Academic Profile

Statistics

Similar Authors

Papers on arXiv

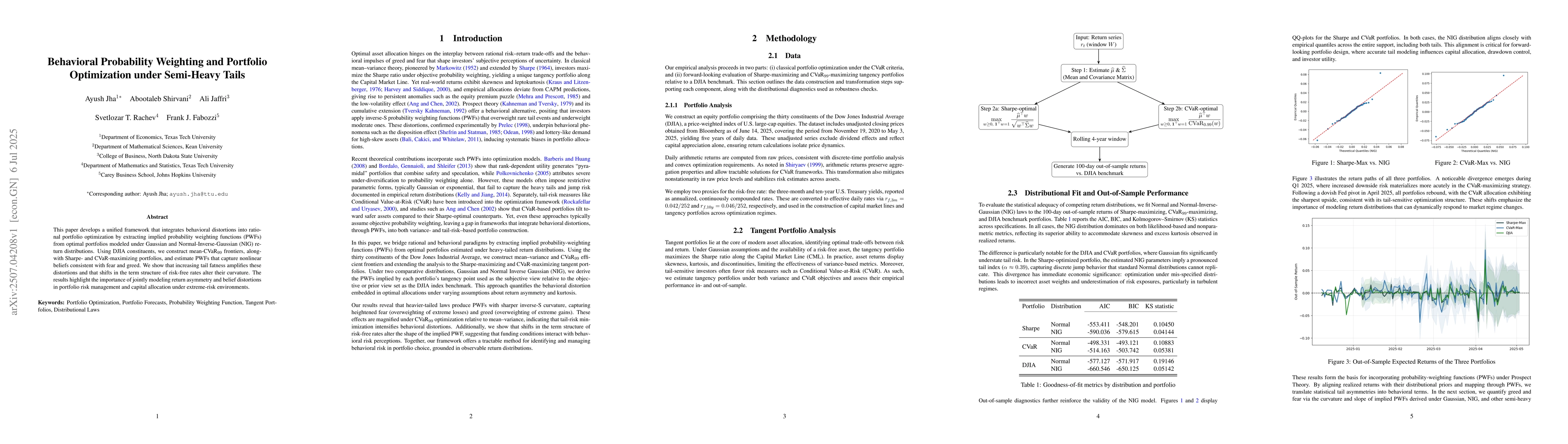

In complete markets, there are risky assets and a riskless asset. It is assumed that the riskless asset and the risky asset are traded continuously in time and that the market is frictionless. In th...

We present a unified, market-complete model that integrates both the Bachelier and Black-Scholes-Merton frameworks for asset pricing. The model allows for the study, within a unified framework, of a...

Using data from 2000 through 2022, we analyze the predictive capability of the annual numbers of new home constructions and four available environmental, social, and governance factors on the averag...

We develop two alternate approaches to arbitrage-free, market-complete, option pricing. The first approach requires no riskless asset. We develop the general framework for this approach and illustra...

We propose a discrete-time econometric model that combines autoregressive filters with factor regressions to predict stock returns for portfolio optimisation purposes. In particular, we test both ro...

The growing interest in sustainable investing calls for an axiomatic approach to measures of risk and reward that focus not only on financial returns, but also on measures of environmental and socia...

We introduce a discrete binary tree for pricing contingent claims with the underlying security prices exhibiting history dependence characteristic of that induced by market microstructure phenomena....

Motivated by the Corns-Satchell, continuous time, option pricing model, we develop a binary tree pricing model with underlying asset price dynamics following It\^o-Mckean skew Brownian motion. While...

