Academic Profile

Statistics

Similar Authors

Papers on arXiv

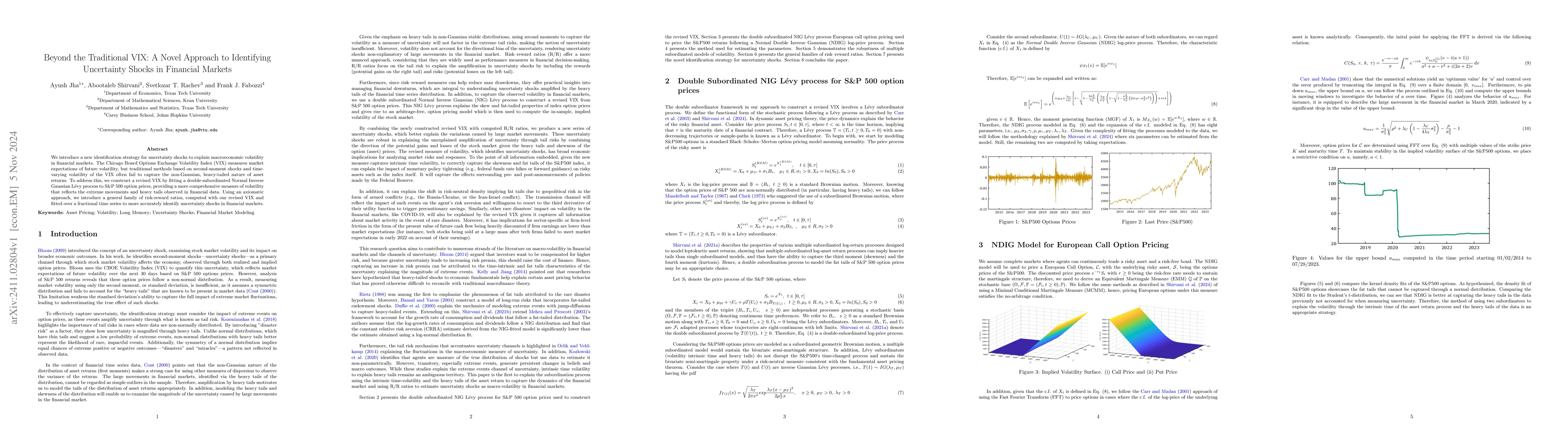

We introduce a new identification strategy for uncertainty shocks to explain macroeconomic volatility in financial markets. The Chicago Board Options Exchange Volatility Index (VIX) measures market ex...

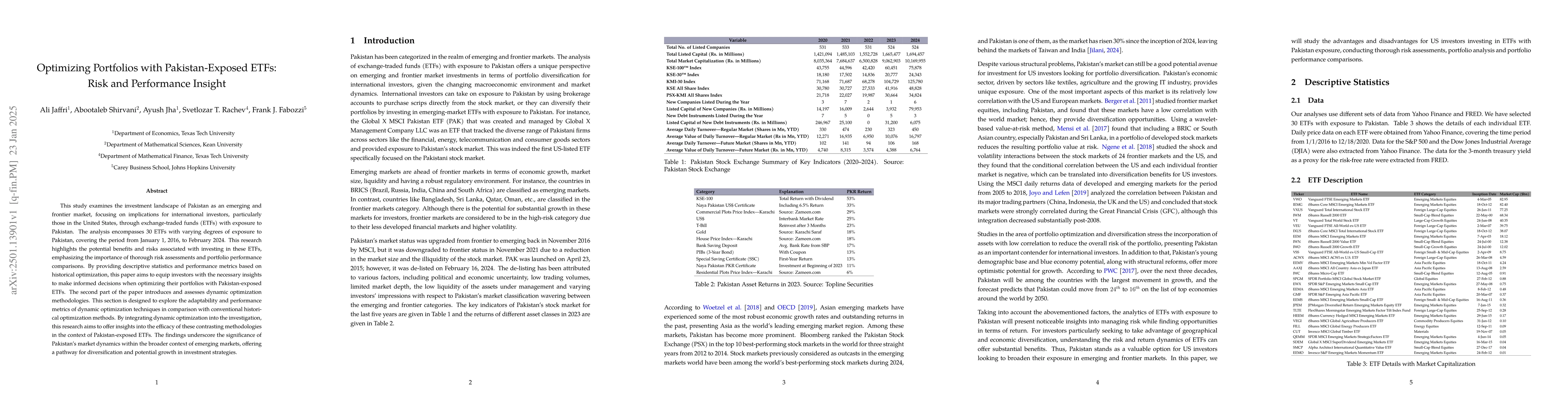

This study examines the investment landscape of Pakistan as an emerging and frontier market, focusing on implications for international investors, particularly those in the United States, through exch...

This study presents the Adaptive Minimum-Variance Portfolio (AMVP) framework and the Adaptive Minimum-Risk Rate (AMRR) metric, innovative tools designed to optimize portfolios dynamically in volatile ...

