Academic Profile

Statistics

Similar Authors

Papers on arXiv

We introduce a novel multivariate GARCH model with flexible convolution-t distributions that is applicable in high-dimensional systems. The model is called Cluster GARCH because it can accommodate c...

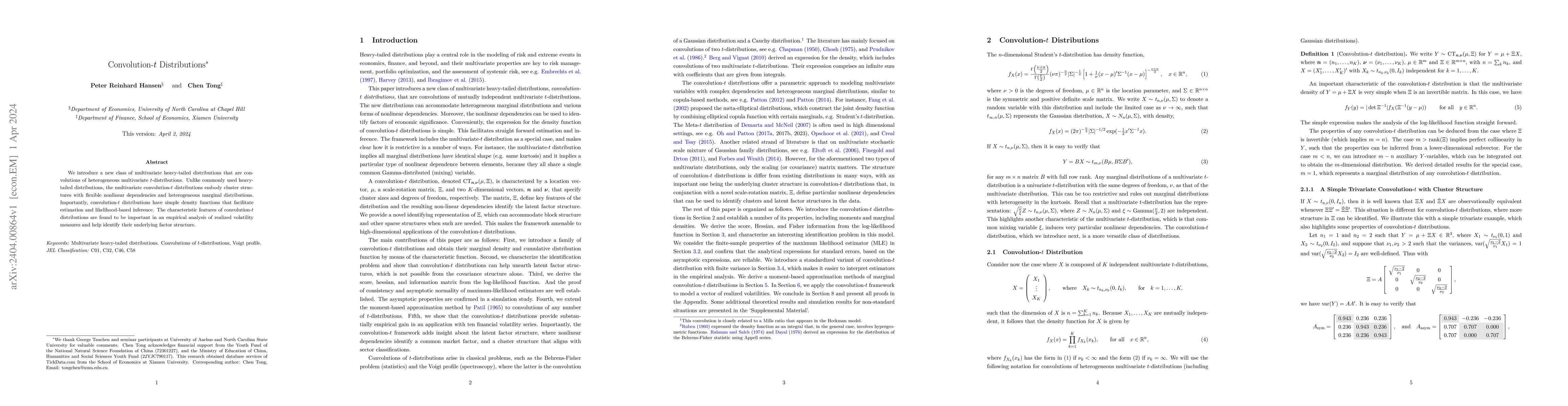

We introduce a new class of multivariate heavy-tailed distributions that are convolutions of heterogeneous multivariate t-distributions. Unlike commonly used heavy-tailed distributions, the multivar...

The Clustered Factor (CF) model induces a block structure on the correlation matrix and is commonly used to parameterize correlation matrices. Our results reveal that the CF model imposes superfluou...

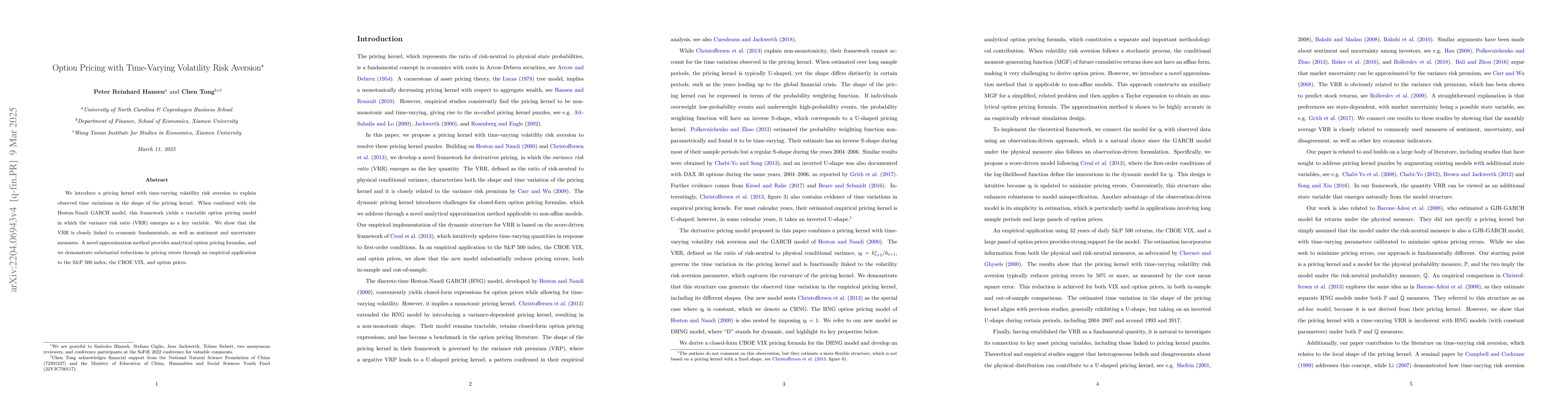

We introduce a novel pricing kernel with time-varying variance risk aversion that yields closed-form expressions for the VIX. We also obtain closed-form expressions for option prices with a novel ap...

