Academic Profile

Statistics

Similar Authors

Papers on arXiv

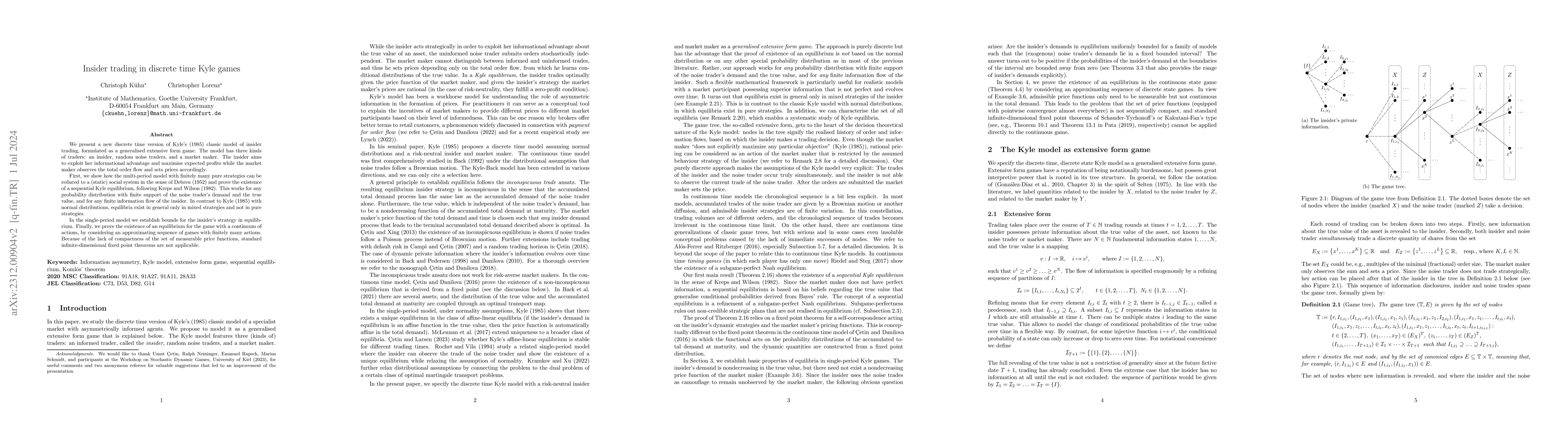

We present a new discrete time version of Kyle's (1985) classic model of insider trading, formulated as a generalised extensive form game. The model has three kinds of traders: an insider, random no...

We prove a version of the fundamental theorem of asset pricing (FTAP) in continuous time that is based on the strict no-arbitrage condition and that is applicable to both frictionless markets and ma...

picFoam is a fully kinetic electrostatic Particle-in-Cell(PIC) solver, including Monte Carlo Collisions(MCC), for non-equilibrium plasma research in the open-source framework of OpenFOAM. The solver...

A standing assumption in the literature on proportional transaction costs is efficient friction. Together with robust no free lunch with vanishing risk, it rules out strategies of infinite variation...

We generalize classical results on the existence of optimal portfolios in discrete time frictionless market models to models with capital gains taxes. We consider the realistic but mathematically chal...