Academic Profile

Statistics

Similar Authors

Papers on arXiv

This work extends a previous work in regime detection, which allowed trading positions to be profitably adjusted when a new regime was detected, to ex ante prediction of regimes, leading to substant...

Regime-switching poses both problems and opportunities for portfolio managers. If a switch in the behaviour of the markets is not quickly detected it can be a source of loss, since previous trading ...

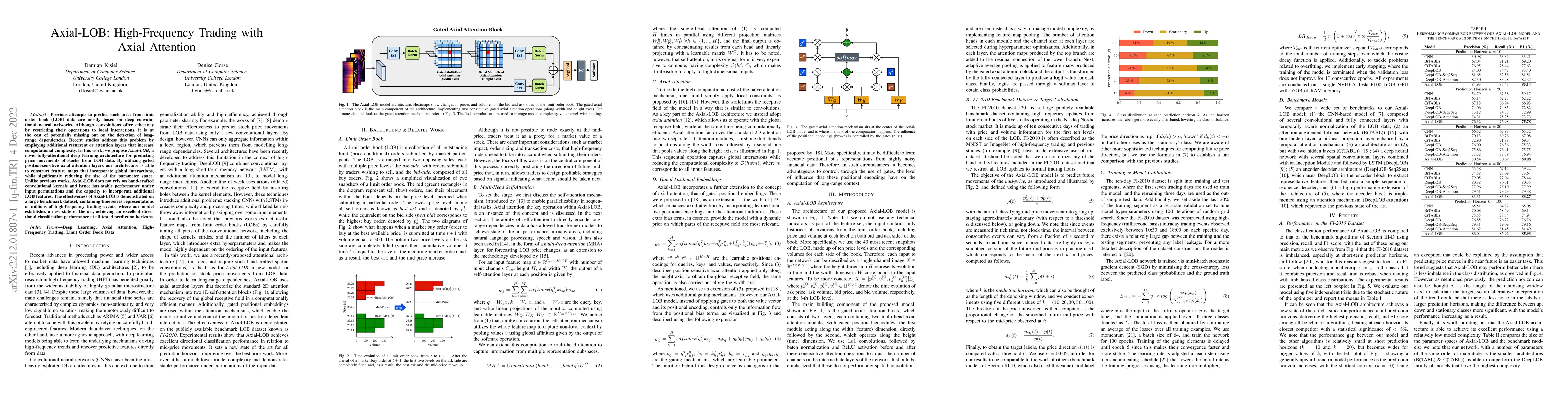

Previous attempts to predict stock price from limit order book (LOB) data are mostly based on deep convolutional neural networks. Although convolutions offer efficiency by restricting their operatio...

This paper extends boolean particle swarm optimization to a multi-objective setting, to our knowledge for the first time in the literature. Our proposed new boolean algorithm, MBOnvPSO, is notably s...

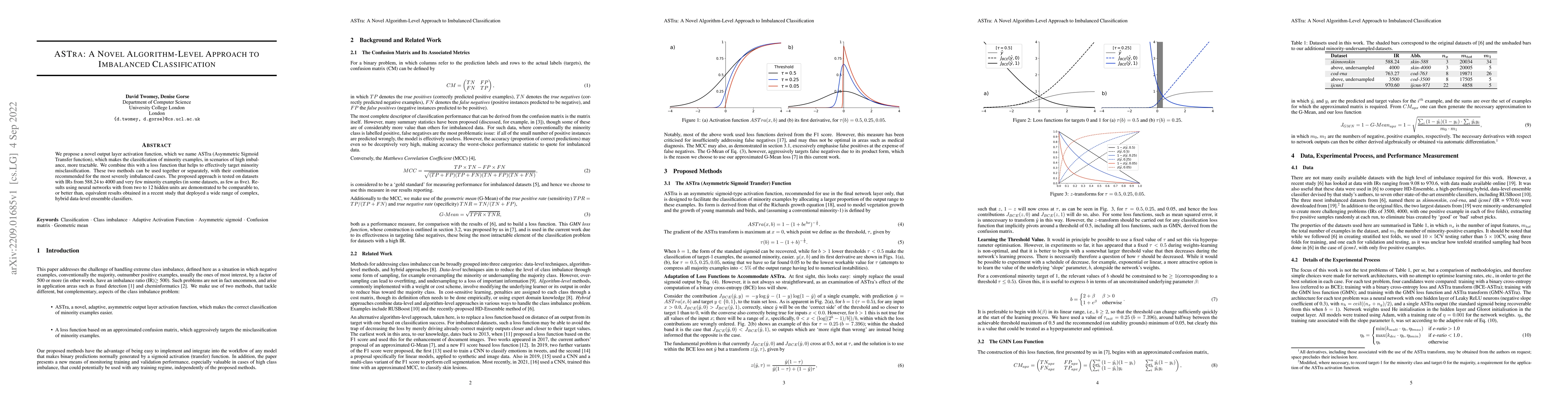

We propose a novel output layer activation function, which we name ASTra (Asymmetric Sigmoid Transfer function), which makes the classification of minority examples, in scenarios of high imbalance, ...

