Academic Profile

Statistics

Similar Authors

Papers on arXiv

Conditional forecasts, i.e. projections of a set of variables of interest on the future paths of some other variables, are used routinely by empirical macroeconomists in a number of applied settings...

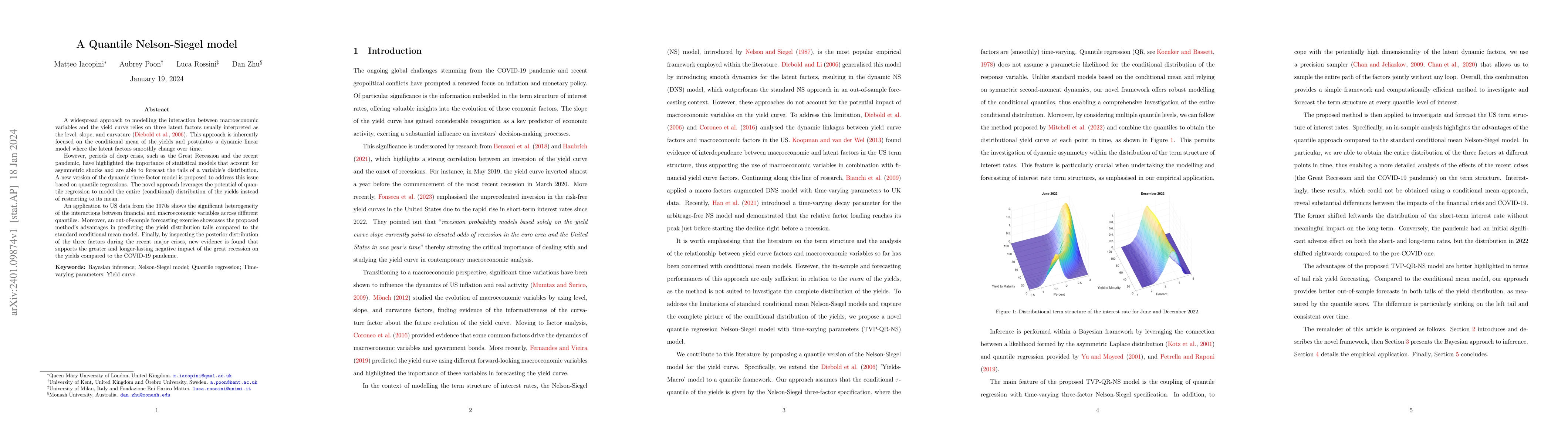

A widespread approach to modelling the interaction between macroeconomic variables and the yield curve relies on three latent factors usually interpreted as the level, slope, and curvature (Diebold ...

An innovative method is proposed to construct a quantile dependence system for inflation and money growth. By considering all quantiles and leveraging a novel notion of quantile sensitivity, the met...

We develop an efficient sampling approach for handling complex missing data patterns and a large number of missing observations in conditionally Gaussian state space models. Two important examples a...

Timely characterizations of risks in economic and financial systems play an essential role in both economic policy and private sector decisions. However, the informational content of low-frequency v...

State-space mixed-frequency vector autoregressions are now widely used for nowcasting. Despite their popularity, estimating such models can be computationally intensive, especially for large systems...