Academic Profile

Statistics

Similar Authors

Papers on arXiv

This paper studies an optimal dividend payout problem with drawdown constraint in a Brownian motion model, where the dividend payout rate must be no less than a fixed proportion of its historical ru...

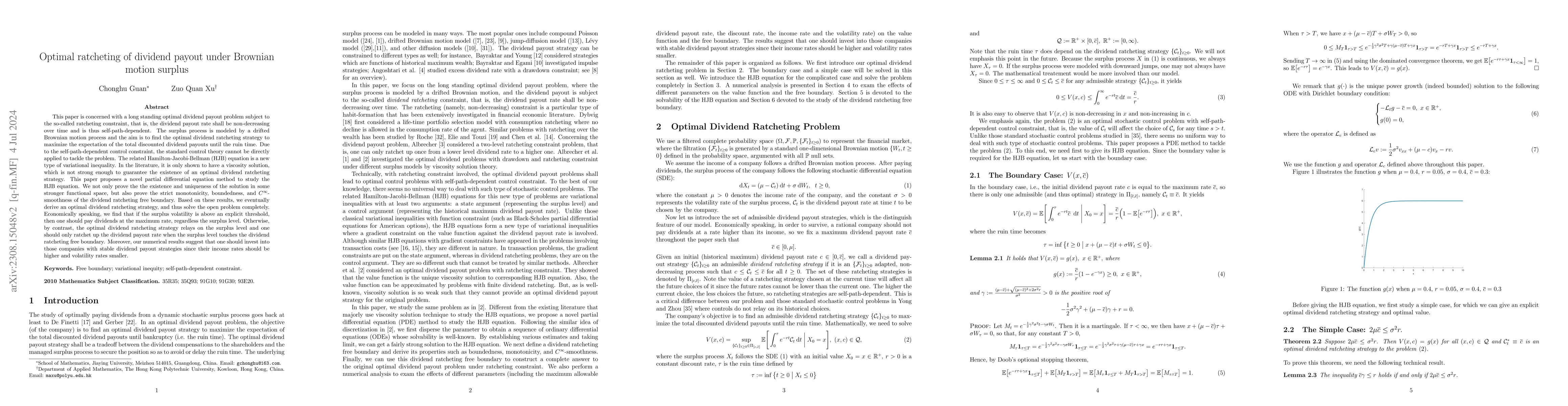

This paper is concerned with a long standing optimal dividend payout problem in insurance subject to the so-called ratcheting constraint, that is, the dividend payout rate shall be non-decreasing ov...

We study Markowitz's mean-variance portfolio selection problem in a continuous-time Black-Scholes market with different borrowing and saving rates. The associated Hamilton-Jacobi-Bellman equation is...

This paper studies a life-time consumption-investment problem under the Black-Scholes framework, where the consumption rate is subject to a lower bound constraint that linearly depends on her wealth...

In this paper, we study a free boundary problem, which arises from an optimal trading problem of a stock that is driven by a uncertain market status process. The free boundary problem is a variation...

This paper studies a dynamic optimal reinsurance and dividend-payout problem for an insurance company in a finite time horizon. The goal of the company is to maximize the expected cumulative discoun...

We study an optimal investment and consumption problem over a finite-time horizon, in which an individual invests in a risk-free asset and a risky asset, and evaluate utility using a general utility f...

We consider an optimal dividend payout problem for an insurance company whose surplus follows the classical Cramér-Lundberg model. The dividend rate is subject to a ratcheting constraint (i.e., it mus...