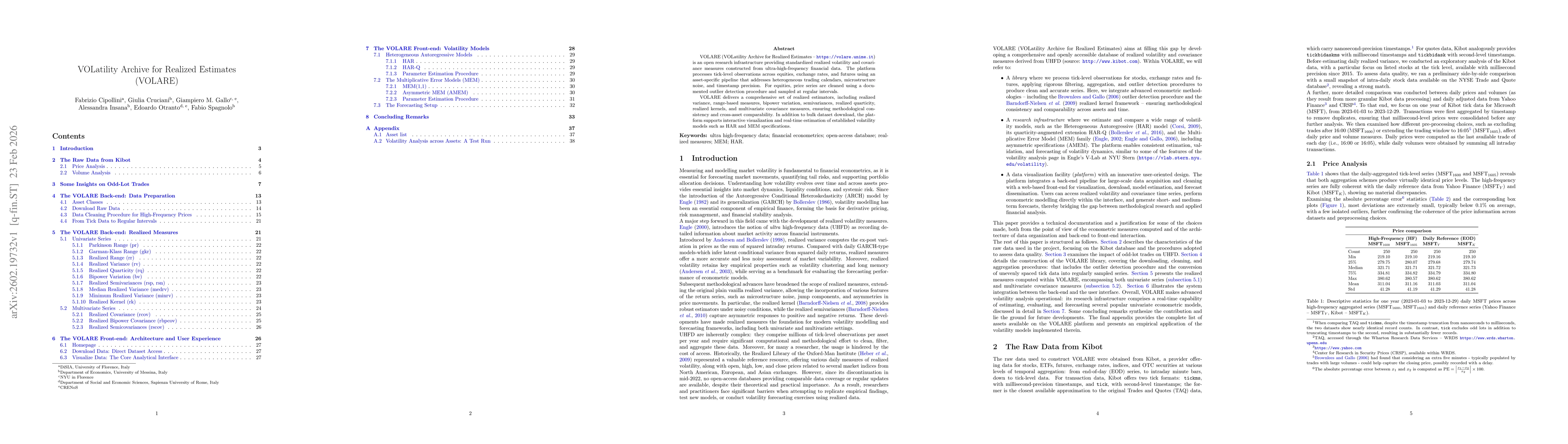

VOLARE (VOLatility Archive for Realized Estimates - https://volare.unime.it) is an open research infrastructure providing standardized realized volatility and covariance measures constructed from ultra-high-frequency financial data. The platform processes tick-level observations across equities, exchange rates, and futures using an asset-specific pipeline that addresses heterogeneous trading calendars, microstructure noise, and timestamp precision. For equities, price series are cleaned using a documented outlier detection procedure and sampled at regular intervals.

VOLARE delivers a comprehensive set of realized estimators, including realized variance, range-based measures, bipower variation, semivariances, realized quarticity, realized kernels, and multivariate covariance measures, ensuring methodological consistency and cross-asset comparability. In addition to bulk dataset download, the platform supports interactive visualization and real-time estimation of established volatility models such as HAR and MEM specifications.

Discussion 0