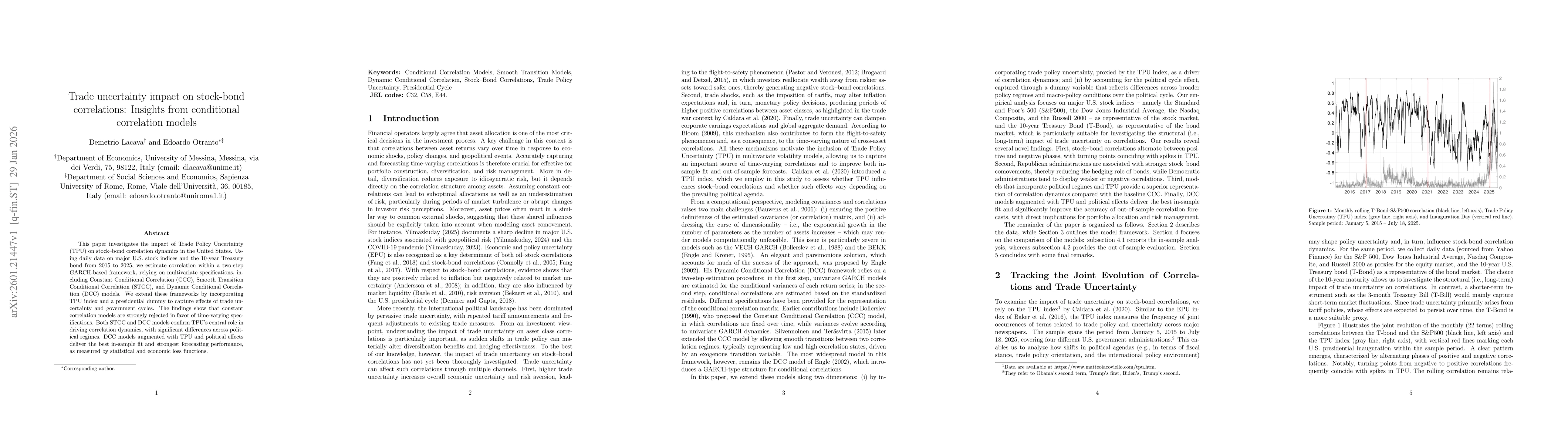

This paper investigates the impact of Trade Policy Uncertainty (TPU) on stock-bond correlation dynamics in the United States. Using daily data on major U.S. stock indices and the 10-year Treasury bond from 2015 to 2025, we estimate correlation within a two-step GARCH-based framework, relying on multivariate specifications, including Constant Conditional Correlation (CCC), Smooth Transition Conditional Correlation (STCC), and Dynamic Conditional Correlation (DCC) models. We extend these frameworks by incorporating TPU index and a presidential dummy to capture effects of trade uncertainty and government cycles. The findings show that constant correlation models are strongly rejected in favor of time-varying specifications. Both STCC and DCC models confirm TPU's central role in driving correlation dynamics, with significant differences across political regimes. DCC models augmented with TPU and political effects deliver the best in-sample fit and strongest forecasting performance, as measured by statistical and economic loss functions.

Discussion 0