Academic Profile

Statistics

Similar Authors

Papers on arXiv

We introduce a new Langevin dynamics based algorithm, called e-TH$\varepsilon$O POULA, to solve optimization problems with discontinuous stochastic gradients which naturally appear in real-world appli...

We present a novel $Q$-learning algorithm tailored to solve distributionally robust Markov decision problems where the corresponding ambiguity set of transition probabilities for the underlying Markov...

In this paper, we extend the Wiener-Ito chaos decomposition to the class of continuous semimartingales that are exponentially integrable, which includes in particular affine and some polynomial diffus...

In this paper, we propose two new algorithms, namely aHOLA and aHOLLA, to sample from high-dimensional target distributions with possibly super-linearly growing potentials. We establish non-asymptot...

In this paper, we present a randomized extension of the deep splitting algorithm introduced in [Beck, Becker, Cheridito, Jentzen, and Neufeld (2021)] using random neural networks suitable to approxi...

In this article we present a general framework for non-concave distributionally robust stochastic control problems in a discrete time finite horizon setting. Our framework allows to consider a varie...

We examine nonlinear Kolmogorov partial differential equations (PDEs). Here the nonlinear part of the PDE comes from its Hamiltonian where one maximizes over all possible drift and diffusion coeffic...

In this paper we develop a Stochastic Gradient Langevin Dynamics (SGLD) algorithm tailored for solving a certain class of non-convex distributionally robust optimisation problems. By deriving non-as...

Numerical experiments indicate that deep learning algorithms overcome the curse of dimensionality when approximating solutions of semilinear PDEs. For certain linear PDEs and semilinear PDEs with gr...

In this paper, we study random neural networks which are single-hidden-layer feedforward neural networks whose weights and biases are randomly initialized. After this random initialization, only the...

In this paper we prove that rectified deep neural networks do not suffer from the curse of dimensionality when approximating McKean--Vlasov SDEs in the sense that the number of parameters in the dee...

Neufeld and Wu (arXiv:2310.12545) developed a multilevel Picard (MLP) algorithm which can approximately solve general semilinear parabolic PDEs with gradient-dependent nonlinearities, allowing also ...

We examine optimization problems in which an investor has the opportunity to trade in $d$ stocks with the goal of maximizing her worst-case cost of cumulative gains and losses. Here, worst-case refe...

In this paper we consider PIDEs with gradient-independent Lipschitz continuous nonlinearities and prove that deep neural networks with ReLU activation function can approximate solutions of such semi...

In this paper we introduce a multilevel Picard approximation algorithm for general semilinear parabolic PDEs with gradient-dependent nonlinearities whose coefficient functions do not need to be cons...

In this note we provide an upper bound for the difference between the value function of a distributionally robust Markov decision problem and the value function of a non-robust Markov decision probl...

We propose a numerical algorithm for computing approximately optimal solutions of the matching for teams problem. Our algorithm is efficient for problems involving large number of agent categories a...

In this paper we demonstrate both theoretically as well as numerically that neural networks can detect model-free static arbitrage opportunities whenever the market admits some. Due to the use of ne...

In this paper we provide a quantum Monte Carlo algorithm to solve high-dimensional Black-Scholes PDEs with correlation for high-dimensional option pricing. The payoff function of the option is of ge...

In this paper we develop a numerical method for efficiently approximating solutions of certain Zakai equations in high dimensions. The key idea is to transform a given Zakai SPDE into a PDE with ran...

We consider the problem of sampling from a high-dimensional target distribution $\pi_\beta$ on $\mathbb{R}^d$ with density proportional to $\theta\mapsto e^{-\beta U(\theta)}$ using explicit numeric...

We introduce a general framework for Markov decision problems under model uncertainty in a discrete-time infinite horizon setting. By providing a dynamic programming principle we obtain a local-to-g...

In this paper we introduce a multilevel Picard approximation algorithm for semilinear parabolic partial integro-differential equations (PIDEs). We prove that the numerical approximation scheme conve...

We consider a general class of two-stage distributionally robust optimization (DRO) problems which includes prominent instances such as task scheduling, the assemble-to-order system, and supply chai...

We develop a new model for spatial random field reconstruction of a binary-valued spatial phenomenon. In our model, sensors are deployed in a wireless sensor network across a large geographical regi...

We show how inter-asset dependence information derived from market prices of options can lead to improved model-free price bounds for multi-asset derivatives. Depending on the type of the traded opt...

We present an approach, based on deep neural networks, that allows identifying robust statistical arbitrage strategies in financial markets. Robust statistical arbitrage strategies refer to trading ...

We propose a numerical algorithm for the computation of multi-marginal optimal transport (MMOT) problems involving general measures that are not necessarily discrete. By developing a relaxation sche...

We consider non-convex stochastic optimization problems where the objective functions have super-linearly growing and discontinuous stochastic gradients. In such a setting, we provide a non-asymptot...

