Academic Profile

Statistics

Similar Authors

Papers on arXiv

Central Banks interventions are frequent in response to exogenous events with direct implications on financial market volatility. In this paper, we introduce the Asymmetric Jump Multiplicative Error...

Markov Switching models have had increasing success in time series analysis due to their ability to capture the existence of unobserved discrete states in the dynamics of the variables under study. ...

The financial turmoil surrounding the Great Recession called for unprecedented intervention by Central Banks: unconventional policies affected various areas in the economy, including stock market vo...

Recent developments in financial time series focus on modeling volatility across multiple assets or indices in a multivariate framework, accounting for potential interactions such as spillover effects...

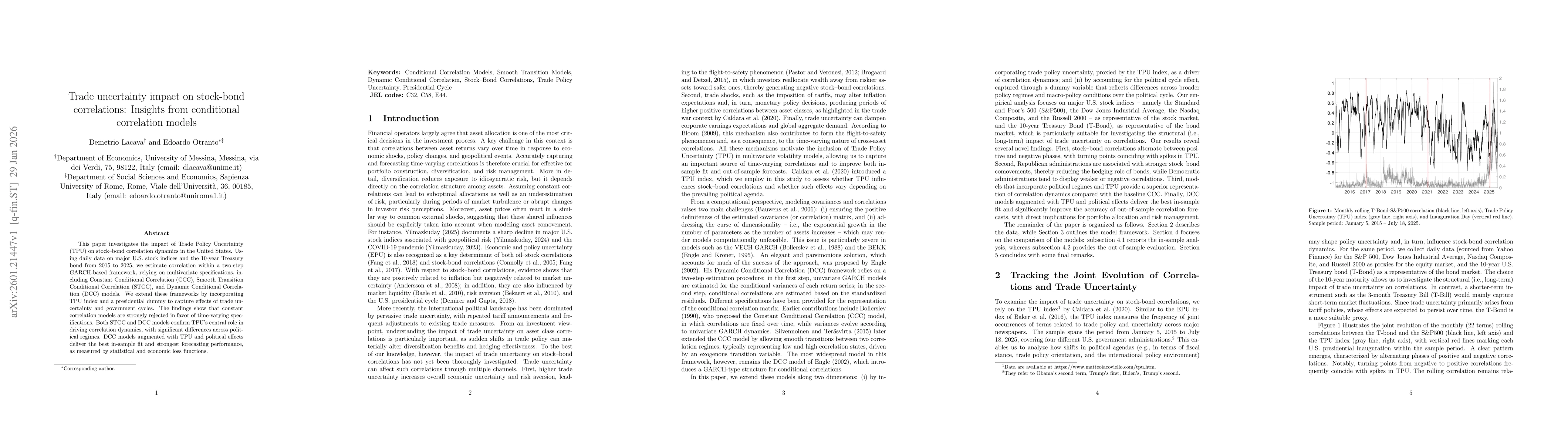

This paper investigates the impact of Trade Policy Uncertainty (TPU) on stock-bond correlation dynamics in the United States. Using daily data on major U.S. stock indices and the 10-year Treasury bond...

This paper proposes a novel data-driven approach for identifying and modelling areas with similar temperature variations throufigureh clustering and Space-Time AutoRegressive (STAR) models. Using annu...

We propose a modeling framework for time-varying covariance matrices based on the assumption that the logarithm of a realized covariance matrix follows a matrix-variate oNrmal distribution. By operati...

