Bruno Gašperov

6 papers on arXiv

Academic Profile

Statistics

Similar Authors

Papers on arXiv

Finding Near-Optimal Portfolios With Quality-Diversity

The majority of standard approaches to financial portfolio optimization (PO) are based on the mean-variance (MV) framework. Given a risk aversion coefficient, the MV procedure yields a single portfo...

A New Angle: On Evolving Rotation Symmetric Boolean Functions

Rotation symmetric Boolean functions represent an interesting class of Boolean functions as they are relatively rare compared to general Boolean functions. At the same time, the functions in this cl...

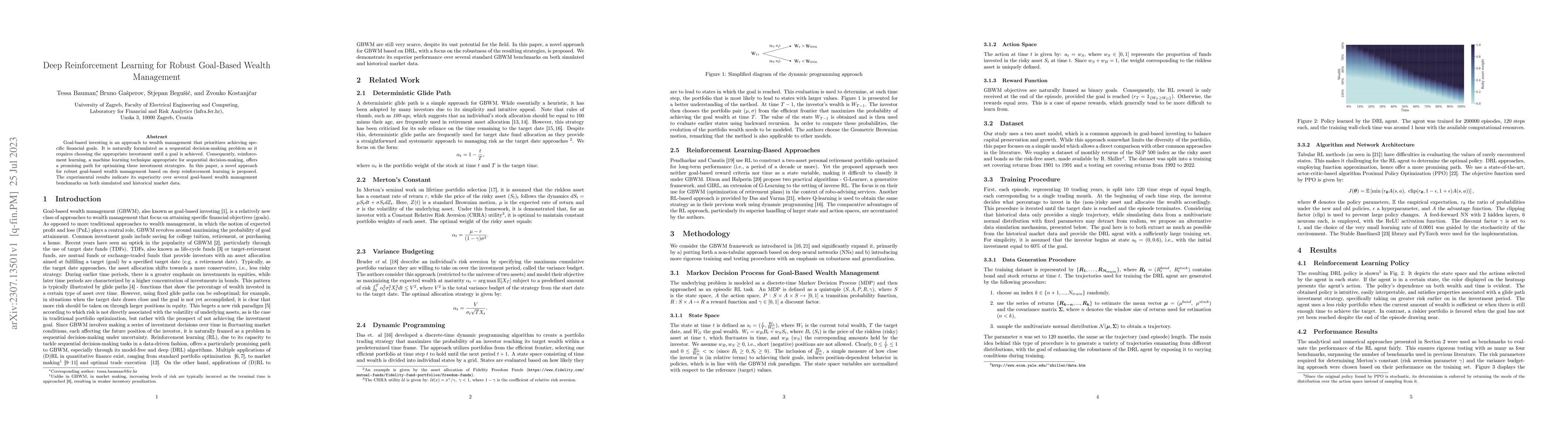

Deep Reinforcement Learning for Robust Goal-Based Wealth Management

Goal-based investing is an approach to wealth management that prioritizes achieving specific financial goals. It is naturally formulated as a sequential decision-making problem as it requires choosi...

On Evolvability and Behavior Landscapes in Neuroevolutionary Divergent Search

Evolvability refers to the ability of an individual genotype (solution) to produce offspring with mutually diverse phenotypes. Recent research has demonstrated that divergent search methods, particu...

A Search for Nonlinear Balanced Boolean Functions by Leveraging Phenotypic Properties

In this paper, we consider the problem of finding perfectly balanced Boolean functions with high non-linearity values. Such functions have extensive applications in domains such as cryptography and ...

Deep Reinforcement Learning for Market Making Under a Hawkes Process-Based Limit Order Book Model

The stochastic control problem of optimal market making is among the central problems in quantitative finance. In this paper, a deep reinforcement learning-based controller is trained on a weakly co...