Academic Profile

Statistics

Similar Authors

Papers on arXiv

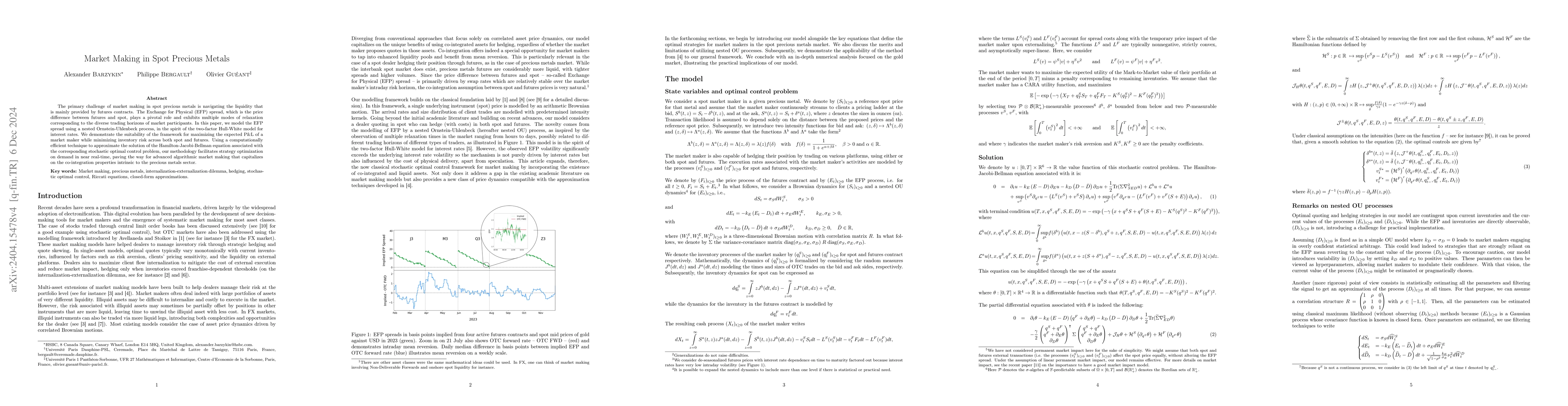

The primary challenge of market making in spot precious metals is navigating the liquidity that is mainly provided by futures contracts. The Exchange for Physical (EFP) spread, which is the price di...

In FX cash markets, market makers provide liquidity to clients for a wide variety of currency pairs. Because of flow uncertainty and market volatility, they face inventory risk. To mitigate this ris...

Dealers make money by providing liquidity to clients but face flow uncertainty and thus price risk. They can efficiently skew their prices and wait for clients to mitigate risk (internalization), or...

In dealer markets, dealers provide prices at which they agree to buy and sell the assets and securities they have in their scope. With ever increasing trading volume, this quoting task has to be don...

We consider a central trading desk which aggregates the inflow of clients' orders with unobserved toxicity, i.e. persistent adverse directionality. The desk chooses either to internalise the inflow or...

Over the past decade, many dealers have implemented algorithmic models to automatically respond to RFQs and manage flows originating from their electronic platforms. In parallel, building on the found...

As the FX markets continue to evolve, many institutions have started offering passive access to their internal liquidity pools. Market makers act as principal and have the opportunity to fill those or...

Dealers in foreign exchange markets provide bid and ask prices to their clients at which they are happy to buy and sell, respectively. To manage risk, dealers can skew their quotes and hedge in the in...

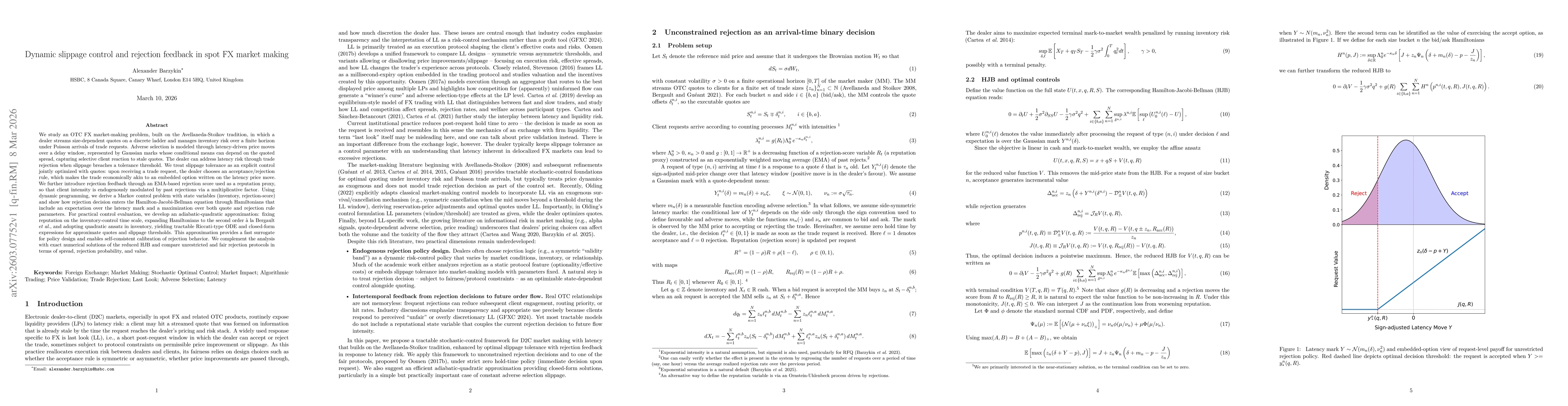

We study an OTC FX market-making problem, built on the Avellaneda-Stoikov tradition, in which a dealer streams size-dependent quotes on a discrete ladder and manages inventory risk over a finite horiz...

We study market making in aggregator-routed RFQ markets where platform routing depends on slowly varying dealer performance scores. We propose a two-tier stochastic control model that separates RFQ-le...

We study OTC bond market making on a size ladder with quadratic inventory penalty and a running target on the dealer's size-weighted hit ratio within a stochastic optimal control approach. We demonstr...