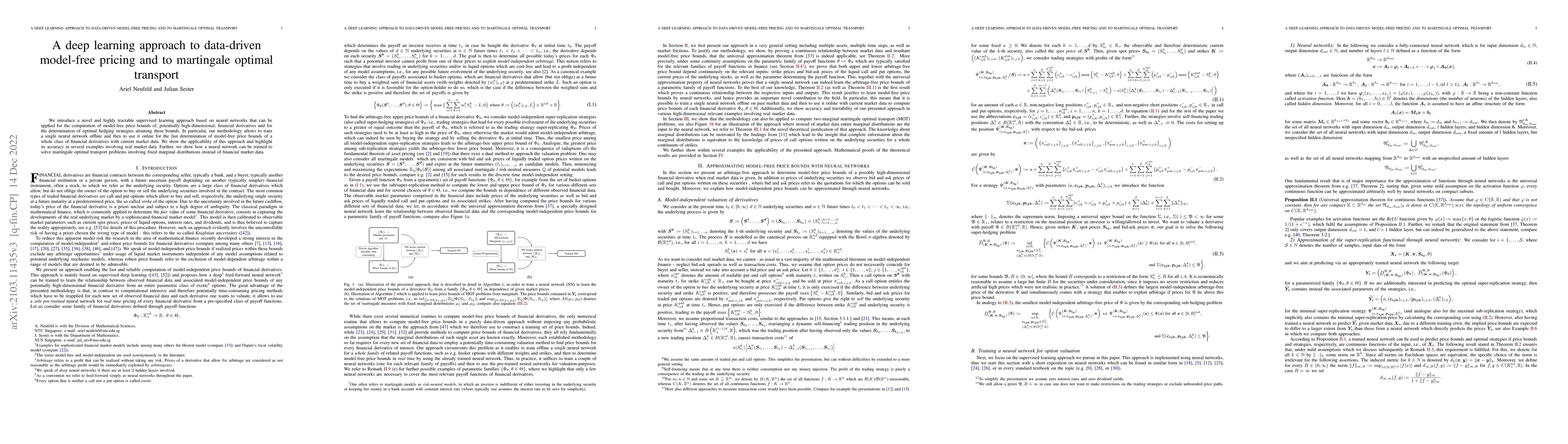

We introduce a novel and highly tractable supervised learning approach based on neural networks that can be applied for the computation of model-free price bounds of, potentially high-dimensional, f...

The cyber risk insurance market is at a nascent stage of its development, even as the magnitude of cyber losses is significant and the rate of cyber loss events is increasing. Existing cyber risk in...

In this paper we extend discrete time semi-static trading strategies by also allowing for dynamic trading in a finite amount of options, and we study the consequences for the model-independent super...

In this paper we present a duality theory for the robust utility maximisation problem in continuous time for utility functions defined on the positive real axis. Our results are inspired by -- and c...

We consider derivatives written on multiple underlyings in a one-period financial market, and we are interested in the computation of model-free upper and lower bounds for their arbitrage-free price...

In this paper we introduce a numerical method for nonlinear parabolic PDEs that combines operator splitting with deep learning. It divides the PDE approximation problem into a sequence of separate l...

The goal of this paper is to define stochastic integrals and to solve stochastic differential equations for typical paths taking values in a possibly infinite dimensional separable Hilbert space wit...

Stochastic gradient descent (SGD) optimization algorithms are key ingredients in a series of machine learning applications. In this article we perform a rigorous strong error analysis for SGD optimi...

In this paper we provide a pricing-hedging duality for the model-independent superhedging price with respect to a prediction set $\Xi\subseteq C[0,T]$, where the superhedging property needs to hold ...

In this paper, we provide a non-asymptotic analysis of the convergence of the stochastic gradient Hamiltonian Monte Carlo (SGHMC) algorithm to a target measure in Wasserstein-1 and Wasserstein-2 dista...

We prove that multilevel Picard approximations and deep neural networks with ReLU, leaky ReLU, and softplus activation are capable of approximating solutions of semilinear Kolmogorov PDEs in $L^\mathf...