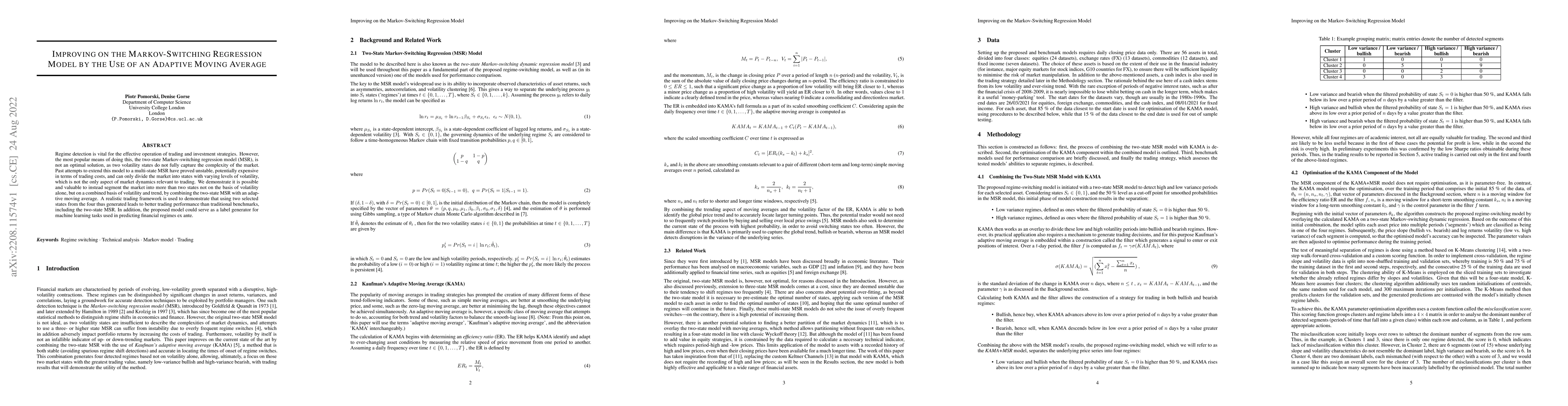

Regime detection is vital for the effective operation of trading and investment strategies. However, the most popular means of doing this, the two-state Markov-switching regression model (MSR), is n...

Traditional approaches to financial asset allocation start with returns forecasting followed by an optimization stage that decides the optimal asset weights. Any errors made during the forecasting s...

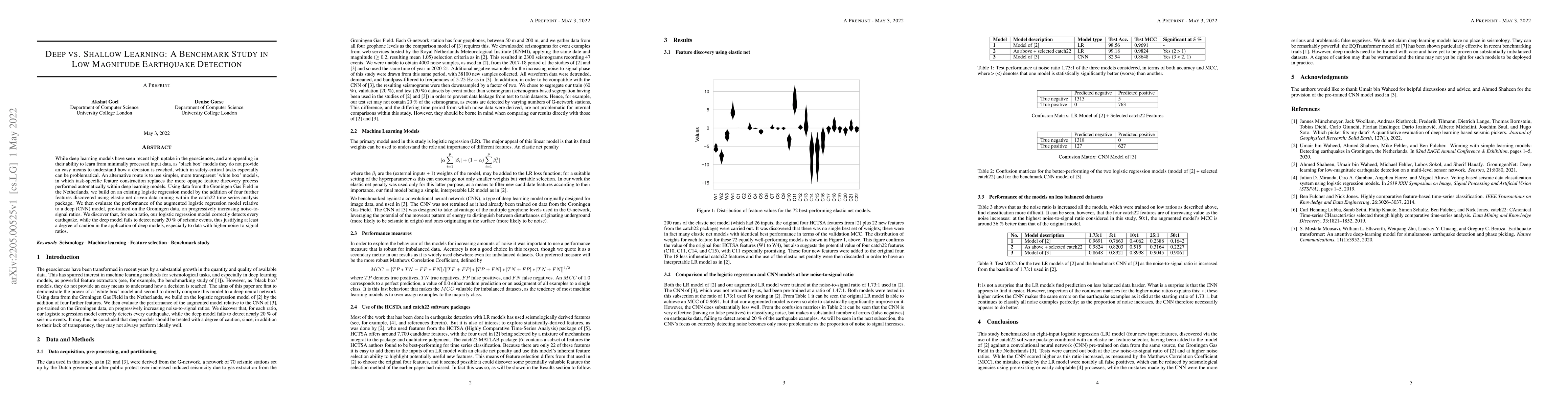

While deep learning models have seen recent high uptake in the geosciences, and are appealing in their ability to learn from minimally processed input data, as black box models they do not provide a...

