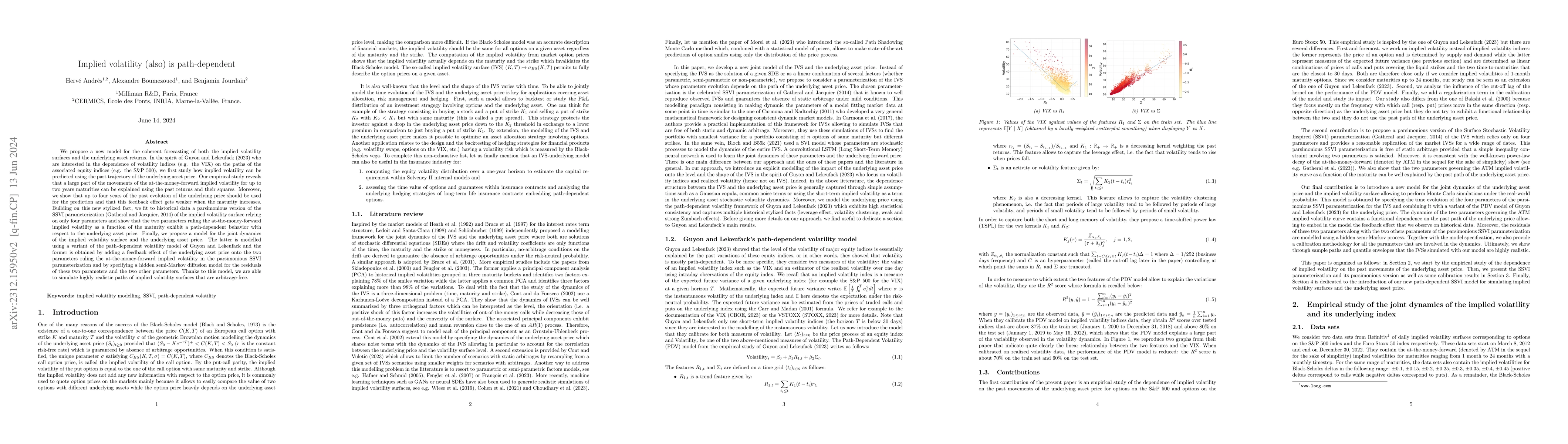

We propose a new model for the coherent forecasting of both the implied

volatility surfaces and the underlying asset returns.In the spirit of Guyon and

Lekeufack (2023) who are interested in the dependence of volatility indices

(e.g. the VIX) on the paths of the associated equity indices (e.g. the S&P

500), we first study how implied volatility can be predicted using the past

trajectory of the underlying asset price. Our empirical study reveals that a

large part of the movements of the at-the-money-forward implied volatility for

up to two years maturities can be explained using the past returns and their

squares. Moreover, we show that up to four years of the past evolution of the

underlying price should be used for the prediction and that this feedback

effect gets weaker when the maturity increases. Building on this new stylized

fact, we fit to historical data a parsimonious version of the SSVI

parameterization (Gatheral and Jacquier, 2014) of the implied volatility

surface relying on only four parameters and show that the two parameters ruling

the at-the-money-forward implied volatility as a function of the maturity

exhibit a path-dependent behavior with respect to the underlying asset price.

Finally, we propose a model for the joint dynamics of the implied volatility

surface and the underlying asset price. The latter is modelled using a variant

of the path-dependent volatility model of Guyon and Lekeufack and the former is

obtained by adding a feedback effect of the underlying asset price onto the two

parameters ruling the at-the-money-forward implied volatility in the

parsimonious SSVI parameterization and by specifying a hidden semi-Markov

diffusion model for the residuals of these two parameters and the two other

parameters. Thanks to this model, we are able to simulate highly realistic

paths of implied volatility surfaces that are arbitrage-free.

Discussion 0