Academic Profile

Statistics

Similar Authors

Papers on arXiv

We are interested in the discretization of stable driven SDEs with additive noise for $\alpha$ $\in$ (1, 2) and Lq -- Lp drift under the Serrin type condition $\alpha$/q + d/p < $\alpha$ -- 1. We sh...

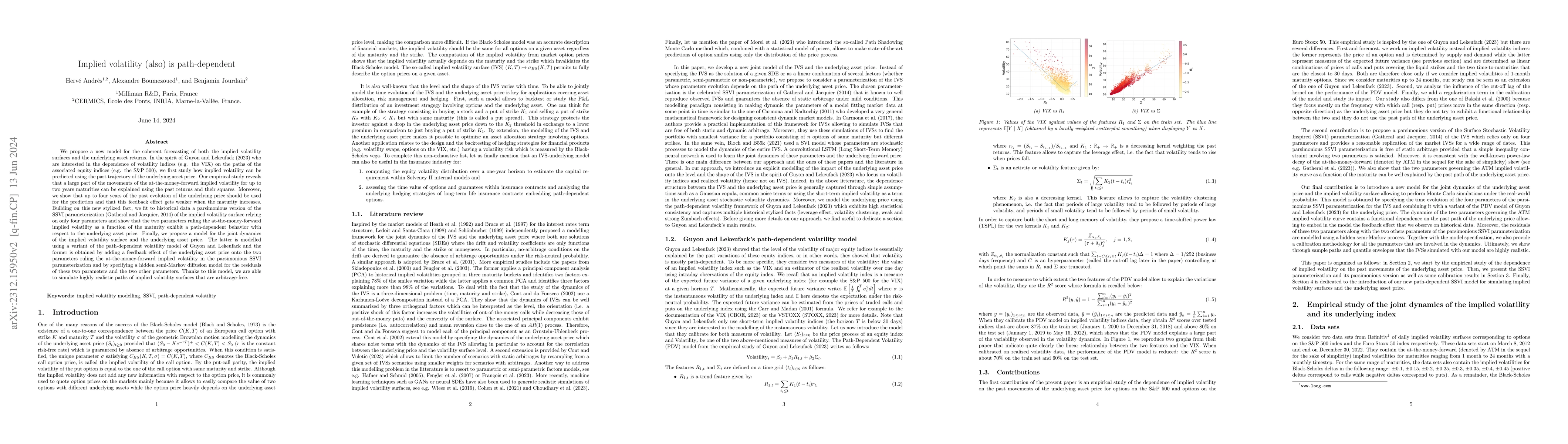

We propose a new model for the coherent forecasting of both the implied volatility surfaces and the underlying asset returns.In the spirit of Guyon and Lekeufack (2023) who are interested in the dep...

In this paper, we are interested in the propagation of convexity by the strong solution to a one-dimensional Brownian stochastic differential equation with coefficients Lipschitz in the spatial vari...

In this note, we complete the analysis of the Martingale Wasserstein Inequality started in arXiv:2011.11599 by checking that this inequality fails in dimension $d\ge 2$ when the integrability parame...

The stratified resampling mechanism is one of the resampling schemes commonly used in the resampling steps of particle filters. In the present paper, we prove a central limit theorem for this mechan...

In this work, we prove the joint convergence in distribution of $q$ variables modulo one obtained as partial sums of a sequence of i.i.d. square integrable random variables multiplied by a common fa...