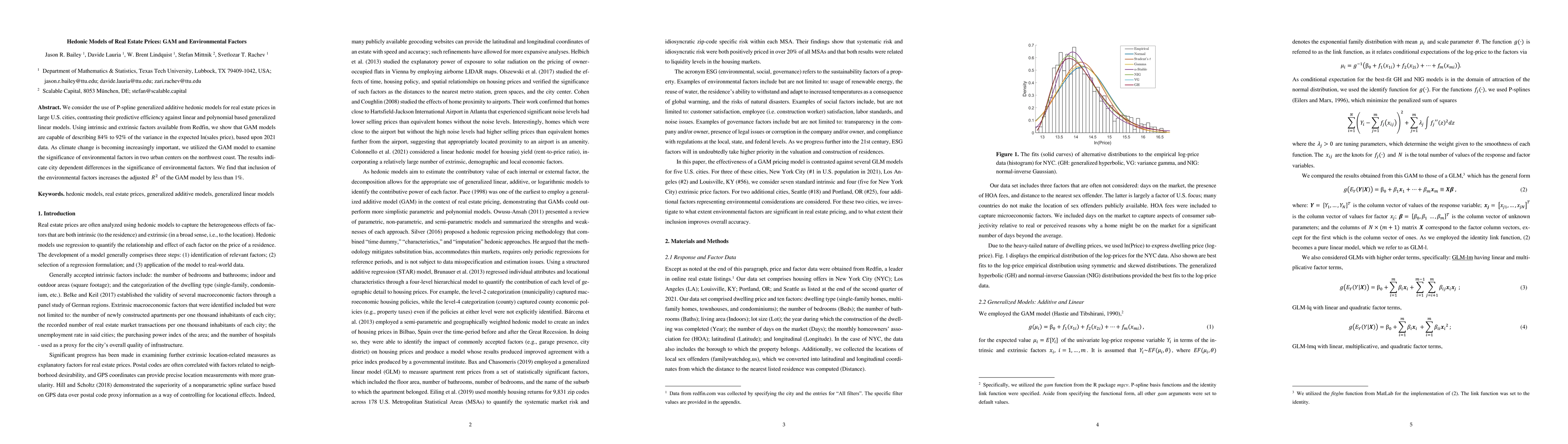

We consider the use of P-spline generalized additive hedonic models for real estate prices in large U.S. cities, contrasting their predictive efficiency against linear and polynomial based generaliz...

We consider option pricing using replicating binomial trees, with a two fold purpose. The first is to introduce ESG valuation into option pricing. We explore this in a number of scenarios, including...

ESG ratings provide a quantitative measure for socially responsible investment. We present a unified framework for incorporating numeric ESG ratings into dynamic pricing theory. Specifically, we int...

The paper Zhao et al. (2015) shows that mean-CVaR-skewness portfolio optimization problems based on asymetric Laplace (AL) distributions can be transformed into quadratic optimization problems under...

We propose a doubly subordinated Levy process, NDIG, to model the time series properties of the cryptocurrency bitcoin. NDIG captures the skew and fat-tailed properties of bitcoin prices and gives r...

Applying the Cherny-Shiryaev-Yor invariance principle, we introduce a generalized Jarrow-Rudd (GJR) option pricing model with uncertainty driven by a skew random walk. The GJR pricing tree exhibits ...

Measures of tail dependence between random variables aim to numerically quantify the degree of association between their extreme realizations. Existing tail dependence coefficients (TDCs) are based ...

Using the Donsker-Prokhorov invariance principle we extend the Kim-Stoyanov-Rachev-Fabozzi option pricing model to allow for variably-spaced trading instances, an important consideration for short-s...

The objective of this paper is to introduce the theory of option pricing for markets with informed traders within the framework of dynamic asset pricing theory. We introduce new models for option pr...

In this paper, we address one of the main puzzles in finance observed in the stock market by proponents of behavioral finance: the stock predictability puzzle. We offer a statistical model within th...

In this paper, we revisit the equity premium puzzle reported in 1985 by Mehra and Prescott. We show that the large equity premium that they report can be explained by choosing a more appropriate dis...

Despite being described as a medium of exchange, cryptocurrencies do not have the typical attributes of a medium of exchange. Consequently, cryptocurrencies are more appropriately described as crypt...

Subordination is an often used stochastic process in modeling asset prices. Subordinated Levy price processes and local volatility price processes are now the main tools in modern dynamic asset pric...

