Academic Profile

Statistics

Similar Authors

Papers on arXiv

In constrained Markov decision processes (CMDPs) with adversarial rewards and constraints, a well-known impossibility result prevents any algorithm from attaining both sublinear regret and sublinear...

We study online learning in constrained Markov decision processes (CMDPs) in which rewards and constraints may be either stochastic or adversarial. In such settings, Stradi et al.(2024) proposed the f...

We study a repeated trading problem in which a mechanism designer facilitates trade between a single seller and multiple buyers. Our model generalizes the classic bilateral trade setting to a multi-bu...

Bilateral trade is a central problem in algorithmic economics, and recent work has explored how to design trading mechanisms using no-regret learning algorithms. However, no-regret learning is impossi...

We study online bilateral trade, where a learner facilitates repeated exchanges between a buyer and a seller to maximize the Gain From Trade (GFT), i.e., the social welfare. In doing so, the learner m...

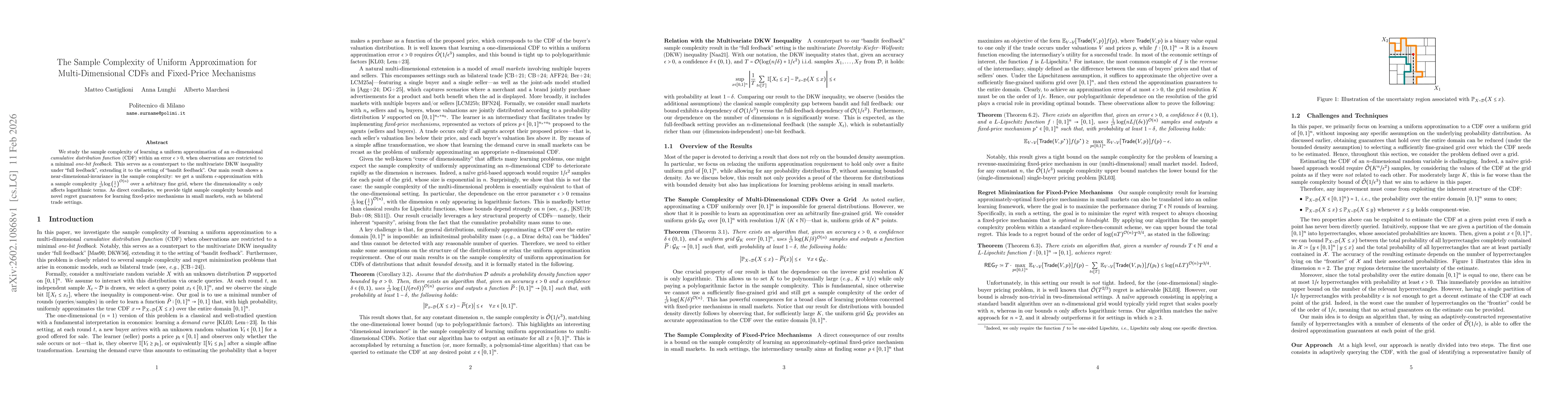

We study the sample complexity of learning a uniform approximation of an $n$-dimensional cumulative distribution function (CDF) within an error $ε> 0$, when observations are restricted to a minimal on...

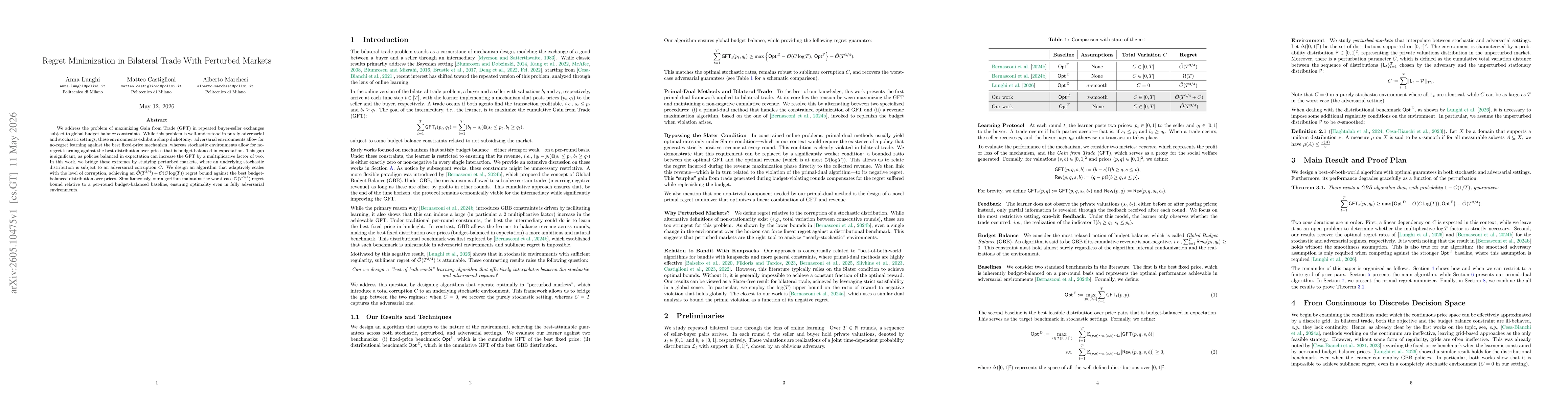

We address the problem of maximizing Gain from Trade (GFT) in repeated buyer-seller exchanges subject to global budget balance constraints. While this problem is well-understood in purely adversarial ...