We introduce a new volatility model for option pricing that combines Markov switching with the Realized GARCH framework. This leads to a novel pricing kernel with a state-dependent variance risk pre...

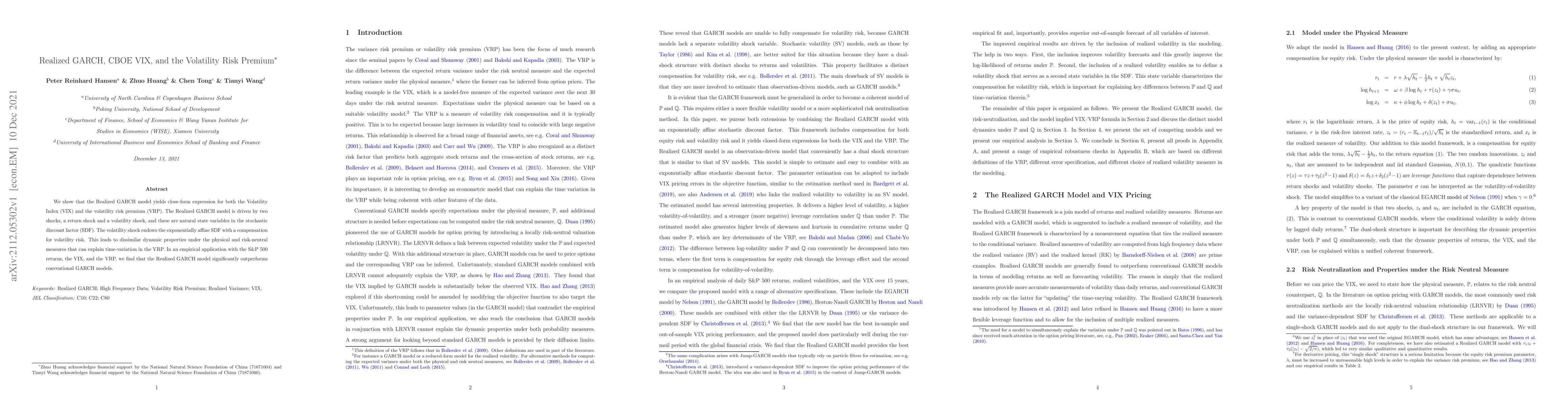

We show that the Realized GARCH model yields close-form expression for both the Volatility Index (VIX) and the volatility risk premium (VRP). The Realized GARCH model is driven by two shocks, a retu...

We introduce a novel method for obtaining a wide variety of moments of a random variable with a well-defined moment-generating function (MGF). We derive new expressions for fractional moments and frac...