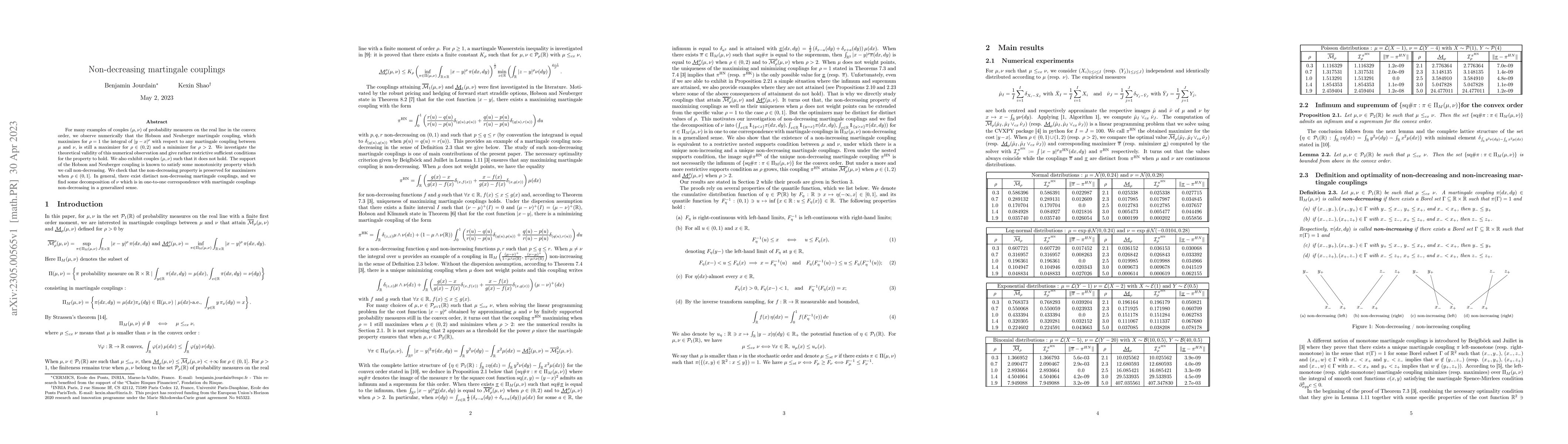

For many examples of couples $(\mu,\nu)$ of probability measures on the real line in the convex order, we observe numerically that the Hobson and Neuberger martingale coupling, which maximizes for $...

While many questions in robust finance can be posed in the martingale optimal transport framework or its weak extension, others like the subreplication price of VIX futures, the robust pricing of Am...

In this paper, we are interested in comparing solutions to stochastic Volterra equations for the convex order on the space of continuous $\R^d$-valued paths and for the monotonic convex order when $...

Wasserstein projections in the convex order were first considered in the framework of weak optimal transport, and found application in various problems such as concentration inequalities and marting...

Motivated by insurance applications, we propose a new approach for the validation of real-world economic scenarios. This approach is based on the statistical test developed by Chevyrev and Oberhause...

The central limit theorem is, with the strong law of large numbers, one of the two fundamental limit theorems in probability theory. Benjamin Jourdain and Alvin Tse have extended to non-linear funct...

While many questions in (robust) finance can be posed in the martingale optimal transport (MOT) framework, others require to consider also non-linear cost functionals. Following the terminology of G...

We are interested in the time discretization of stochastic differential equations with additive d-dimensional Brownian noise and L q -- L $\rho$ drift coefficient when the condition d $\rho$ + 2 q <...

We are interested in martingale rearrangement couplings. As introduced by Wiesel [37] in order to prove the stability of Martingale Optimal Transport problems, these are projections in adapted Wasse...

Our main result is to establish stability of martingale couplings: suppose that $\pi$ is a martingale coupling with marginals $\mu, \nu$. Then, given approximating marginal measures $\tilde \mu \app...

Quantization provides a very natural way to preserve the convex order when approximating two ordered probability measures by two finitely supported ones. Indeed, when the convex order dominating ori...

We establish for dual quantization the counterpart of Kieffer's uniqueness result for compactly supported one dimensional probability distributions having a $\log$-concave density (also called stron...

The purpose of this paper is to study the existence and uniqueness of solutions to a Stochastic Differential Equation (SDE) coming from the eigenvalues of Wishart processes. The coordinates are non-...

In this work, a generalised version of the central limit theorem is proposed for nonlinear functionals of the empirical measure of i.i.d. random variables, provided that the functional satisfies som...

We are interested in proposing approximations of a sequence of probability measures in the convex order by finitely supported probability measures still in the convex order. We propose to alternate ...

We show the existence and uniqueness of a continuous solution to a path-dependent volatility model introduced by Guyon and Lekeufack (2023) to model the price of an equity index and its spot volatilit...

Motivated by the study of the propagation of convexity by semi-groups of stochastic differential equations and convex comparison between the distributions of solutions of two such equations, we study ...

Local stochastic volatility refers to a popular model class in applied mathematical finance that allows for "calibration-on-the-fly", typically via a particle method, derived from a formal McKean-Vlas...

In this paper, we first show continuity of both Wasserstein projections in the convex order when they are unique. We also check that, in arbitrary dimension $d$, the quadratic Wasserstein projection o...

In this note, we give a simple derivation of the formula obtained in Dowson and Landau (1982), Olkin and Pukelsheim (1982) and Givens and Shortt (1984) for the quadratic Wasserstein distance between t...

In this paper, we investigate the distributions of random couples $(X,Y)$ with $X$ real-valued such that any non-negative integrable random variable $f(X)$ can be represented as a conditional expectat...

According to Talay and Tubaro \cite{talay_expansion_1990}, the weak error between the solution to a stochastic differential equation with smooth coefficients and its Euler-Maruyama scheme can be expan...

The addition of the running time as a component of a path before computing its signature is a widespread approach to ensure the one-to-one property between them and leads to universal approximation th...

We emphasize that for a stochastic differential equation with isotropic stable additive noise and non Lipschitz drift, when considering an appropriate discretization scheme and the associated weak err...

We investigate a McKean-Vlasov stochastic differential equation with an additive common noise and in which the interaction is through the conditional expectation. We show that, in the presence of an a...