Academic Profile

Statistics

Similar Authors

Papers on arXiv

In this paper we show that Cardanos formula for the solution of cubic equations can be reduced to expressions involving only square roots if the real root is rational.

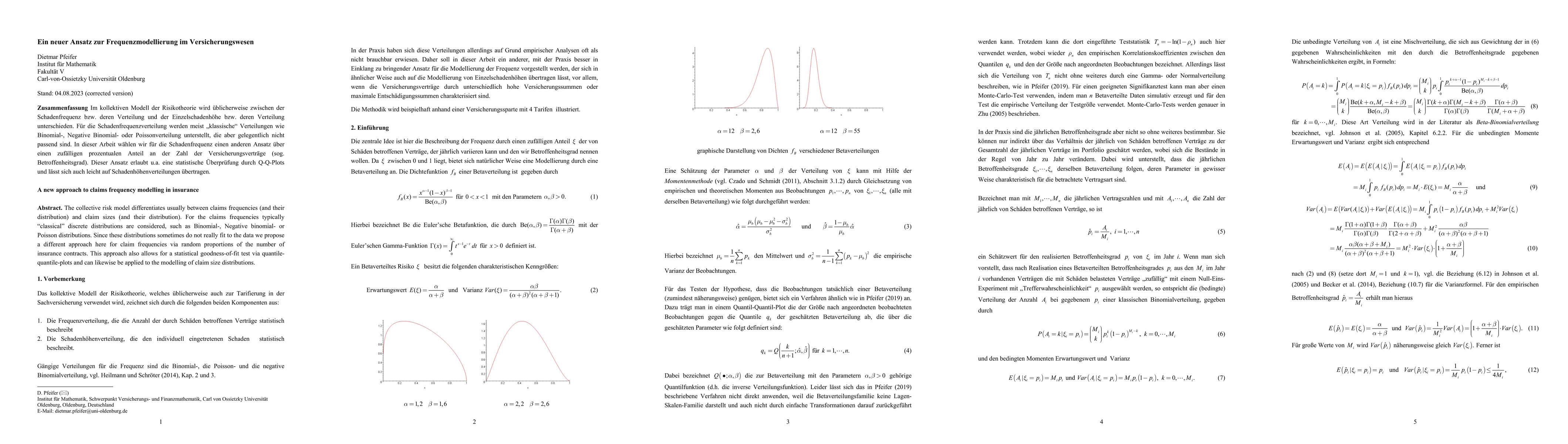

The collective risk model differentiates usually between claims frequencies (and their distribution) and claim sizes (and their distribution). For the claims frequencies typically classical discrete...

In this study, we will discuss recent developments in risk management of the global financial and insurance business with respect to sustainable development. So far climate change aspects have been ...

The central idea of the paper is to present a general simple patchwork construction principle for multivariate copulas that create unfavourable VaR (i.e. Value at Risk) scenarios while maintaining g...

