Academic Profile

Statistics

Similar Authors

Papers on arXiv

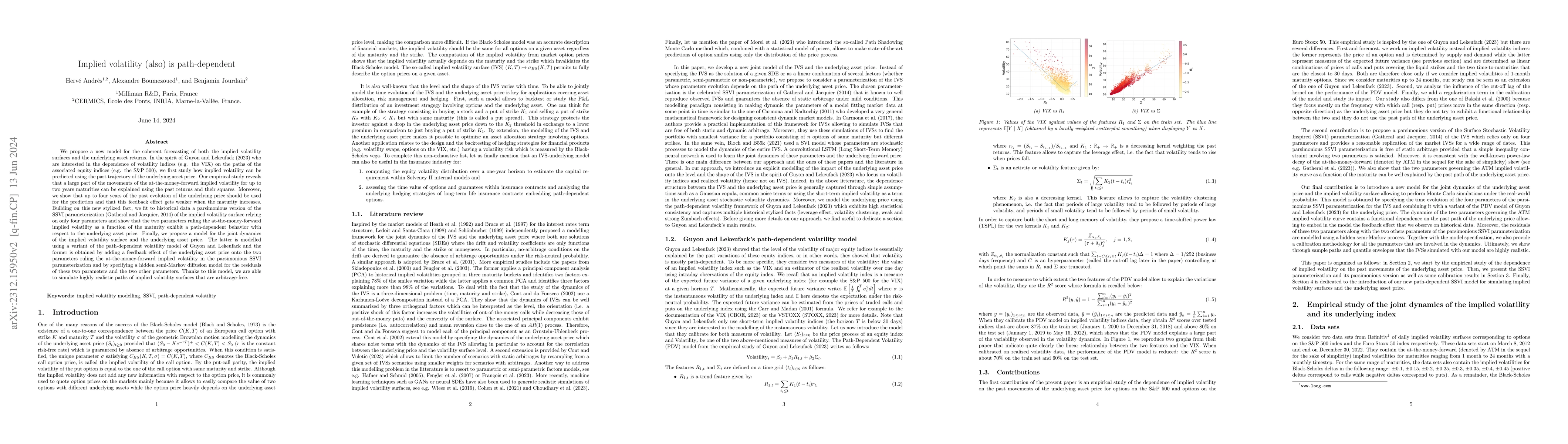

We propose a new model for the coherent forecasting of both the implied volatility surfaces and the underlying asset returns.In the spirit of Guyon and Lekeufack (2023) who are interested in the dep...

With the growing digital transformation of the worldwide economy, cyber risk has become a major issue. As 1 % of the world's GDP (around $1,000 billion) is allegedly lost to cybercrime every year, I...

Motivated by insurance applications, we propose a new approach for the validation of real-world economic scenarios. This approach is based on the statistical test developed by Chevyrev and Oberhause...

We propose to take advantage of the common knowledge of the characteristic function of the swap rate process as modelled in the LIBOR Market Model with Stochastic Volatility and Displaced Diffusion ...

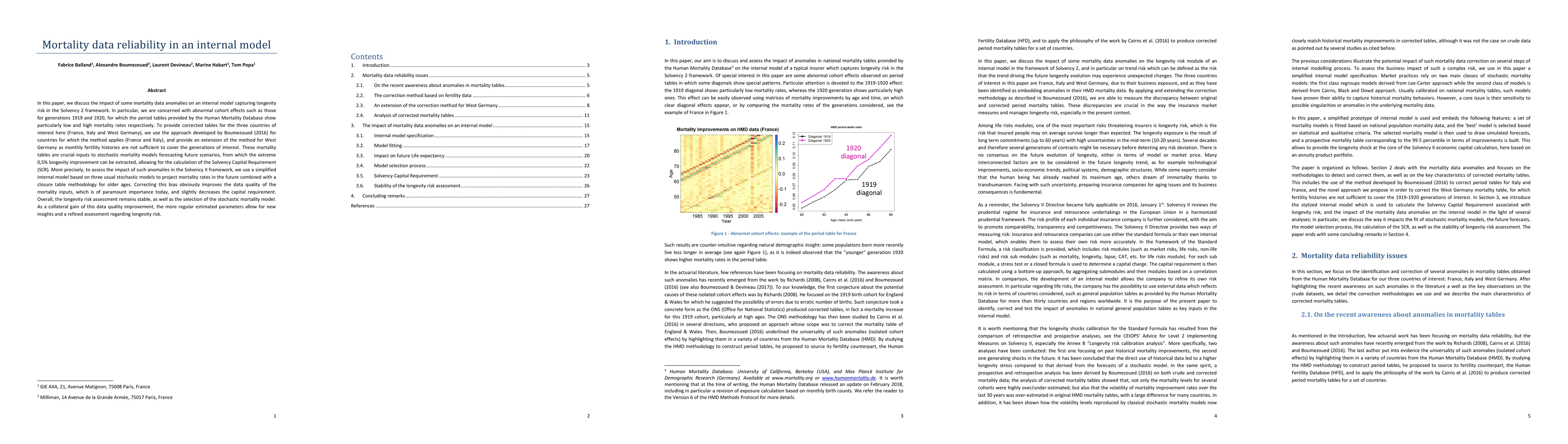

In this paper, we discuss the impact of some mortality data anomalies on an internal model capturing longevity risk in the Solvency 2 framework. In particular, we are concerned with abnormal cohort ...

Estimating risk measures such as large loss probabilities and Value-at-Risk is fundamental in financial risk management and often relies on computationally intensive nested Monte Carlo methods. While ...