This paper develops and estimates a multivariate affine GARCH(1,1) model with

Normal Inverse Gaussian innovations that captures time-varying volatility,

heavy tails, and dynamic correlation across asset returns. We generalize the

Heston-Nandi framework to a multivariate setting and apply it to 30 Dow Jones

Industrial Average stocks. The model jointly supports three core financial

applications: dynamic portfolio optimization, wealth path simulation, and

option pricing. Closed-form solutions are derived for a Constant Relative Risk

Aversion (CRRA) investor's intertemporal asset allocation, and we implement a

forward-looking risk-adjusted performance comparison against Merton-style

constant strategies. Using the model's conditional volatilities, we also

construct implied volatility surfaces for European options, capturing skew and

smile features. Empirically, we document substantial wealth-equivalent utility

losses from ignoring time-varying correlation and tail risk. These findings

underscore the value of a unified econometric framework for analyzing joint

asset dynamics and for managing portfolio and derivative exposures under

non-Gaussian risks.

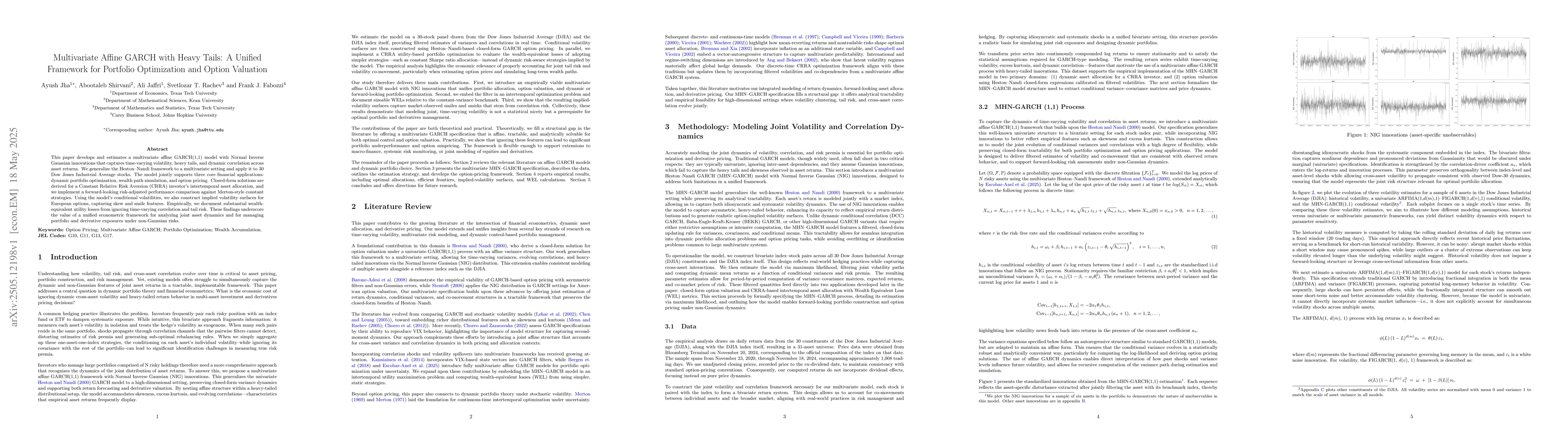

Discussion 0