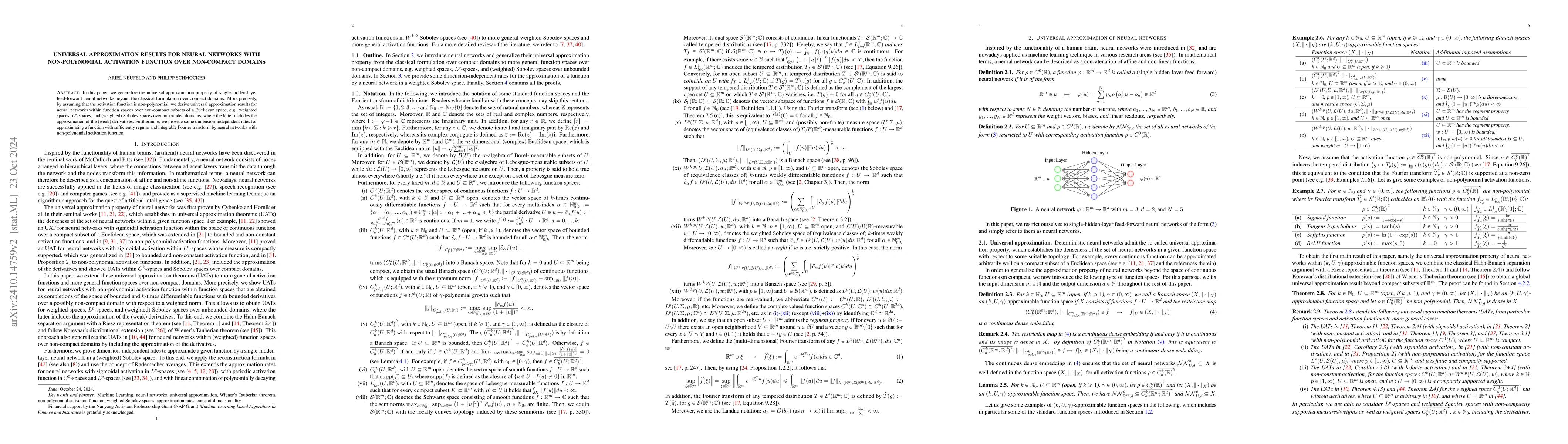

In this paper, we generalize the universal approximation property of single-hidden-layer feed-forward neural networks beyond the classical formulation over compact domains. More precisely, by assuming...

In this paper, we solve stochastic partial differential equations (SPDEs) numerically by using (possibly random) neural networks in the truncated Wiener chaos expansion of their corresponding solution...

We propose and analyze a framework for mean-field Markov games under model uncertainty. In this framework, a state-measure flow describing the collective behavior of a population affects the given rew...

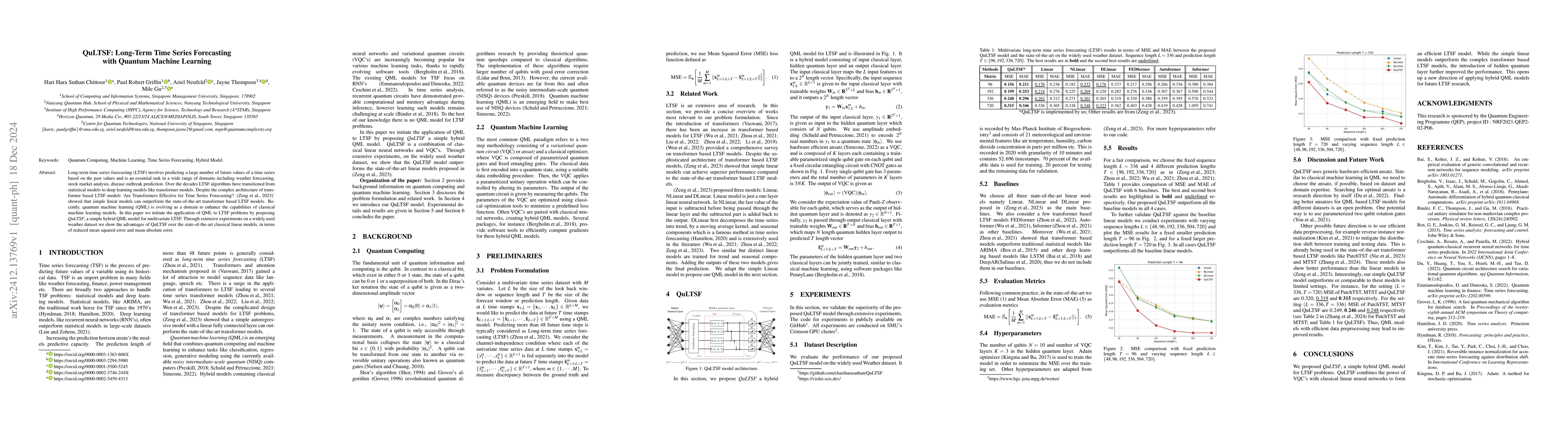

Long-term time series forecasting (LTSF) involves predicting a large number of future values of a time series based on the past values and is an essential task in a wide range of domains including wea...

We introduce multilevel Picard (MLP) approximations for McKean-Vlasov stochastic differential equations (SDEs) with nonconstant diffusion coefficient. Under standard Lipschitz assumptions on the coeff...

We propose a provably convergent algorithm for approximating the 2-Wasserstein barycenter of continuous non-parametric probability measures. Our algorithm is inspired by the fixed-point iterative sche...

Neural operators (NOs) are a class of deep learning models designed to simultaneously solve infinitely many related problems by casting them into an infinite-dimensional space, whereon these NOs opera...

Quantum neural networks (QNNs) are an analog of classical neural networks in the world of quantum computing, which are represented by a unitary matrix with trainable parameters. Inspired by the univer...

We examine the scaling limit of multi-period distributionally robust optimization (DRO) problems via a semigroup approach. Each period involves a worst-case maximization over distributions in a Wasser...

We propose and analyze a framework for discrete-time robust mean-field control problems under common noise uncertainty. In this framework, the mean-field interaction describes the collective behavior ...

In this article, we present a robust $Q$-learning algorithm for discrete-time mean-field control problems under Wasserstein uncertainty in the common noise law. The algorithm combines a quantization-a...