Academic Profile

Statistics

Similar Authors

Papers on arXiv

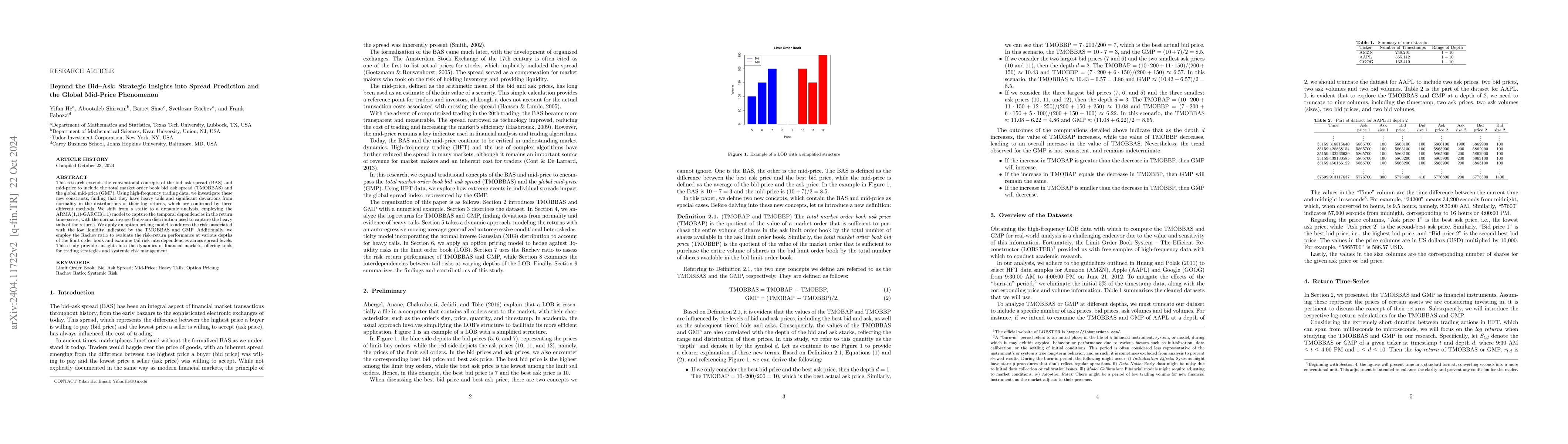

This study introduces novel concepts in the analysis of limit order books (LOBs) with a focus on unveiling strategic insights into spread prediction and understanding the global mid-price (GMP) phen...

This paper introduces the concept of a global financial market for environmental indices, addressing sustainability concerns and aiming to attract institutional investors. Risk mitigation measures a...

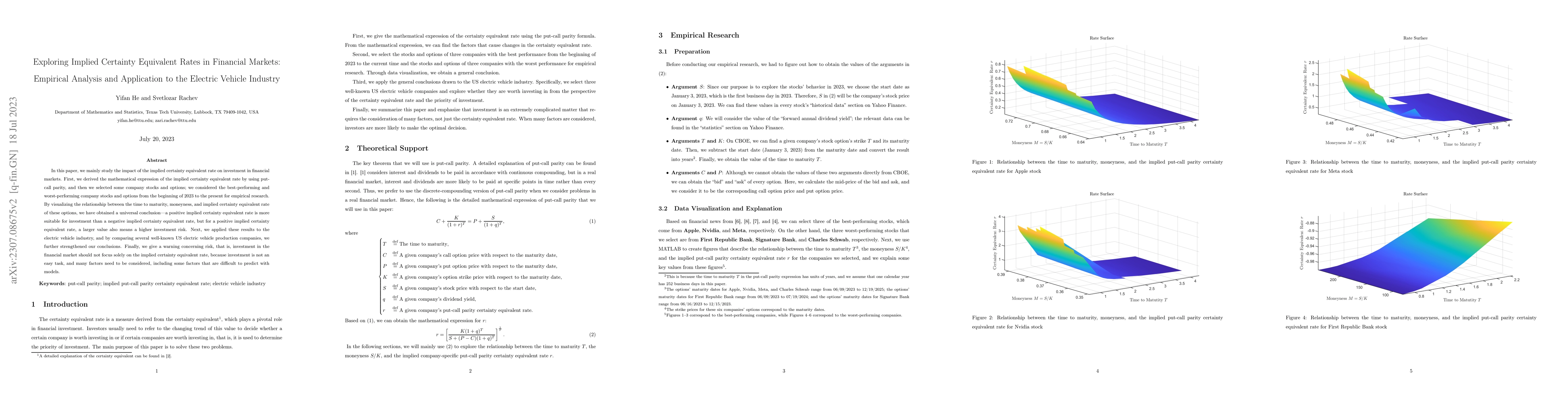

In this paper, we mainly study the impact of the implied certainty equivalent rate on investment in financial markets. First, we derived the mathematical expression of the implied certainty equivale...

This paper delves into the dynamics of asset pricing within Bachelier market model, elucidating the representation of risky asset price dynamics and the definition of riskless assets.

This study delves into the temporal dynamics within the equity market through the lens of bond traders. Recognizing that the riskless interest rate fluctuates over time, we leverage the Black-Derman...

Environmental, Social, and Governance (ESG) finance is a cornerstone of modern finance and investment, as it changes the classical return-risk view of investment by incorporating an additional dimen...

The financial industry should be involved in mitigating the risk of downturns in the financial wellbeing indices around the world by implementing well-developed financial tools such as insurance ins...

Crime can have a volatile impact on investments. Despite the potential importance of crime rates in investments, there are no indices dedicated to evaluating the financial impact of crime in the Uni...

We explain the main concepts of Prospect Theory and Cumulative Prospect Theory within the framework of rational dynamic asset pricing theory. We derive option pricing formulas when asset returns are...

This study evaluates the performance of random forest regression models enhanced with technical indicators for high-frequency stock price prediction. Using minute-level SPY data, we assessed 13 models...

This study presents a comprehensive empirical investigation of the presence of long-range dependence (LRD) in the dynamics of major U.S. stock market indexes--S\&P 500, Dow Jones, and Nasdaq--at daily...

This paper considers an optimal control problem for a linear mean-field stochastic differential equation having regime switching with quadratic functional in the large time horizons. Our main contribu...

We introduce a simple portfolio optimization strategy using ESG data with the Black-Litterman allocation framework. ESG scores are used as a bias for Stein shrinkage estimation of equilibrium risk pre...