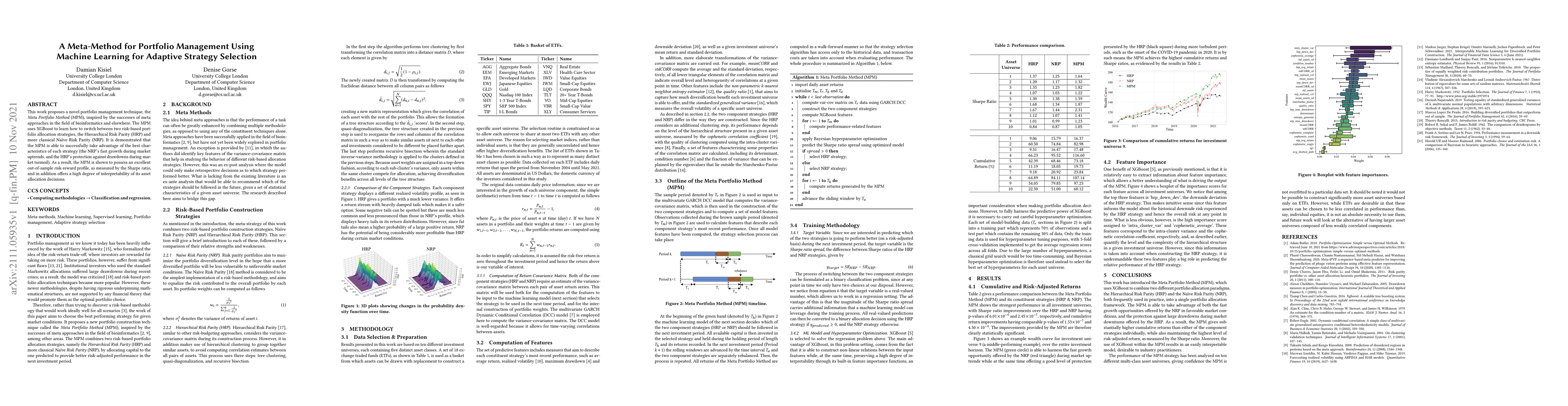

This work proposes a novel portfolio management technique, the Meta Portfolio Method (MPM), inspired by the successes of meta approaches in the field of bioinformatics and elsewhere. The MPM uses XG...

Intra-day price variations in financial markets are driven by the sequence of orders, called the order flow, that is submitted at high frequency by traders. This paper introduces a novel application...

In this paper we propose a deep recurrent model based on the order flow for the stationary modelling of the high-frequency directional prices movements. The order flow is the microsecond stream of o...

In this paper we propose a deep recurrent architecture for the probabilistic modelling of high-frequency market prices, important for the risk management of automated trading systems. Our proposed a...

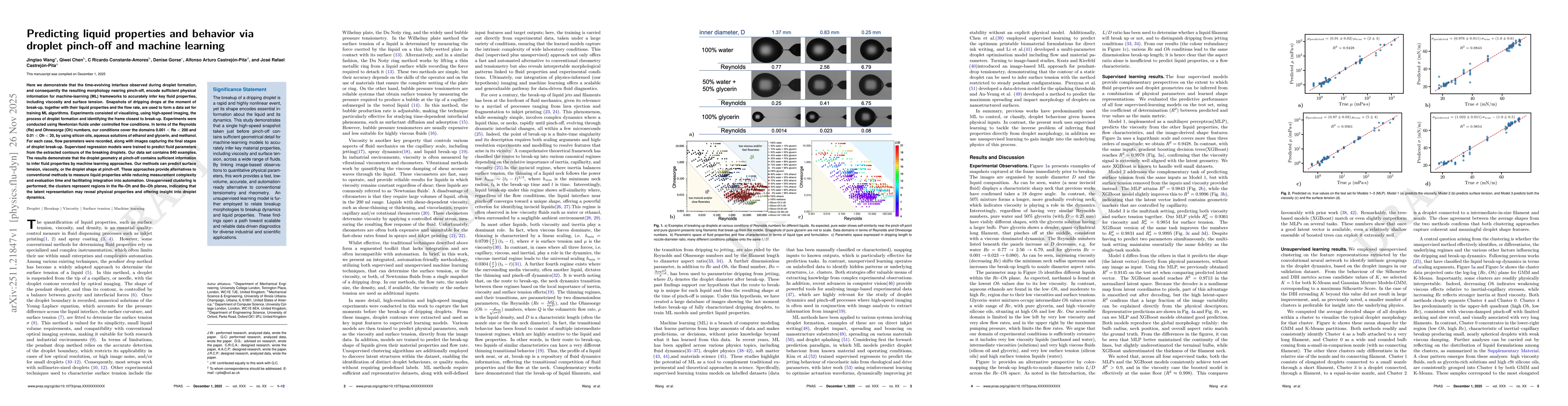

Here we demonstrate that the time-evolving interface observed during droplet formation, and consequently the resulting morphology nearing pinch-off, encode sufficient physical information for machine-...

In this paper we build upon a previous study in which we demonstrated, using XGBoost and earthquake catalogue data from Japan and Chile, that a set of 60 seismic statistical features (SSFs) had much g...