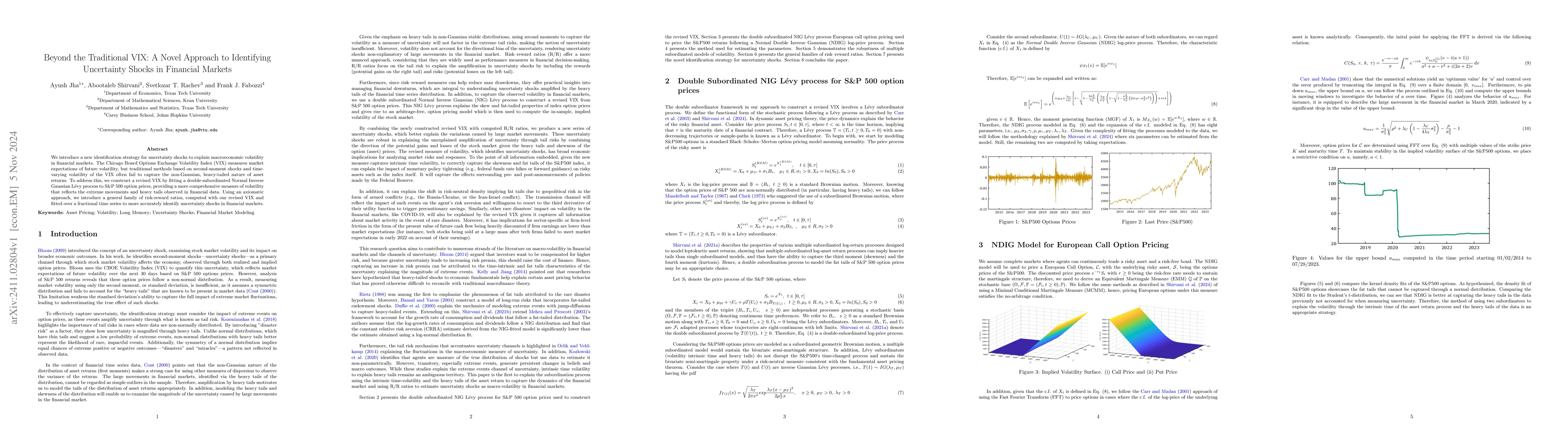

We introduce a new identification strategy for uncertainty shocks to explain macroeconomic volatility in financial markets. The Chicago Board Options Exchange Volatility Index (VIX) measures market ex...

We address the problem of asset pricing in a market where there is no risky asset. Previous work developed a theoretical model for a shadow riskless rate (SRR) for such a market in terms of the drift ...

We introduce a fairly general, recombining trinomial tree model in the natural world. Market-completeness is ensured by considering a market consisting of two risky assets, a riskless asset, and a Eur...

This paper studies the properties of the Multiply Iterated Poisson Process (MIPP), a stochastic process constructed by repeatedly time-changing a Poisson process, and its applications in ruin theory. ...

