Bitcoin Forecasting with Classical Time Series Models on Prices and Volatility

Publication

Metrics

Paper Preview

Abstract

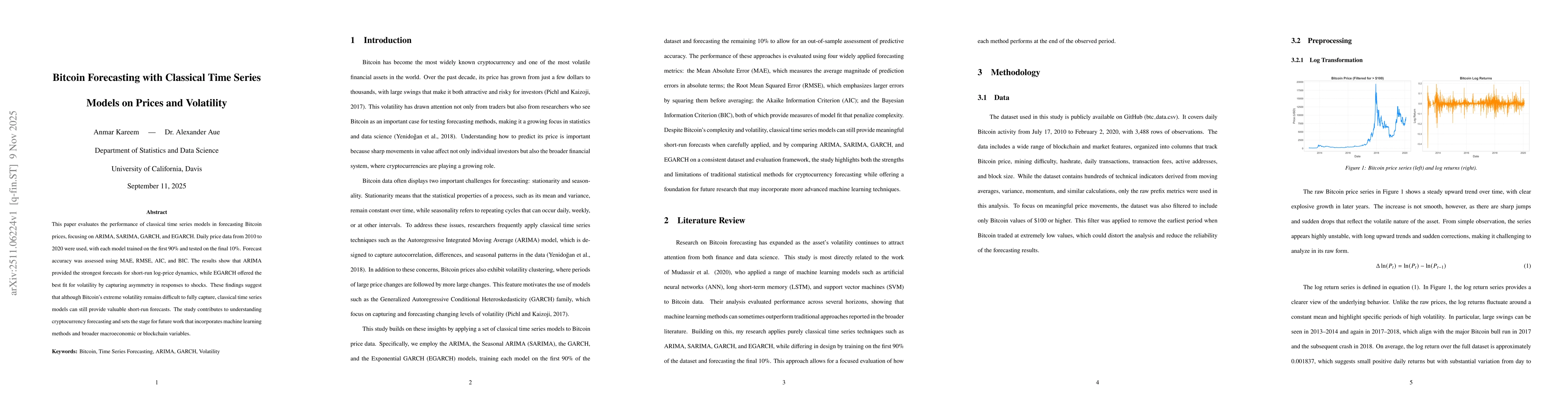

This paper evaluates the performance of classical time series models in forecasting Bitcoin prices, focusing on ARIMA, SARIMA, GARCH, and EGARCH. Daily price data from 2010 to 2020 were analyzed, with models trained on the first 90 percent and tested on the final 10 percent. Forecast accuracy was assessed using MAE, RMSE, AIC, and BIC. The results show that ARIMA provided the strongest forecasts for short-run log-price dynamics, while EGARCH offered the best fit for volatility by capturing asymmetry in responses to shocks. These findings suggest that despite Bitcoin's extreme volatility, classical time series models remain valuable for short-run forecasting. The study contributes to understanding cryptocurrency predictability and sets the stage for future work integrating machine learning and macroeconomic variables.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Discussion 0