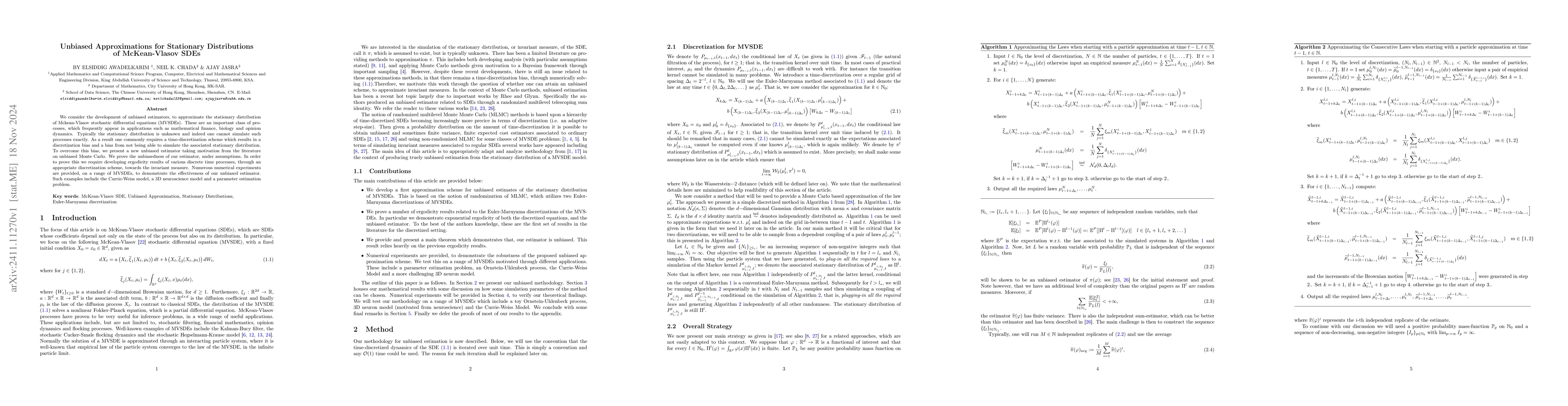

We consider the development of unbiased estimators, to approximate the stationary distribution of Mckean-Vlasov stochastic differential equations (MVSDEs). These are an important class of processes, w...

In this article we consider likelihood-based estimation of static parameters for a class of partially observed McKean-Vlasov (POMV) diffusion process with discrete-time observations over a fixed time ...

In this paper we examine the numerical approximation of the limiting invariant measure associated with Feynman-Kac formulae. These are expressed in a discrete time formulation and are associated with ...

In this paper we consider the estimation of unknown parameters in Bayesian inverse problems. In most cases of practical interest, there are several barriers to performing such estimation, This include...

We consider the problem of Bayesian inference for bi-variate data observed in time but with observation times which occur non-synchronously. In particular, this occurs in a wide variety of application...

In this article we consider Bayesian estimation of static parameters for a class of partially observed McKean-Vlasov diffusion processes with discrete-time observations over a fixed time interval. Thi...

In this note we consider the finite-dimensional parameter estimation problem associated to inverse problems. In such scenarios, one seeks to maximize the marginal likelihood associated to a Bayesian m...

In this article we consider the estimation of static parameters for partially observed diffusion processes with discrete-time observations over a fixed time interval. In particular, when one only has ...

We consider the discrete-time filtering problem in scenarios where the observation noise is degenerate or low. More precisely, one is given access to a discrete time observation sequence which at any ...

In this article, we consider the problem of clustering multi-view data, that is, information associated to individuals that form heterogeneous data sources (the views). We adopt a Bayesian model and i...

We consider the discrete-time filtering problem in scenarios where the observation noise is degenerate or low. We focus on the case where the observation equation is a linear function of the state and...

Entropic optimal transport problems play an increasingly important role in machine learning and generative modelling. In contrast with optimal transport maps which often have limited applicability in ...

In this paper we consider parameter estimation for discretely observed diffusion processes. In particular, we focus on data that are observed at low frequency and methodology that can estimate paramet...

In this paper we consider the parameter estimation problem associated to partially-observed time changed SDEs, with observations that are given at discrete times. In particular we consider both likeli...

In this paper we consider the conditional stochastic optimization (CSO) problem. This consists of optimizing a function which can be written as the expectation of a function which is itself a function...

In this paper we investigate the efficacy of the score-based martingale posteriors (SMP) (Cui & Walker, 2025; Fong et al., 2023) in the context of modern and large-scale machine learning problems and ...