Academic Profile

Statistics

Similar Authors

Papers on arXiv

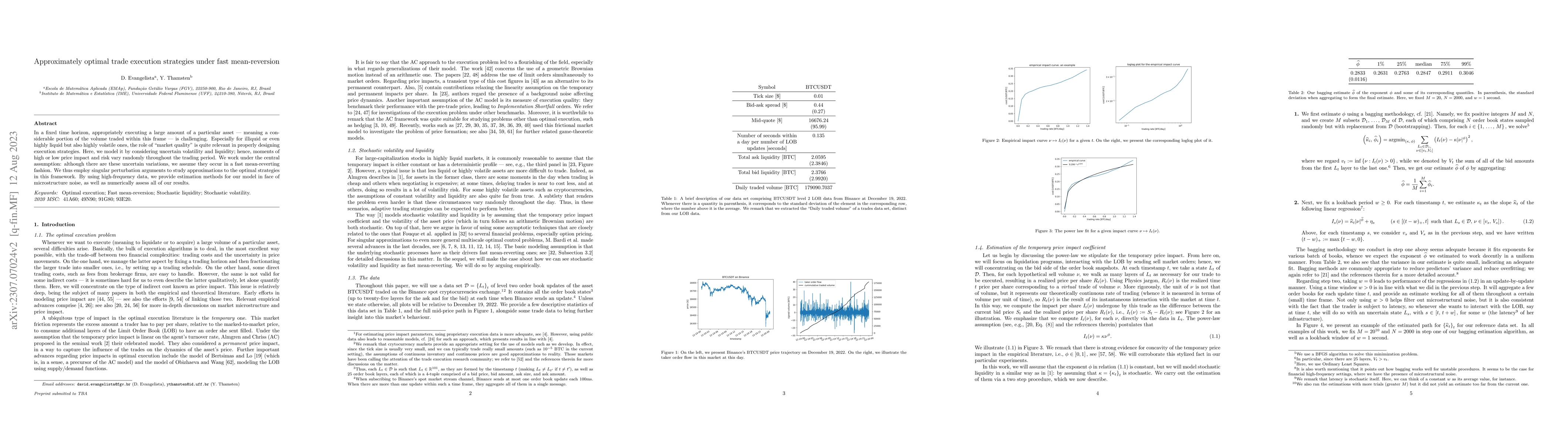

In a fixed time horizon, appropriately executing a large amount of a particular asset -- meaning a considerable portion of the volume traded within this frame -- is challenging. Especially for illiq...

We propose two novel frameworks to study the price formation of an asset negotiated in an order book. Specifically, we develop a game-theoretic model in many-person games and mean-field games, consi...

We investigate stochastic differential games of optimal trading comprising a finite population. There are market frictions in the present framework, which take the form of stochastic permanent and t...

A large proportion of market making models derive from the seminal model of Avellaneda and Stoikov. The numerical approximation of the value function and the optimal quotes in these models remains a...

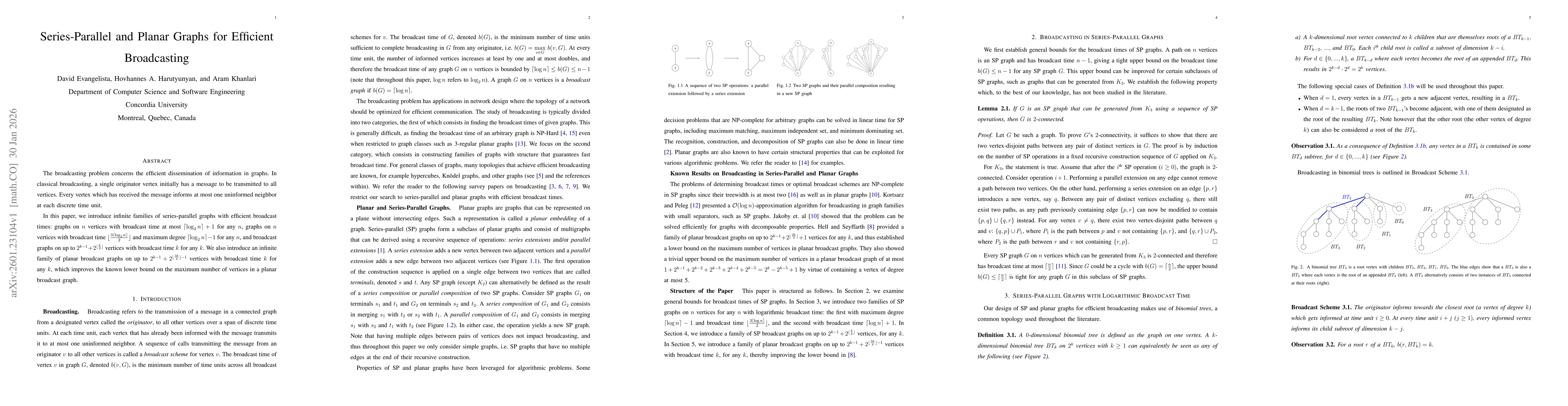

The broadcasting problem concerns the efficient dissemination of information in graphs. In classical broadcasting, a single originator vertex initially has a message to be transmitted to all vertices....