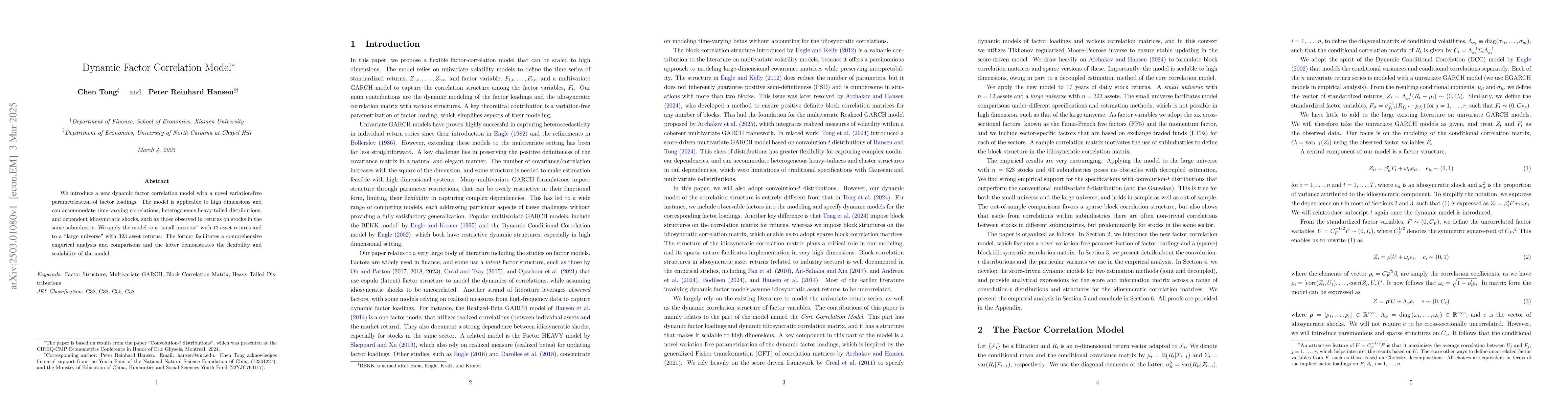

We introduce a new dynamic factor correlation model with a novel variation-free parametrization of factor loadings. The model is applicable to high dimensions and can accommodate time-varying correlat...

We derive an integral expression $G(z)$ for the reciprocal gamma function, $1/\Gamma(z)=G(z)/\pi$, that is valid for all $z\in\mathbb{C}$, without the need for analytic continuation. The same integral...

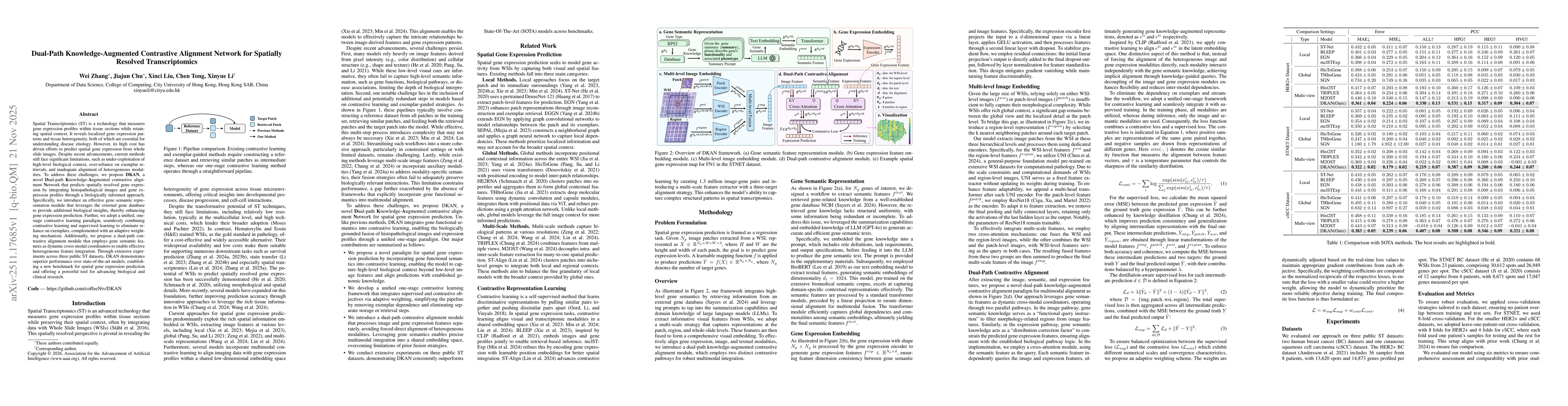

Spatial Transcriptomics (ST) is a technology that measures gene expression profiles within tissue sections while retaining spatial context. It reveals localized gene expression patterns and tissue het...

We take a new perspective on identification in structural dynamic models: rather than imposing restrictions, we optimize an objective. This provides new theoretical insights into traditional Cholesky ...

We present a unified integral framework based on the Fourier-Laplace transform evaluated along a vertical line in the complex plane. By identifying the moment-generating function (MGF) of a random var...

The convolution of a Gaussian and a Cauchy distribution, known as the Voigt distribution, is widely used in spectroscopy and provides a natural framework for modeling heavy-tailed measurement noise. W...

Score-driven models update time-varying parameters using conditional likelihood scores. This paper gives a Bayesian interpretation based on Tweedie's formula. In Gaussian signal extraction, Tweedie's ...