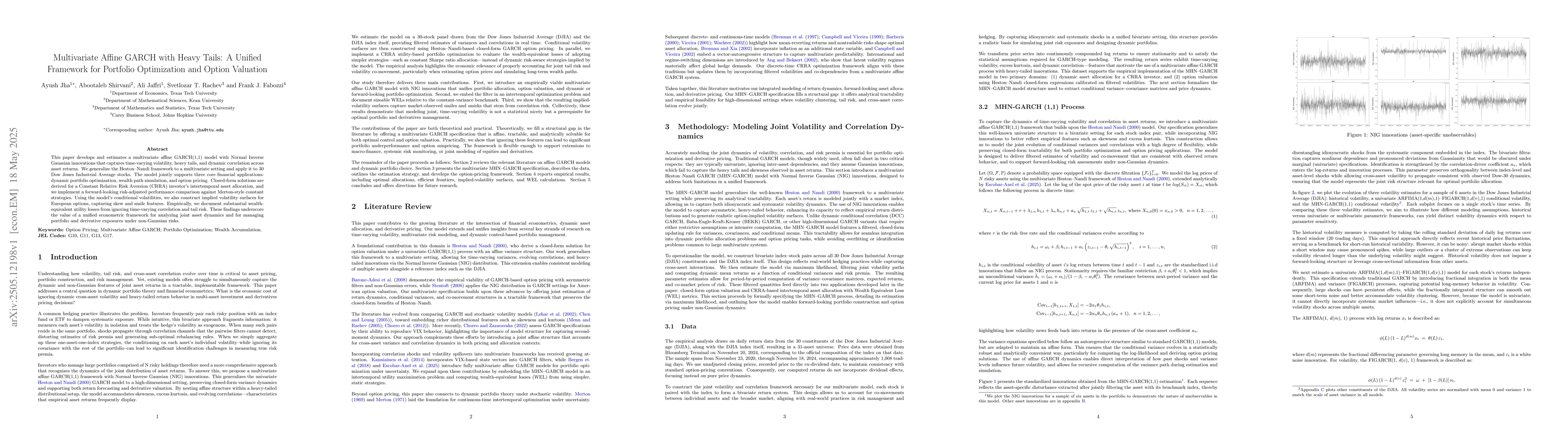

This paper develops and estimates a multivariate affine GARCH(1,1) model with Normal Inverse Gaussian innovations that captures time-varying volatility, heavy tails, and dynamic correlation across ass...

This paper introduces a state-dependent momentum framework that integrates ESG regime switching with tail-risk-aware reward-risk metrics. Using a dynamic programming approach and solving a finite-hori...

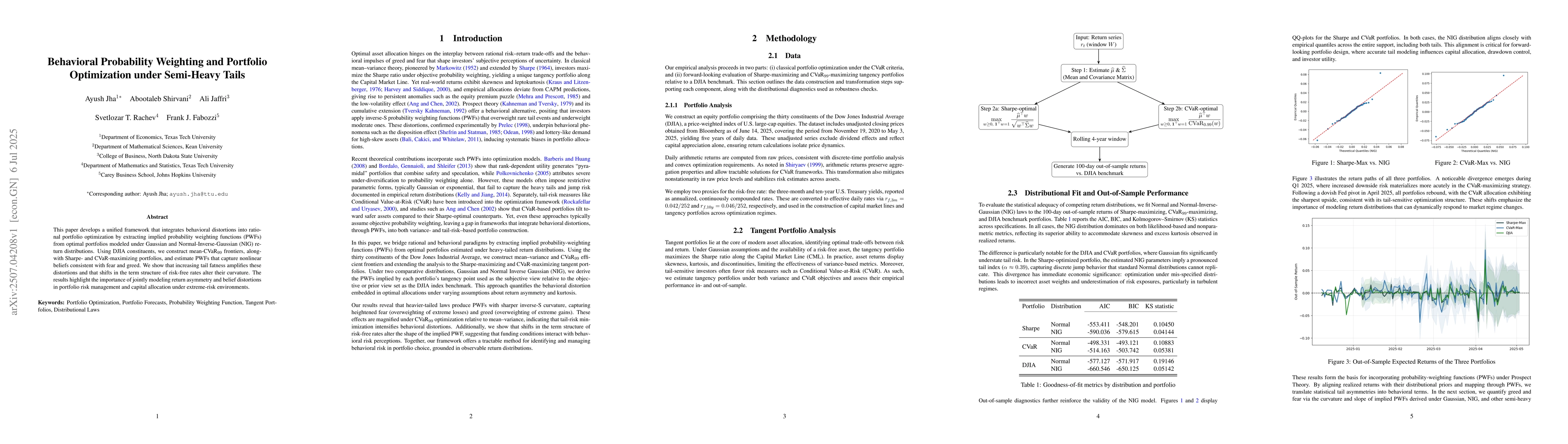

This paper develops a unified framework that integrates behavioral distortions into rational portfolio optimization by extracting implied probability weighting functions (PWFs) from optimal portfolios...

With the advancement of millimeter-wave radar technology, Synthetic Aperture Radar (SAR) imaging at millimeter-wave frequencies has gained significant attention in both academic research and industria...

We develop a partial integro-differential equation (PIDE) framework for option pricing under joint stochastic volatility and jump dynamics, and evaluate its empirical content using the S&P500 index op...

Why do similar funding shocks generate sharply different credit outcomes across countries? We develop and estimate a dynamic structural model in which intermediary credit capacity governs the transmis...

Predictive dependence in time series need not be confined to the conditional mean. Outside the Gaussian setting, causal content may arise through conditional scale, tail behavior, asymmetry, or other ...