Academic Profile

Statistics

Similar Authors

Papers on arXiv

In complete markets, there are risky assets and a riskless asset. It is assumed that the riskless asset and the risky asset are traded continuously in time and that the market is frictionless. In th...

We present a unified, market-complete model that integrates both the Bachelier and Black-Scholes-Merton frameworks for asset pricing. The model allows for the study, within a unified framework, of a...

This paper introduces the concept of a global financial market for environmental indices, addressing sustainability concerns and aiming to attract institutional investors. Risk mitigation measures a...

Motivated by the Corns-Satchell, continuous time, option pricing model, we develop a binary tree pricing model with underlying asset price dynamics following It\^o-Mckean skew Brownian motion. While...

Applying the Cherny-Shiryaev-Yor invariance principle, we introduce a generalized Jarrow-Rudd (GJR) option pricing model with uncertainty driven by a skew random walk. The GJR pricing tree exhibits ...

Using the Donsker-Prokhorov invariance principle we extend the Kim-Stoyanov-Rachev-Fabozzi option pricing model to allow for variably-spaced trading instances, an important consideration for short-s...

The objective of this paper is to introduce the theory of option pricing for markets with informed traders within the framework of dynamic asset pricing theory. We introduce new models for option pr...

When pricing options, there may be different views on the instantaneous mean return of the underlying price process. According to Black (1972), where there exist heterogeneous views on the instantan...

Proponents of behavioral finance have identified several "puzzles" in the market that are inconsistent with rational finance theory. One such puzzle is the "excess volatility puzzle". Changes in equ...

In this paper, we combine modern portfolio theory and option pricing theory so that a trader who takes a position in a European option contract and the underlying assets can construct an optimal por...

In this paper, we address one of the main puzzles in finance observed in the stock market by proponents of behavioral finance: the stock predictability puzzle. We offer a statistical model within th...

In this paper, we revisit the equity premium puzzle reported in 1985 by Mehra and Prescott. We show that the large equity premium that they report can be explained by choosing a more appropriate dis...

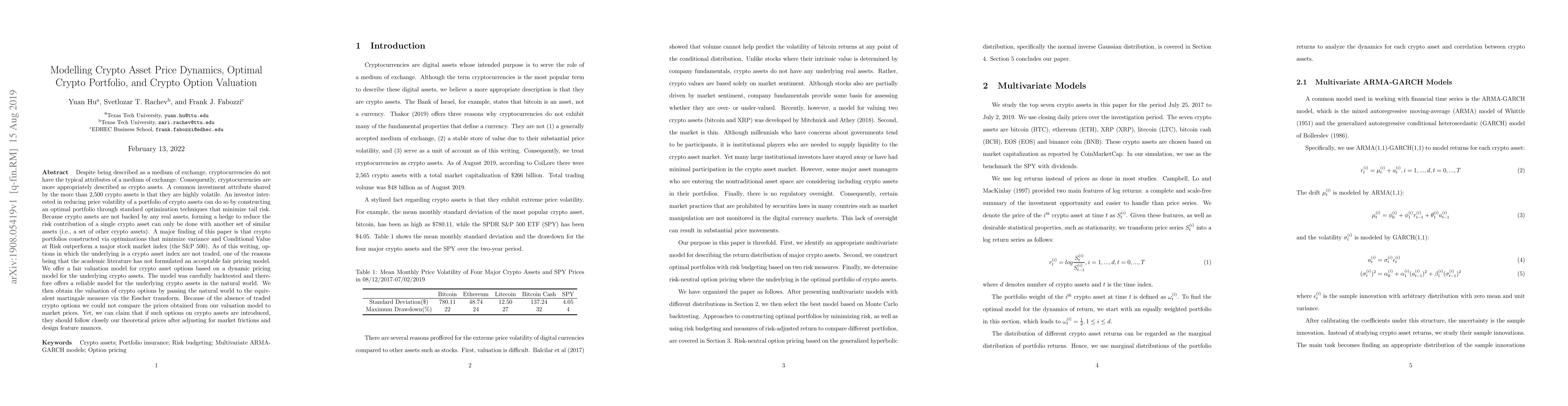

Despite being described as a medium of exchange, cryptocurrencies do not have the typical attributes of a medium of exchange. Consequently, cryptocurrencies are more appropriately described as crypt...

Subordination is an often used stochastic process in modeling asset prices. Subordinated Levy price processes and local volatility price processes are now the main tools in modern dynamic asset pric...

We explain the main concepts of Prospect Theory and Cumulative Prospect Theory within the framework of rational dynamic asset pricing theory. We derive option pricing formulas when asset returns are...

