Academic Profile

Statistics

Similar Authors

Papers on arXiv

This work introduces a novel approach to price rainbow options, a type of path-independent multi-asset derivatives, with quantum computers. Leveraging the Iterative Quantum Amplitude Estimation meth...

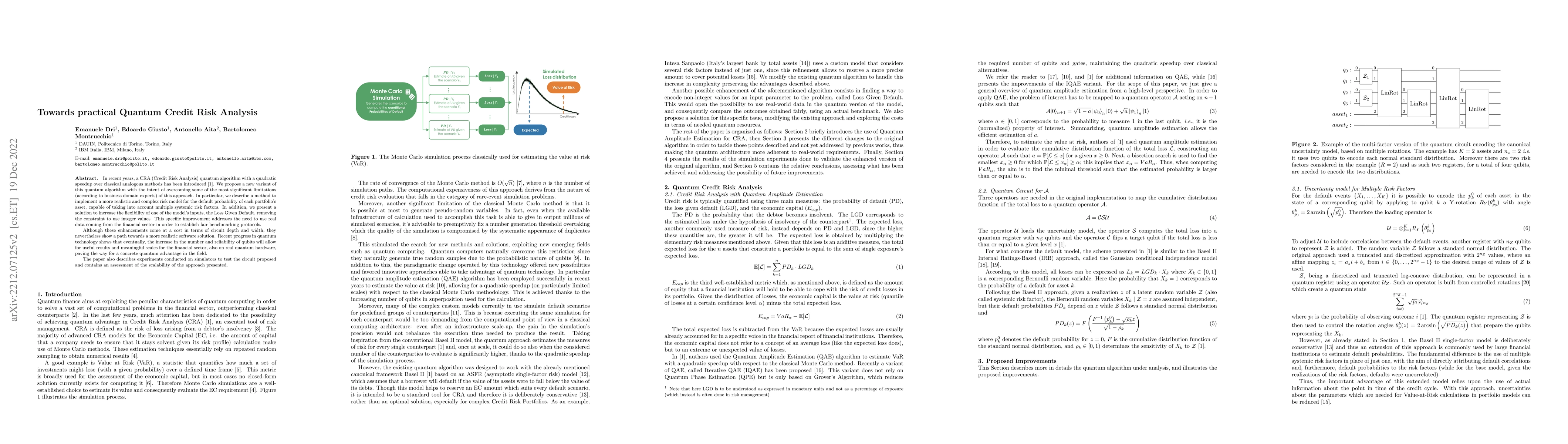

In recent years, a CRA (Credit Risk Analysis) quantum algorithm with a quadratic speedup over classical analogous methods has been introduced. We propose a new variant of this quantum algorithm with...

Quantum computing is a new technology that is expected to revolutionize the computation paradigm in the next few years. Qubits exploit the quantum physics proprieties to increase the parallelism and...

In this paper, we present an approach for estimating significant financial metrics within risk management by utilizing quantum phenomena for random number generation. We explore Quantum-Enhanced Monte...

The analysis of credit risk is crucial for the efficient operation of financial institutions. Quantum Amplitude Estimation (QAE) offers the potential for a quadratic speed-up over classical methods us...

We present a comprehensive quantum algorithm tailored for pricing autocallable options, offering a full implementation and experimental validation. Our experiments include simulations conducted on hig...

