Academic Profile

Statistics

Similar Authors

Papers on arXiv

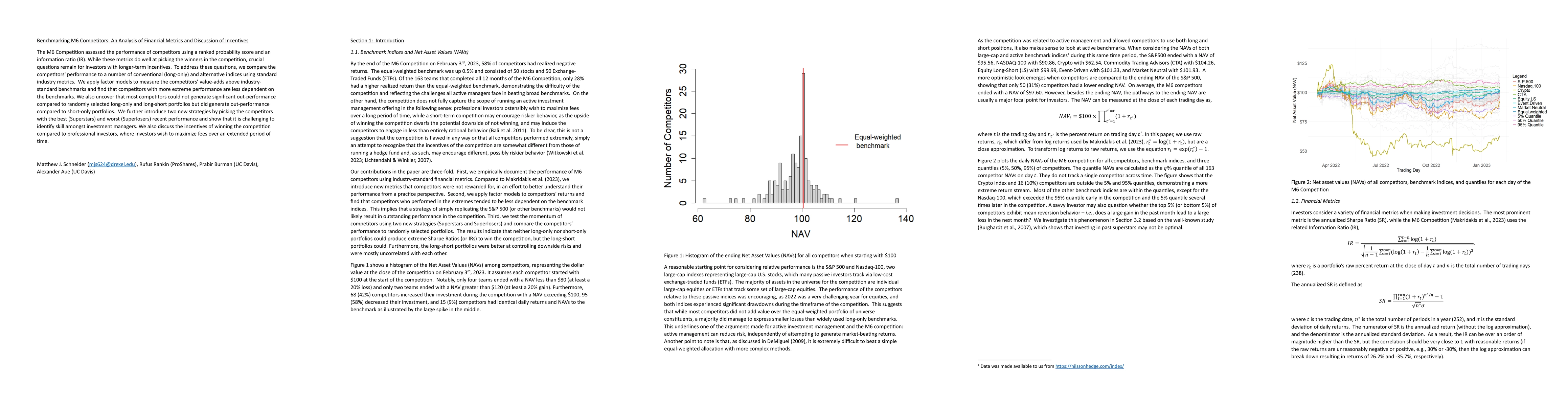

The M6 Competition assessed the performance of competitors using a ranked probability score and an information ratio (IR). While these metrics do well at picking the winners in the competition, cruc...

This paper deals with two-sample tests for functional time series data, which have become widely available in conjunction with the advent of modern complex observation systems. Here, particular inte...

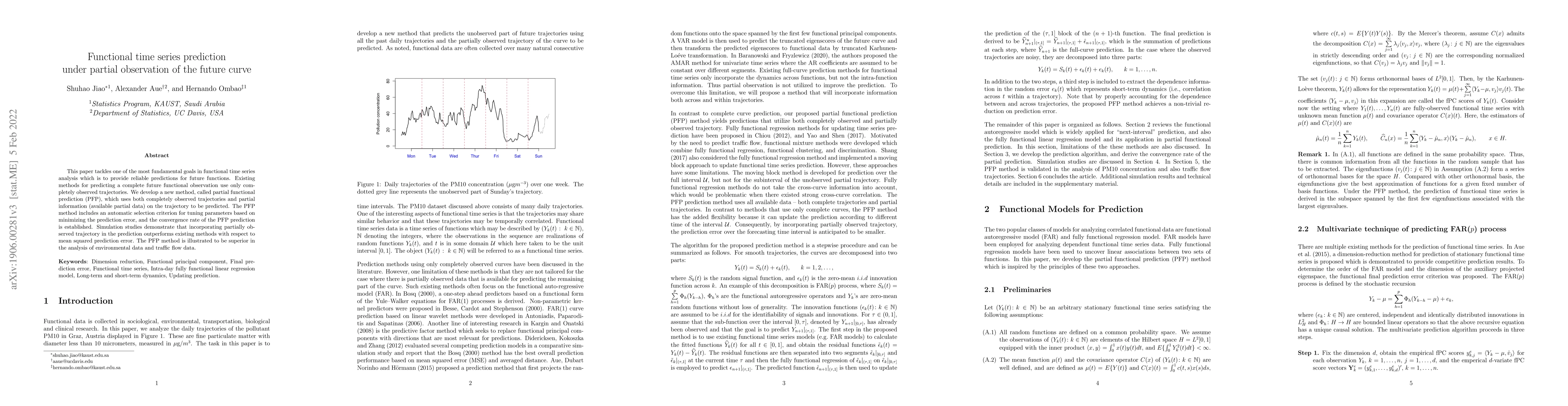

This paper tackles one of the most fundamental goals in functional time series analysis which is to provide reliable predictions for future functions. Existing methods for predicting a complete futu...

Invertible processes naturally arise in many aspects of functional time series analysis, and consistent estimation of the infinite dimensional operators that define them are of interest. Asymptotic up...

We propose a novel estimation procedure for certain spectral distributions associated with a class of high dimensional linear time series. The processes under consideration are of the form $X_t = \sum...

We transform the randomness of LLMs into precise assurances using an actuator at the API interface that applies a user-defined risk constraint in finite samples via Conformal Risk Control (CRC). This ...

Deploying black-box LLMs requires managing uncertainty in the absence of token-level probability or true labels. We propose introducing an unsupervised conformal inference framework for generation, wh...

This paper evaluates the performance of classical time series models in forecasting Bitcoin prices, focusing on ARIMA, SARIMA, GARCH, and EGARCH. Daily price data from 2010 to 2020 were analyzed, with...

The rapid adoption of synthetic data for training Large Language Models (LLMs) has introduced the technical challenge of "model collapse"-a degenerative process where recursive training on model-gener...

AutoRegressive Conditional Heteroscedasticity (ARCH) models are standard for modeling time series exhibiting volatility, with a rich literature in univariate and multivariate settings. In recent years...

We construct geometric regime-switching diffusions, a class of Markov processes on locally compact stratified Riemannian state spaces. In contrast with classical regime-switching and stochastic hybrid...