Academic Profile

Statistics

Similar Authors

Papers on arXiv

Claim reserving primarily relies on macro-level models, with the Chain-Ladder method being the most widely adopted. These methods were heuristically developed without minimal statistical foundations...

With the advancement in technology, telematics data which capture vehicle movements information are becoming available to more insurers. As these data capture the actual driving behaviour, they are ...

Experience rating in insurance uses a Bayesian credibility model to upgrade the current premiums of a contract by taking into account policyholders' attributes and their claim history. Most data-dri...

A well-designed framework for risk classification and ratemaking in automobile insurance is key to insurers' profitability and risk management, while also ensuring that policyholders are charged a f...

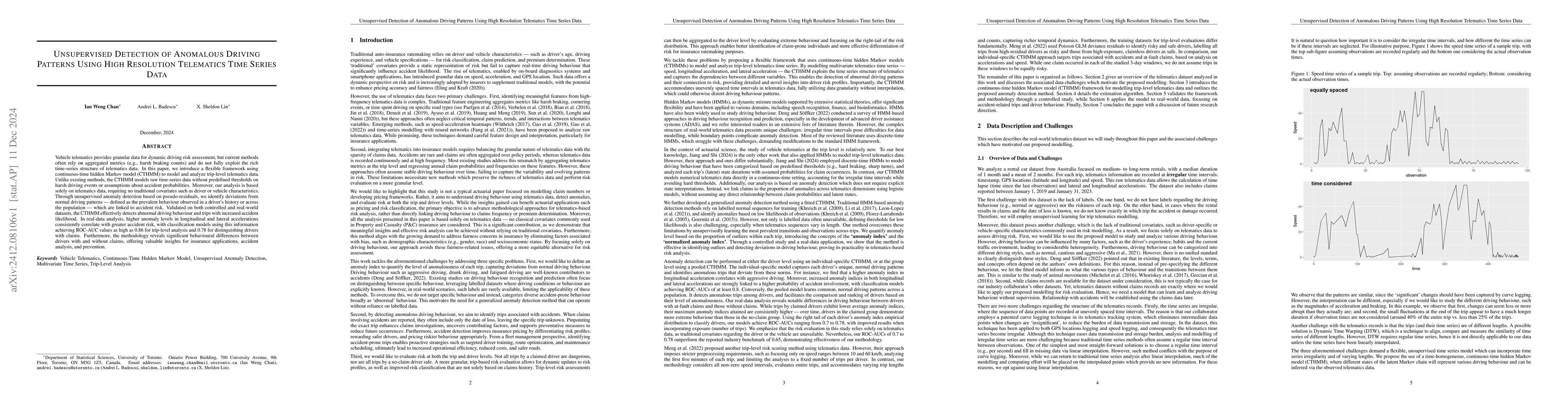

Vehicle telematics provides granular data for dynamic driving risk assessment, but current methods often rely on aggregated metrics (e.g., harsh braking counts) and do not fully exploit the rich time-...

Claim reserving in insurance has been studied through two primary frameworks: the macro-level approach, which estimates reserves at an aggregate level (e.g., Chain-Ladder), and the micro-level approac...