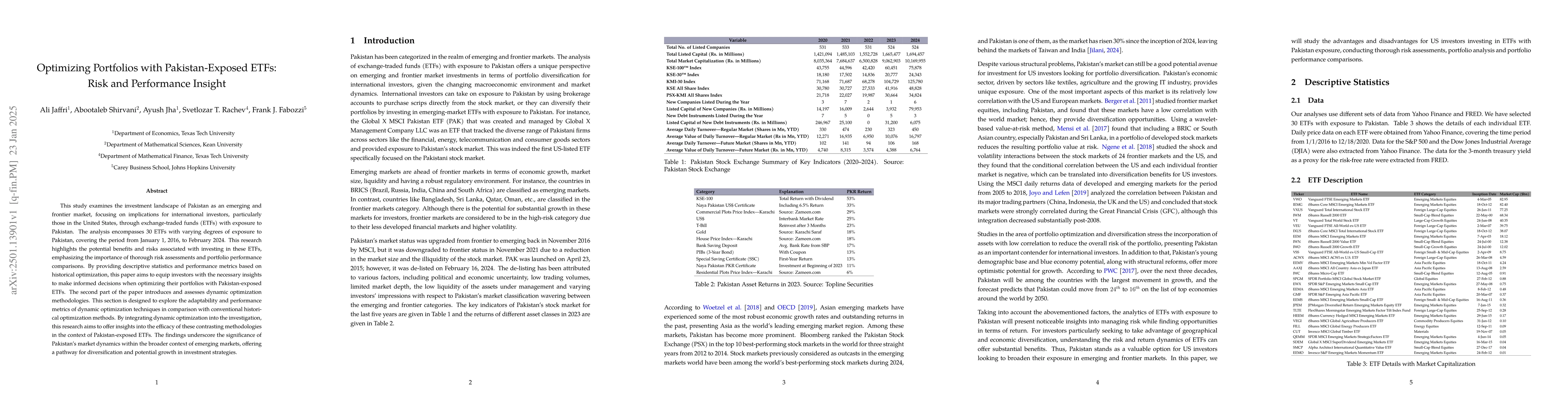

This study examines the investment landscape of Pakistan as an emerging and frontier market, focusing on implications for international investors, particularly those in the United States, through exch...

This study presents the Adaptive Minimum-Variance Portfolio (AMVP) framework and the Adaptive Minimum-Risk Rate (AMRR) metric, innovative tools designed to optimize portfolios dynamically in volatile ...

This paper develops and estimates a multivariate affine GARCH(1,1) model with Normal Inverse Gaussian innovations that captures time-varying volatility, heavy tails, and dynamic correlation across ass...

This paper introduces a state-dependent momentum framework that integrates ESG regime switching with tail-risk-aware reward-risk metrics. Using a dynamic programming approach and solving a finite-hori...

We explore credit risk pricing by modeling equity as a call option and debt as the difference between the firm's asset value and a put option, following the structural framework of the Merton model. O...

This paper develops a unified framework that integrates behavioral distortions into rational portfolio optimization by extracting implied probability weighting functions (PWFs) from optimal portfolios...

We propose a machine learning-based extension of the classical binomial option pricing model that incorporates key market microstructure effects. Traditional models assume frictionless markets, overlo...

We extend the application of the Cherny-Shiryaev-Yor invariance principle to a unified Bachelier-Black-Scholes-Merton (BBSM) dynamic pricing model. This extension incorporates the influence of the his...

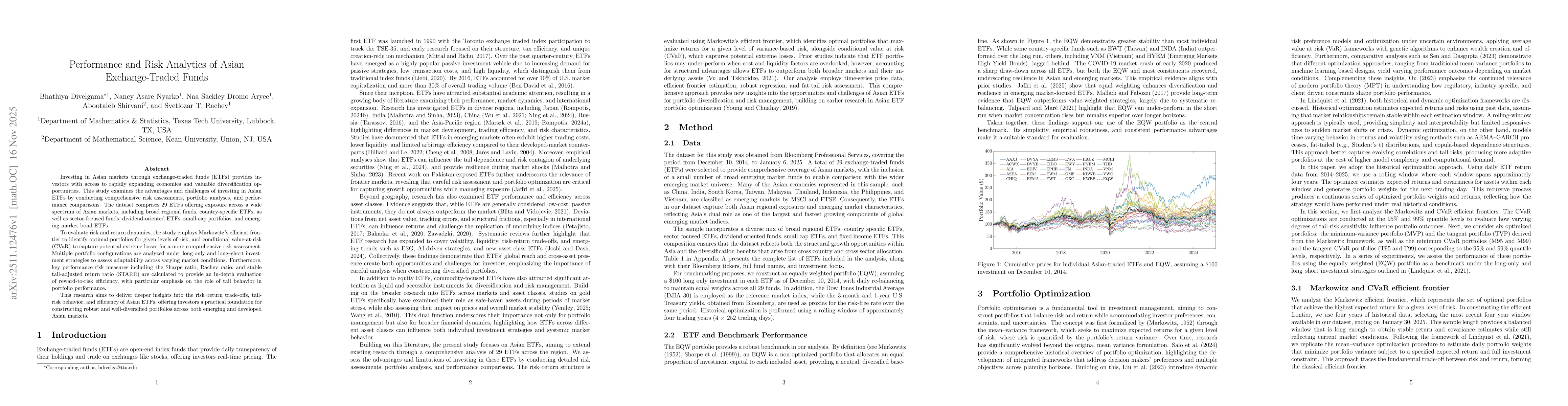

Investing in Asian markets through exchange-traded funds (ETFs) provides investors with access to rapidly expanding economies and valuable diversification opportunities. This study examines the advant...