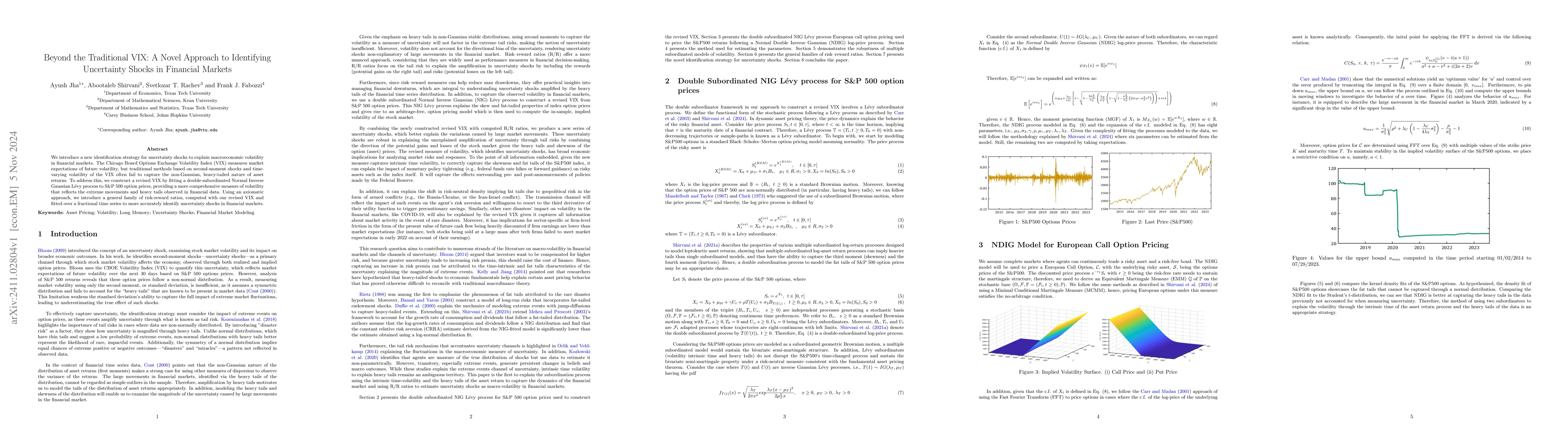

We introduce a new identification strategy for uncertainty shocks to explain macroeconomic volatility in financial markets. The Chicago Board Options Exchange Volatility Index (VIX) measures market ex...

We address the problem of asset pricing in a market where there is no risky asset. Previous work developed a theoretical model for a shadow riskless rate (SRR) for such a market in terms of the drift ...

This study evaluates the performance of random forest regression models enhanced with technical indicators for high-frequency stock price prediction. Using minute-level SPY data, we assessed 13 models...

This study examines the investment landscape of Pakistan as an emerging and frontier market, focusing on implications for international investors, particularly those in the United States, through exch...

This study presents the Adaptive Minimum-Variance Portfolio (AMVP) framework and the Adaptive Minimum-Risk Rate (AMRR) metric, innovative tools designed to optimize portfolios dynamically in volatile ...

This paper develops and estimates a multivariate affine GARCH(1,1) model with Normal Inverse Gaussian innovations that captures time-varying volatility, heavy tails, and dynamic correlation across ass...

This paper introduces a state-dependent momentum framework that integrates ESG regime switching with tail-risk-aware reward-risk metrics. Using a dynamic programming approach and solving a finite-hori...

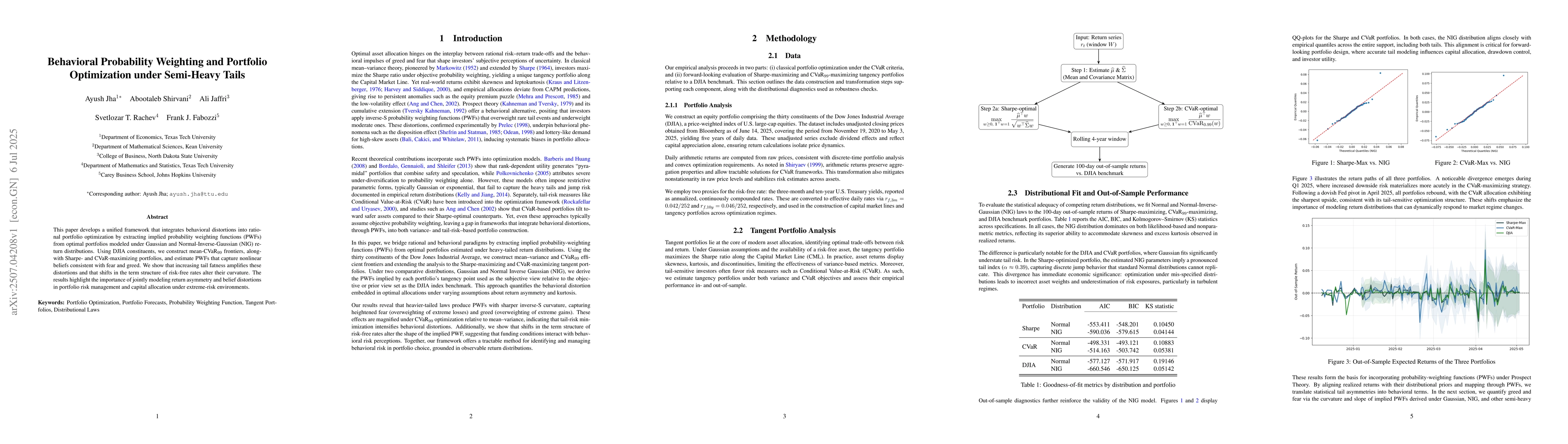

This paper develops a unified framework that integrates behavioral distortions into rational portfolio optimization by extracting implied probability weighting functions (PWFs) from optimal portfolios...

We propose a machine learning-based extension of the classical binomial option pricing model that incorporates key market microstructure effects. Traditional models assume frictionless markets, overlo...

We develop an econometric framework integrating heavy-tailed Student's $t$ distributions with behavioral probability weighting while preserving infinite divisibility. Using 432{,}752 observations acro...

We develop a partial integro-differential equation (PIDE) framework for option pricing under joint stochastic volatility and jump dynamics, and evaluate its empirical content using the S&P500 index op...

Classical option pricing models, such as Bachelier and Black--Scholes--Merton, postulate symmetric Brownian diffusion, which limits their capacity to reflect empirical phenomena including return skewn...

This paper examines portfolio optimization and tail-risk analytics for a heterogeneous universe of actively managed investment funds. Using daily Bloomberg data for 30 funds from 4 December 2020 to 24...