Academic Profile

Statistics

Similar Authors

Papers on arXiv

Milionis et al.(2023) studied the rate at which automated market makers leak value to arbitrageurs when block times are discrete and follow a Poisson process, and where the risky asset price follows...

This work introduces a framework for evaluating onchain order flow auctions (OFAs), emphasizing the metric of price improvement. Utilizing a set of open-source tools, our methodology systematically ...

Automated market makers (AMMs) have emerged as the dominant market mechanism for trading on decentralized exchanges implemented on blockchains. This paper presents a single mechanism that targets tw...

We develop a general and practical framework to address the problem of the optimal design of dynamic fee mechanisms for multiple blockchain resources. Our framework allows to compute policies that o...

We consider the impact of trading fees on the profits of arbitrageurs trading against an automated marker marker (AMM) or, equivalently, on the adverse selection incurred by liquidity providers due ...

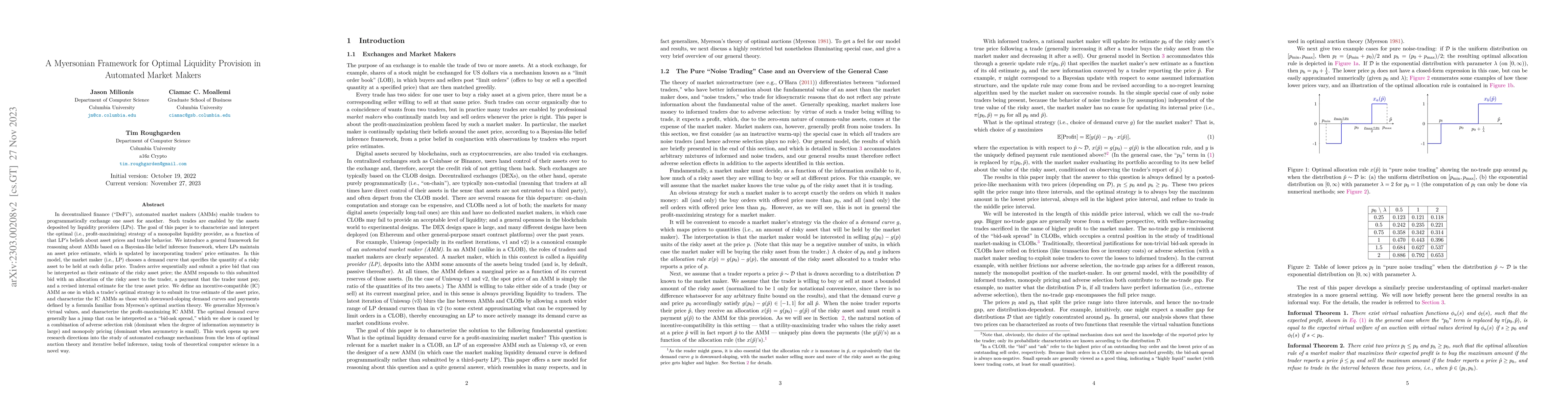

In decentralized finance ("DeFi"), automated market makers (AMMs) enable traders to programmatically exchange one asset for another. Such trades are enabled by the assets deposited by liquidity prov...

This paper presents a general framework for the design and analysis of exchange mechanisms between two assets that unifies and enables comparisons between the two dominant paradigms for exchange, co...

We consider the market microstructure of automated market makers (AMMs) from the perspective of liquidity providers (LPs). Our central contribution is a ``Black-Scholes formula for AMMs''. We identi...

We consider a liquidation problem in which a risk-averse trader tries to liquidate a fixed quantity of an asset in the presence of market impact and random price fluctuations. The trader encounters ...

We study the use of policy gradient algorithms to optimize over a class of generalized Thompson sampling policies. Our central insight is to view the posterior parameter sampled by Thompson sampling...

We consider a finite-horizon multi-armed bandit (MAB) problem in a Bayesian setting, for which we propose an information relaxation sampling framework. With this framework, we define an intuitive fa...

Revert protection is a feature provided by some blockchain platforms that prevents users from incurring fees for failed transactions. This paper explores the economic implications and benefits of reve...

We empirically study liquidity and market depth on decentralized exchanges (DEXs), identifying factors at the blockchain, token pair, and pool levels that predict future effective spreads for fixed tr...

In financial applications, latency advantages - the ability to make decisions later than others, even without the ability to see what others have done - can provide individual participants with an edg...

This paper presents a comprehensive framework for transaction posting and pricing in Layer 2 (L2) blockchain systems, focusing on challenges stemming from fluctuating Layer 1 (L1) gas fees and the con...

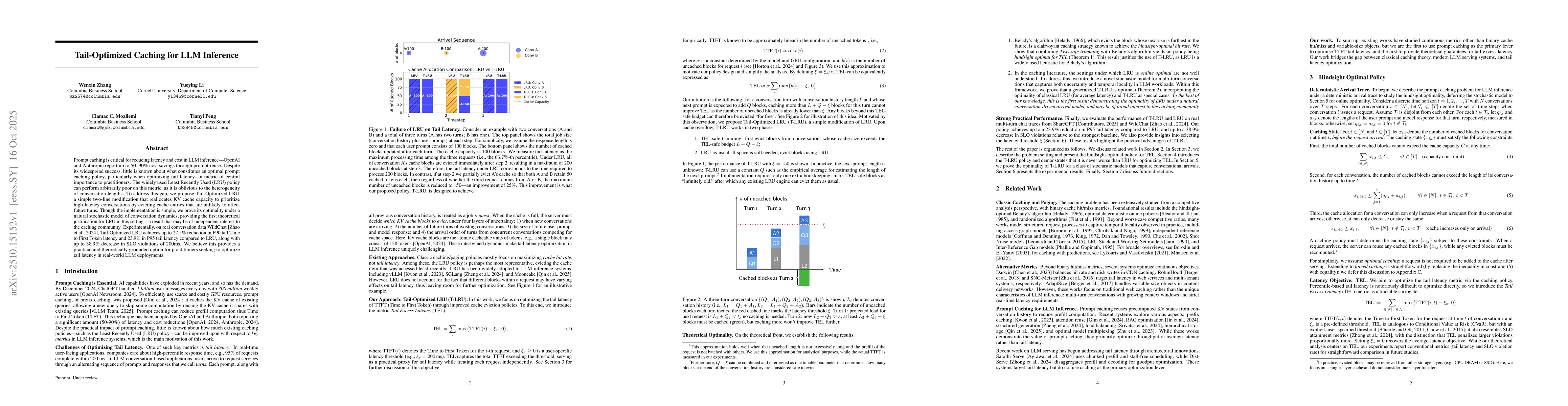

Prompt caching is critical for reducing latency and cost in LLM inference: OpenAI and Anthropic report up to 50-90% cost savings through prompt reuse. Despite its widespread success, little is known a...

AI researchers have long focused on poker-like games as a testbed for environments characterized by multi-player dynamics, imperfect information, and reasoning under uncertainty. While recent breakthr...

Auto-deleveraging (ADL) mechanisms are a critical yet understudied component of risk management on cryptocurrency futures exchanges. When available margin and other loss-absorbing resources are insuff...

Forward-looking volatility forecasts are central inputs to derivatives pricing, market making, risk management, and volatility-linked trading strategies, with ARCH and GARCH models serving as the cano...