Academic Profile

Statistics

Similar Authors

Papers on arXiv

Data envelopment analysis (DEA) theory formulates a number of desirable properties that DEA models should satisfy. Among these, indication, strict monotonicity, and strong efficiency of projections ...

The \emph{law of one price (LOP)} broadly asserts that identical financial flows should command the same price. We show that, when properly formulated, LOP is the minimal condition for a well-define...

The paper analyses properties of a large class of "path-based" Data Envelopment Analysis models through a unifying general scheme. The scheme includes the well-known oriented radial models, the hype...

The paper investigates quadratic hedging in a semimartingale market that does not necessarily contain a risk-free asset. An equivalence result for hedging with and without numeraire change is establ...

It is shown that the ratio between the mean and the $L^2$-norm leads to a particularly parsimonious description of the mean-variance efficient frontier and the dual pricing kernel restrictions known...

The paper develops multiplicative compensation for complex-valued semimartingales and studies some of its consequences. It is shown that the stochastic exponential of any complex-valued semimartinga...

We develop a stochastic calculus that makes it easy to capture a variety of predictable transformations of semimartingales such as changes of variables, stochastic integrals, and their compositions....

A new integral with respect to an integer-valued random measure is introduced. In contrast to the finite variation integral ubiquitous in semimartingale theory (Jacod and Shiryaev, 2003, II.1.5), th...

We study dynamic optimal portfolio allocation for monotone mean--variance preferences in a general semimartingale model. Armed with new results in this area we revisit the work of Cui, Li, Wang and ...

In life-cycle economics the Samuelson paradigm (Samuelson, 1969) states that the optimal investment is in constant proportions out of lifetime wealth composed of current savings and the present valu...

In this paper we report further progress towards a complete theory of state-independent expected utility maximization with semimartingale price processes for arbitrary utility function. Without any ...

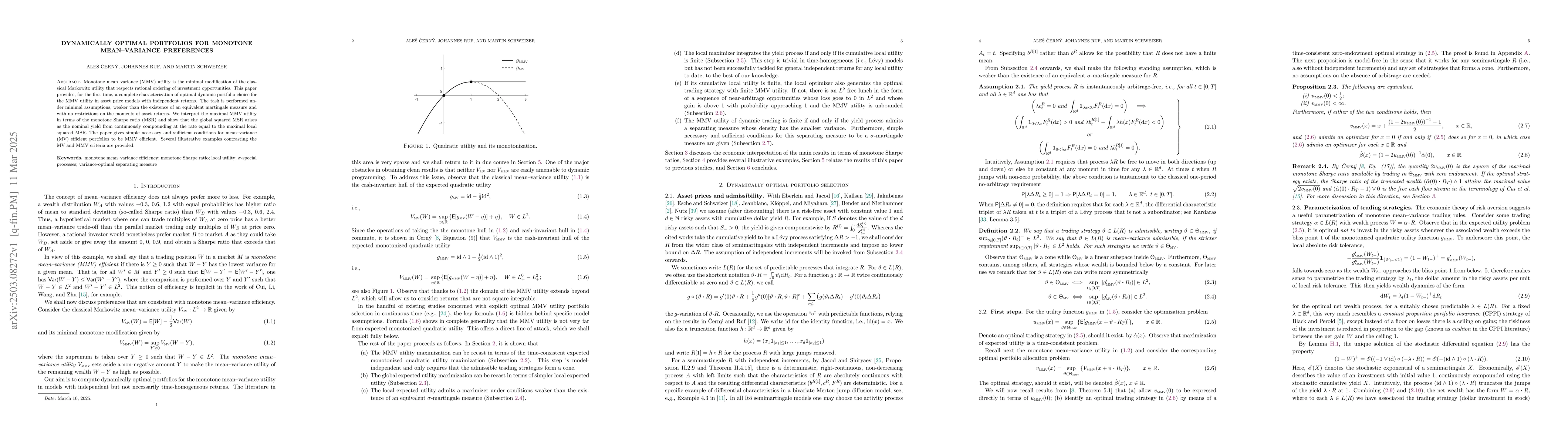

Monotone mean-variance (MMV) utility is the minimal modification of the classical Markowitz utility that respects rational ordering of investment opportunities. This paper provides, for the first time...

Uniformly weighted divergence preferences (UWDP) introduced in Maccheroni et al. (2006) are an important class of risk-averse preferences that contain as a special case the monotone mean--variance uti...