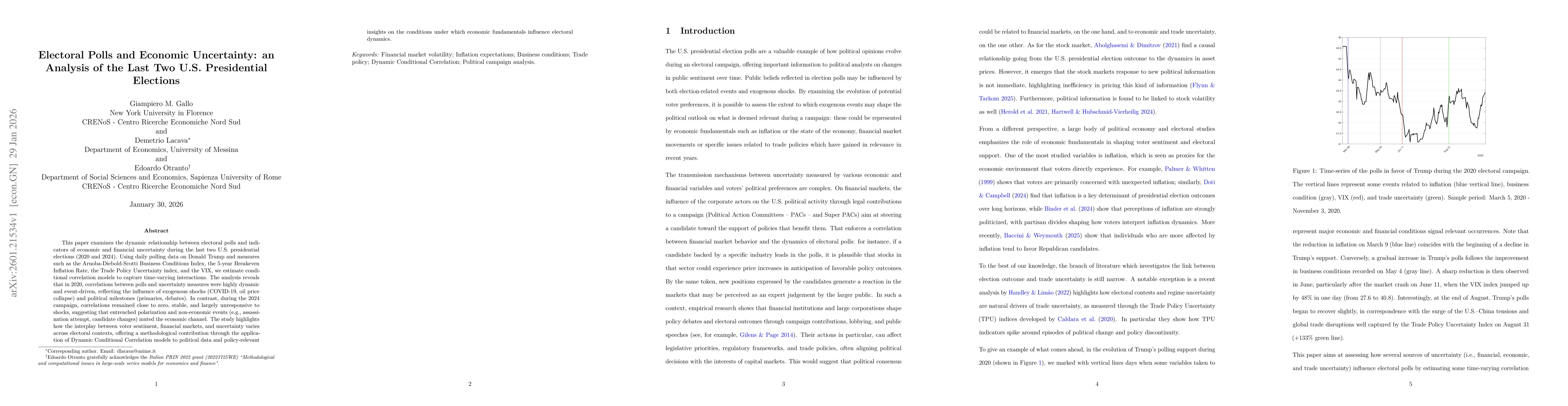

This paper examines the dynamic relationship between electoral polls and indicators of economic and financial uncertainty during the last two U.S. presidential elections (2020 and 2024). Using daily p...

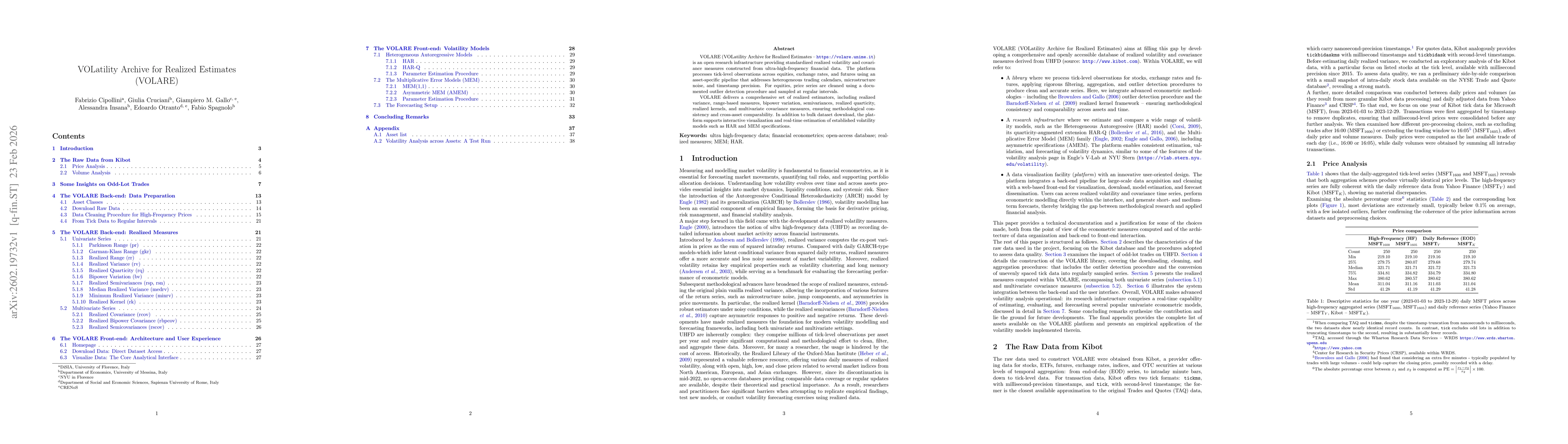

VOLARE (VOLatility Archive for Realized Estimates - https://volare.unime.it) is an open research infrastructure providing standardized realized volatility and covariance measures constructed from ultr...