Academic Profile

Statistics

Similar Authors

Papers on arXiv

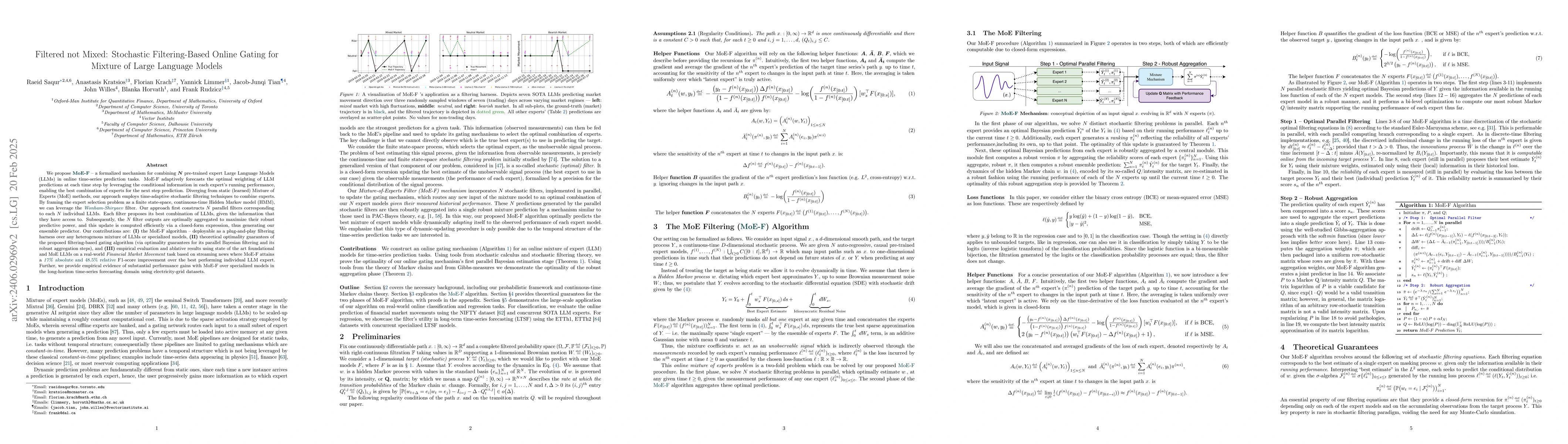

We propose MoE-F -- a formalised mechanism for combining $N$ pre-trained expert Large Language Models (LLMs) in online time-series prediction tasks by adaptively forecasting the best weighting of LL...

One of the inherent challenges in deploying transformers on time series is that \emph{reality only happens once}; namely, one typically only has access to a single trajectory of the data-generating ...

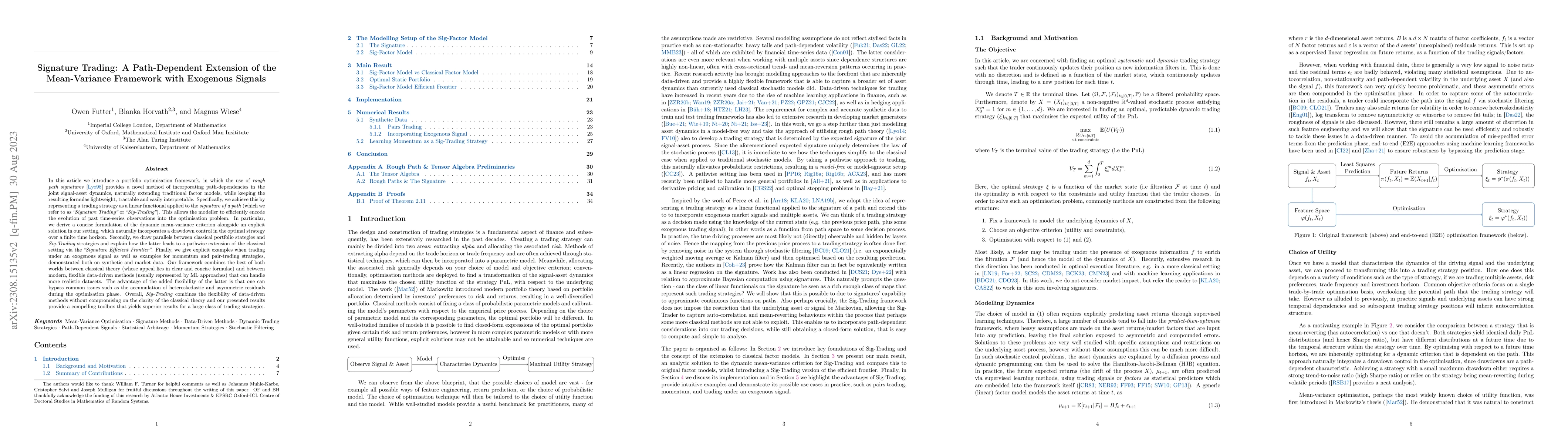

In this article we introduce a portfolio optimisation framework, in which the use of rough path signatures (Lyons, 1998) provides a novel method of incorporating path-dependencies in the joint signa...