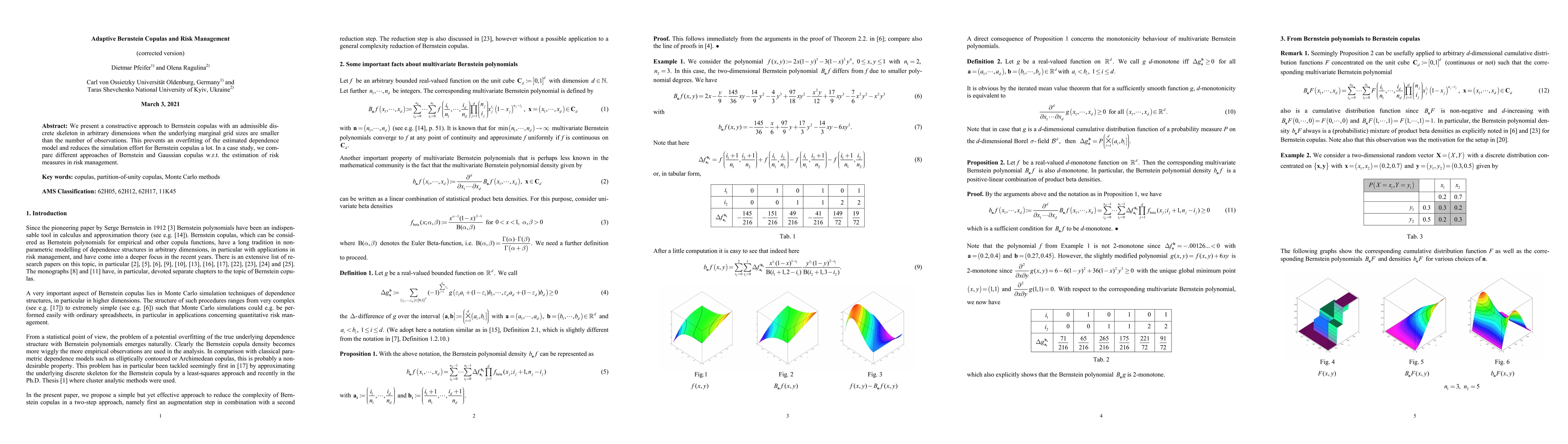

We present a constructive approach to Bernstein copulas with an admissible discrete skeleton in arbitrary dimensions when the underlying marginal grid sizes are smaller than the number of observatio...

In this paper we review Bernstein and grid-type copulas for arbitrary dimensions and general grid resolutions in connection with discrete random vectors possessing uniform margins. We further sugges...

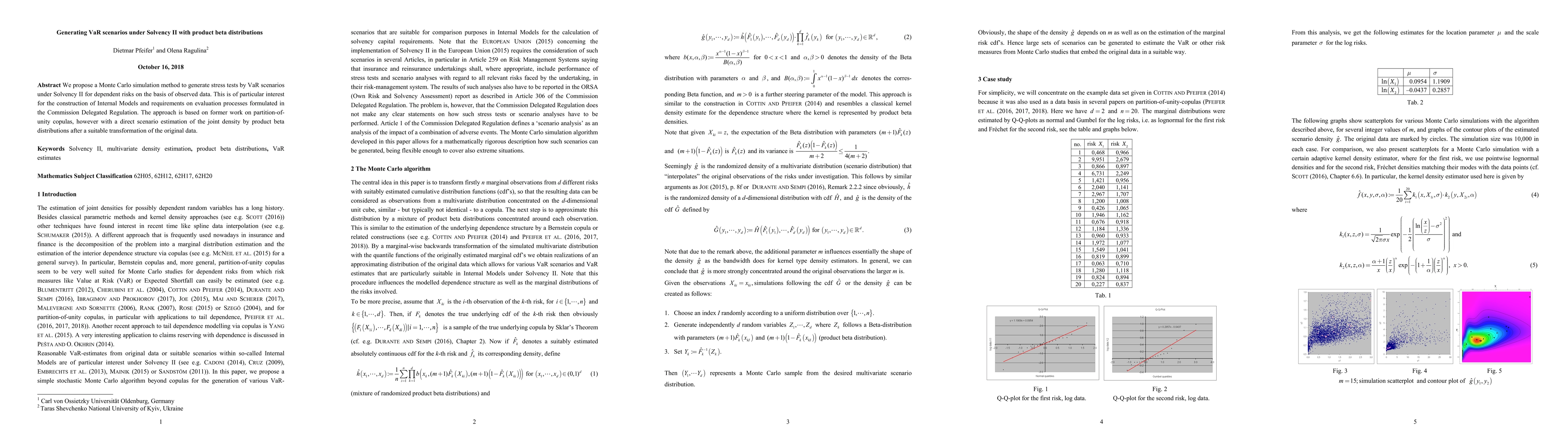

We propose a Monte Carlo simulation method to generate stress tests by VaR scenarios under Solvency II for dependent risks on the basis of observed data. This is of particular interest for the const...

We present a simple elementary recursive representation of the so called Faulhaber series $\sum_{k=1}^n k^n$ for integer $n$ and $N$, without reference to Bernoulli numbers or polynomials.