Academic Profile

Statistics

Similar Authors

Papers on arXiv

The main component of the NextGeneration EU (NGEU) program is the Recovery and Resilience Facility (RRF), spanning an implementation period between 2021 and 2026. The RRF also includes a monitoring ...

We focus on the time-varying modeling of VaR at a given coverage $\tau$, assessing whether the quantiles of the distribution of the returns standardized by their conditional means and standard devia...

Central Banks interventions are frequent in response to exogenous events with direct implications on financial market volatility. In this paper, we introduce the Asymmetric Jump Multiplicative Error...

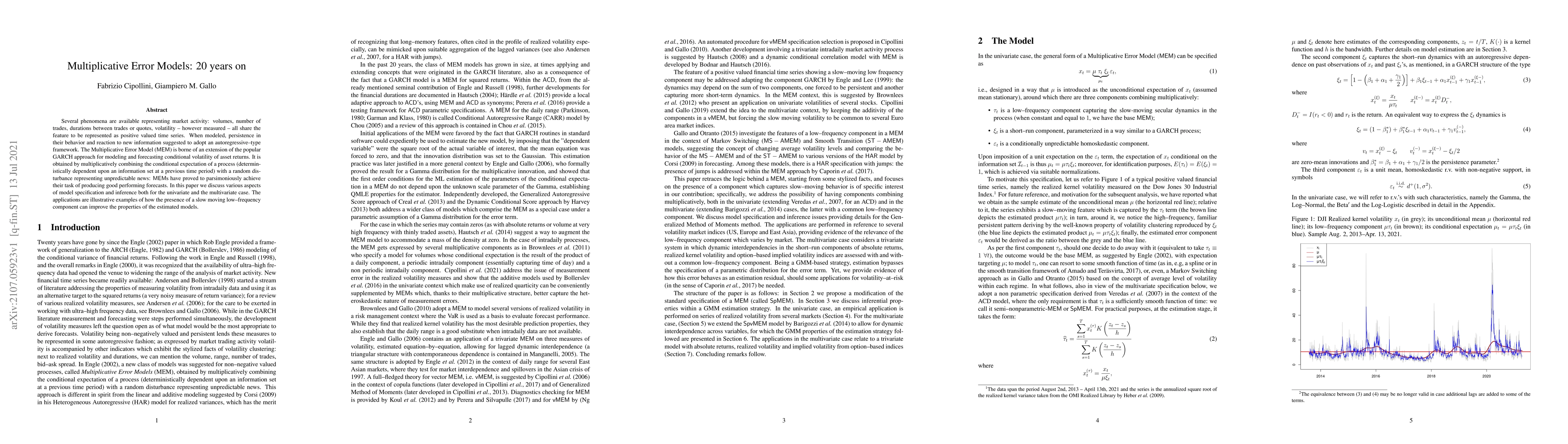

Several phenomena are available representing market activity: volumes, number of trades, durations between trades or quotes, volatility - however measured - all share the feature to be represented a...

The financial turmoil surrounding the Great Recession called for unprecedented intervention by Central Banks: unconventional policies affected various areas in the economy, including stock market vo...

Although quantile regression to calculate risk measures has been widely established in the financial literature, when considering data observed at mixed--frequency, an extension is needed. In this p...

We suggest the Doubly Multiplicative Error class of models (DMEM) for modeling and forecasting realized volatility, which combines two components accommodating low-, respectively, high-frequency fea...

We build the time series of optimal realized portfolio weights from high-frequency data and we suggest a novel Dynamic Conditional Weights (DCW) model for their dynamics. DCW is benchmarked against ...

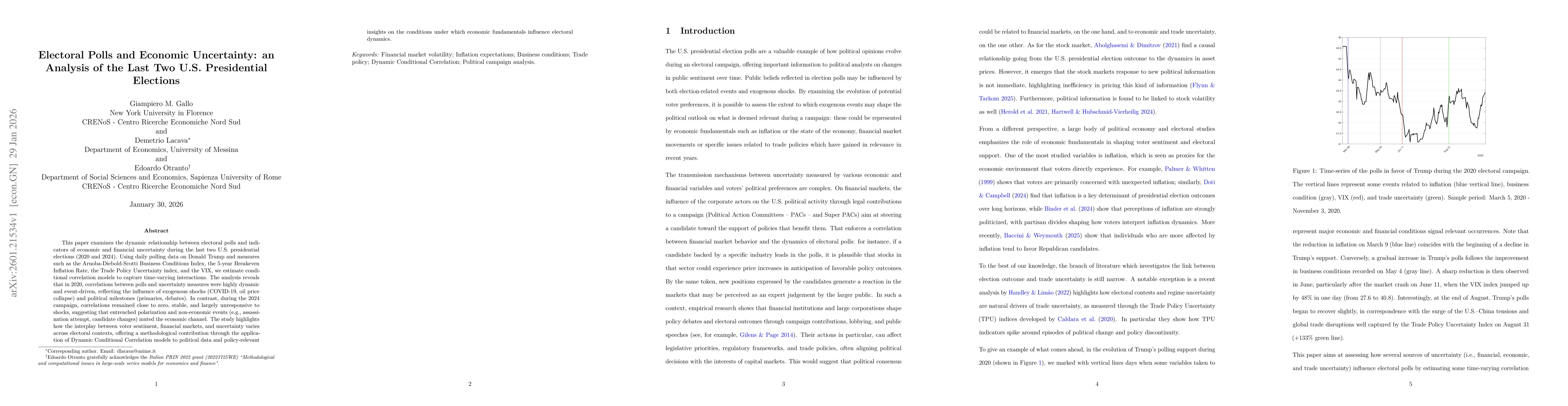

This paper examines the dynamic relationship between electoral polls and indicators of economic and financial uncertainty during the last two U.S. presidential elections (2020 and 2024). Using daily p...

VOLARE (VOLatility Archive for Realized Estimates - https://volare.unime.it) is an open research infrastructure providing standardized realized volatility and covariance measures constructed from ultr...