We develop an econometric framework integrating heavy-tailed Student's $t$ distributions with behavioral probability weighting while preserving infinite divisibility. Using 432{,}752 observations acro...

We present two models for incorporating the total effect of market microstructure noise into dynamic pricing of assets and European options. The first model is developed under a Black-Scholes-Merton, ...

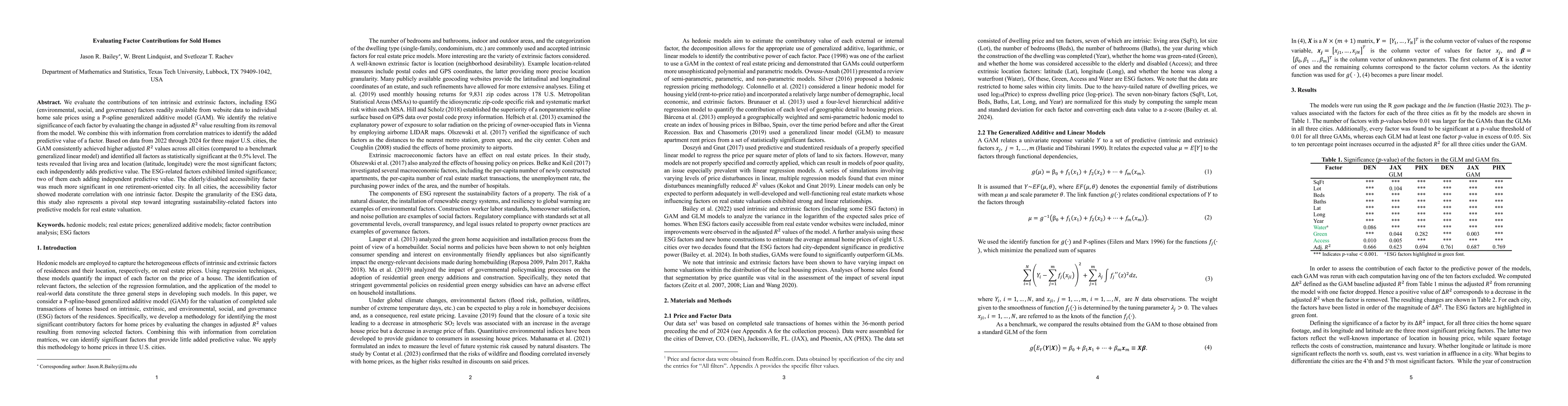

We evaluate the contributions of ten intrinsic and extrinsic factors, including ESG (environmental, social, and governance) factors readily available from website data to individual home sale prices u...

This paper develops a three-dimensional decomposition of volatility memory into orthogonal components of level, shape, and tempo. The framework unifies regime-switching, fractional-integration, and bu...

This paper addresses a critical inconsistency in models of the term structure of interest rates (TSIR), where zero-coupon bonds are priced under risk-neutral measures distinct from those used in equit...

This paper studies the joint role of long-memory dynamics,rough-volatility behavior, and persistence-based forecasting features in equity volatility modeling. We combine semiparametric long-memory est...

We develop a partial integro-differential equation (PIDE) framework for option pricing under joint stochastic volatility and jump dynamics, and evaluate its empirical content using the S&P500 index op...

Classical option pricing models, such as Bachelier and Black--Scholes--Merton, postulate symmetric Brownian diffusion, which limits their capacity to reflect empirical phenomena including return skewn...

This paper examines portfolio optimization for commodity exchange-traded funds (ETFs) under heavy-tailed return behavior. Using daily Bloomberg data for 30 U.S.-listed commodity ETFs from 12 December ...

This paper examines portfolio optimization and tail-risk analytics for a heterogeneous universe of actively managed investment funds. Using daily Bloomberg data for 30 funds from 4 December 2020 to 24...