Academic Profile

Statistics

Similar Authors

Papers on arXiv

Portfolio's optimal drivers for diversification are common causes of the constituents' correlations. A closed-form formula for the conditional probability of the portfolio given its optimal common d...

Multi-modal regression is important in forecasting nonstationary processes or with a complex mixture of distributions. It can be tackled with multiple hypotheses frameworks but with the difficulty o...

We present a method to test and monitor structural relationships between time variables. The distribution of the first eigenvalue for lagged correlation matrices (Tracy-Widom distribution) is used t...

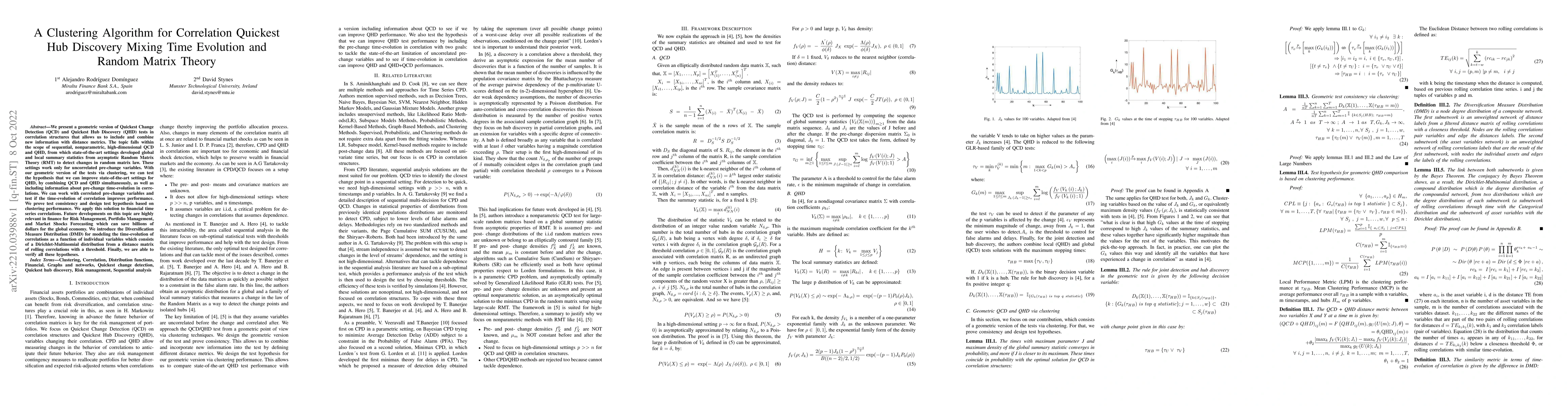

We present a geometric version of Quickest Change Detection (QCD) and Quickest Hub Discovery (QHD) tests in correlation structures that allows us to include and combine new information with distance...

We present a framework for modeling asset and portfolio dynamics, incorporating this information into portfolio optimization. For this framework, we introduce the Commonality Principle, providing a ...

A framework for portfolio allocation based on multiple hypotheses prediction using structured ensemble models is presented. Portfolio optimization is formulated as an ensemble learning problem, where ...

Fundamental and necessary principles for achieving efficient portfolio optimization based on asset and diversification dynamics are presented. The Commonality Principle is a necessary and sufficient c...

This paper challenges the claim that causal factor modeling is a necessary condition for investment efficiency. Through formal analysis and empirical counterexamples, we show that predictive models, e...

Existing approaches to predictive uncertainty rely either on multi-hypothesis prediction, which promotes diversity but lacks principled aggregation, or on ensemble learning, which improves accuracy bu...

Classical portfolio models collapse under structural breaks, while modern machine-learning allocators adapt flexibly but often at the cost of transparency and interpretability. This paper introduces C...

We introduce an operator-theoretic framework for causal analysis in multivariate time series based on order-constrained spectral non-invariance. Directional influence is defined as sensitivity of seco...

No-arbitrage asset pricing characterizes valuation through the existence of equivalent martingale measures relative to a filtration and a class of admissible trading strategies. In practice, pricing i...

Large language models are trained primarily on human-generated data and feedback, yet they exhibit persistent errors arising from annotation noise, subjective preferences, and the limited expressive b...

We study the squared price-of-risk premium of a portfolio -- an integrated conditional squared Sharpe-ratio functional, not an expected excess return -- and its attribution to causal drivers. Relative...

We formalize a single structural condition on a portfolio problem, causal separation: conditional on the realized path of a declared set of drivers through the investment horizon, asset returns are mu...

When a portfolio is conditioned on a minimal set of observable drivers under which its assets become mutually independent over the investment horizon, the dynamic investment problem acquires a distinc...