The availability of deep hedging has opened new horizons for solving hedging problems under a large variety of realistic market conditions. At the same time, any model - be it a traditional stochast...

In this work we present a non-parametric online market regime detection method for multidimensional data structures using a path-wise two-sample test derived from a maximum mean discrepancy-based si...

Neural SDEs are continuous-time generative models for sequential data. State-of-the-art performance for irregular time series generation has been previously obtained by training these models adversa...

Distribution Regression on path-space refers to the task of learning functions mapping the law of a stochastic process to a scalar target. The learning procedure based on the notion of path-signatur...

The problem of rapid and automated detection of distinct market regimes is a topic of great interest to financial mathematicians and practitioners alike. In this paper, we outline an unsupervised le...

In this chapter we first briefly review the existing approaches to hedging in rough volatility models. Next, we present a simple but general result which shows that in a one-factor rough stochastic ...

We investigate the performance of the Deep Hedging framework under training paths beyond the (finite dimensional) Markovian setup. In particular we analyse the hedging performance of the original ar...

Neural network based data-driven market simulation unveils a new and flexible way of modelling financial time series without imposing assumptions on the underlying stochastic dynamics. Though in thi...

Techniques from deep learning play a more and more important role for the important task of calibration of financial models. The pioneering paper by Hernandez [Risk, 2017] was a catalyst for resurfa...

We present a neural network based calibration method that performs the calibration task within a few milliseconds for the full implied volatility surface. The framework is consistently applicable th...

The non-Markovian nature of rough volatility processes makes Monte Carlo methods challenging and it is in fact a major challenge to develop fast and accurate simulation algorithms. We provide an eff...

Distribution Regression (DR) on stochastic processes describes the learning task of regression on collections of time series. Path signatures, a technique prevalent in stochastic analysis, have been u...

Maximum Mean Discrepancy (MMD) is a widely used concept in machine learning research which has gained popularity in recent years as a highly effective tool for comparing (finite-dimensional) distribut...

This paper addresses the challenge of model uncertainty in quantitative finance, where decisions in portfolio allocation, derivative pricing, and risk management rely on estimating stochastic models f...

In this article, we develop a kernel-based framework for constructing dynamic, pathdependent trading strategies under a mean-variance optimisation criterion. Building on the theoretical results of (Mu...

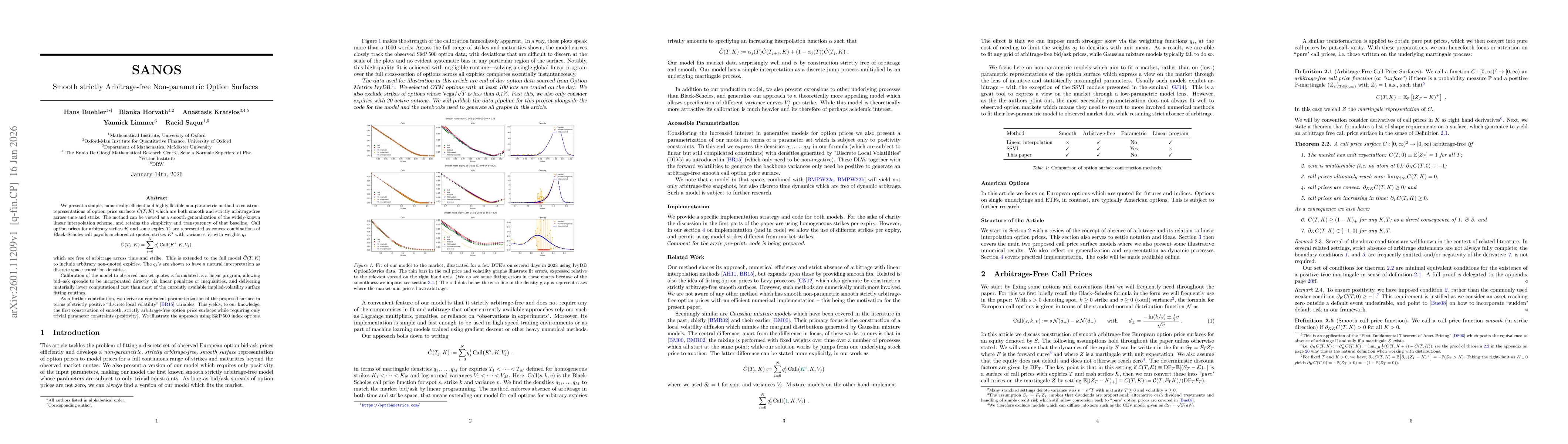

We present a simple, numerically efficient but highly flexible non-parametric method to construct representations of option price surfaces which are both smooth and strictly arbitrage-free across time...

We argue that the current practice of evaluating AI/ML time-series forecasting models, predominantly on benchmarks characterized by strong, persistent periodicities and seasonalities, obscures real pr...

Modern option-learning systems operate in two coordinates: price space, where markets quote and no-arbitrage constraints are most naturally enforced, and implied volatility (IV) space, where volatilit...