Academic Profile

Statistics

Similar Authors

Papers on arXiv

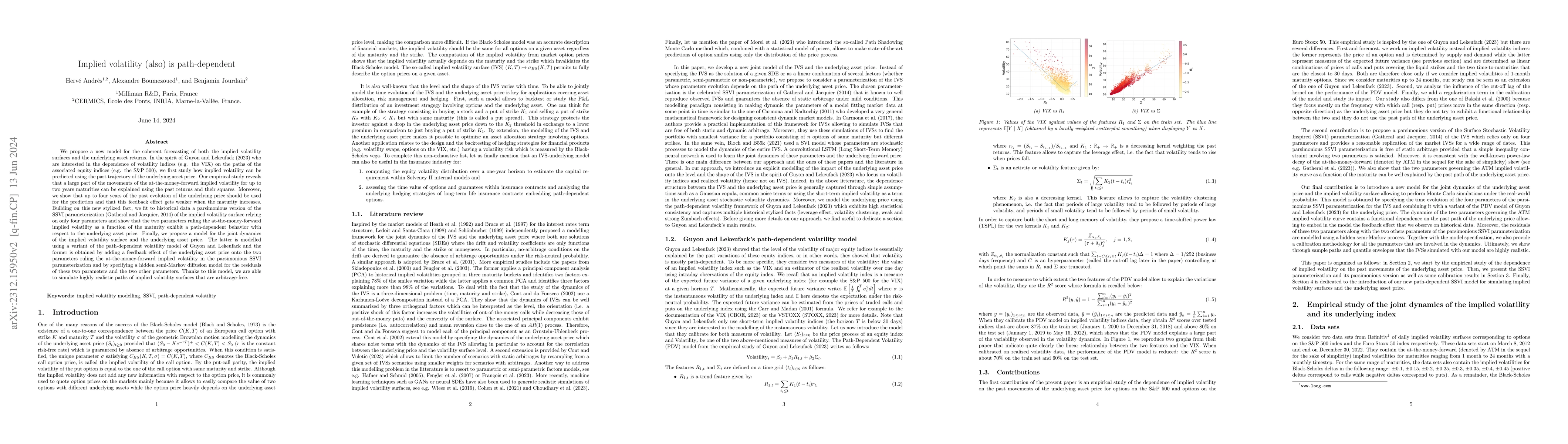

We propose a new model for the coherent forecasting of both the implied volatility surfaces and the underlying asset returns.In the spirit of Guyon and Lekeufack (2023) who are interested in the dep...

Motivated by insurance applications, we propose a new approach for the validation of real-world economic scenarios. This approach is based on the statistical test developed by Chevyrev and Oberhause...

We show the existence and uniqueness of a continuous solution to a path-dependent volatility model introduced by Guyon and Lekeufack (2023) to model the price of an equity index and its spot volatilit...

The addition of the running time as a component of a path before computing its signature is a widespread approach to ensure the one-to-one property between them and leads to universal approximation th...