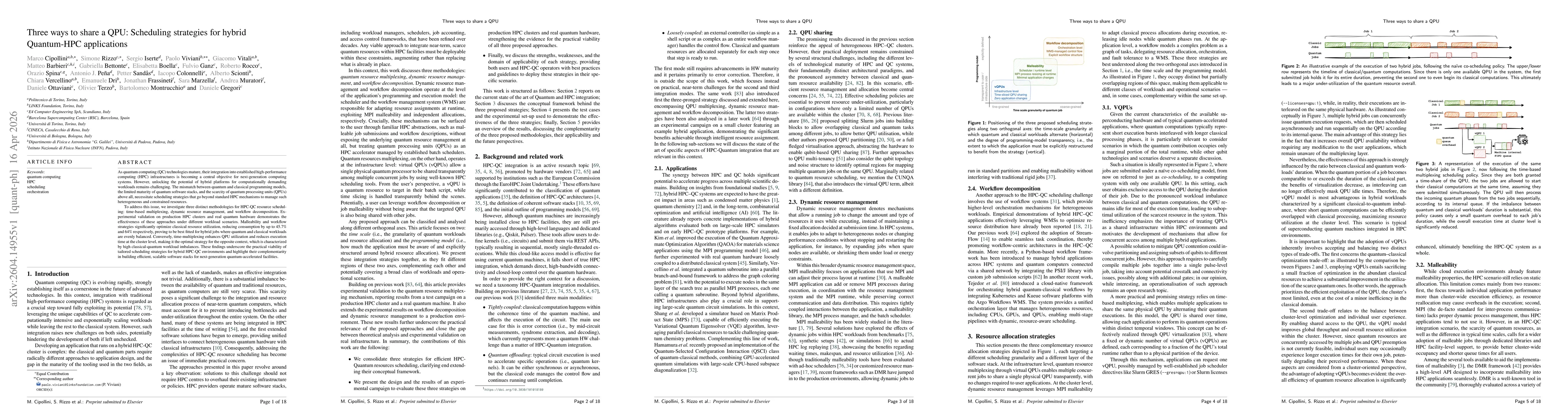

As quantum computing (QC) technologies mature, their integration into established high-performance computing (HPC) infrastructures is becoming a central objective for next-generation computing systems...

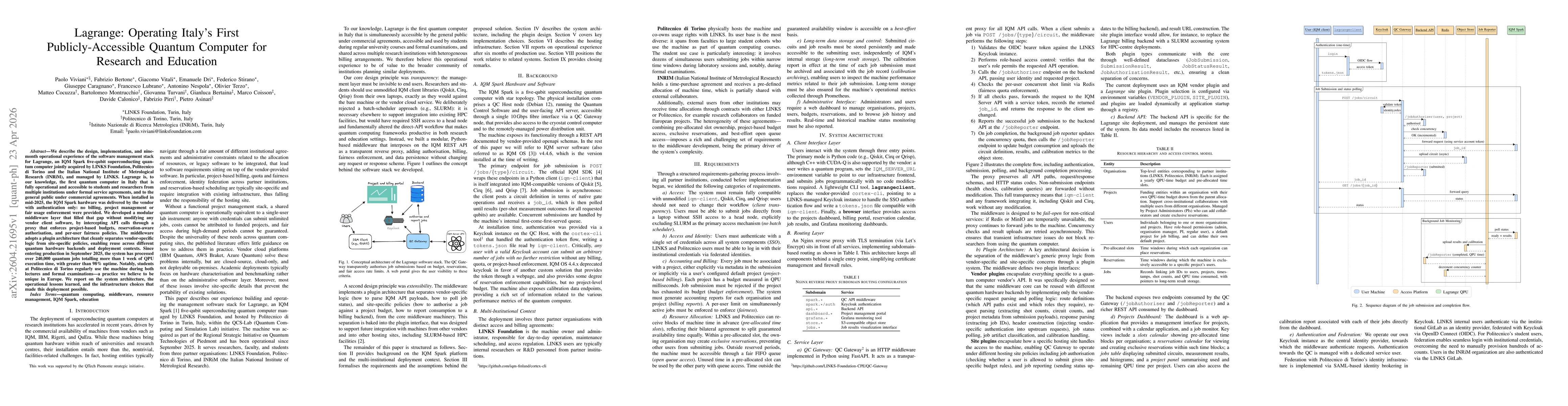

We describe the design, implementation, and nine-month operational experience of the software management stack for Lagrange, an IQM Spark five-qubit superconducting quantum computer jointly acquired b...

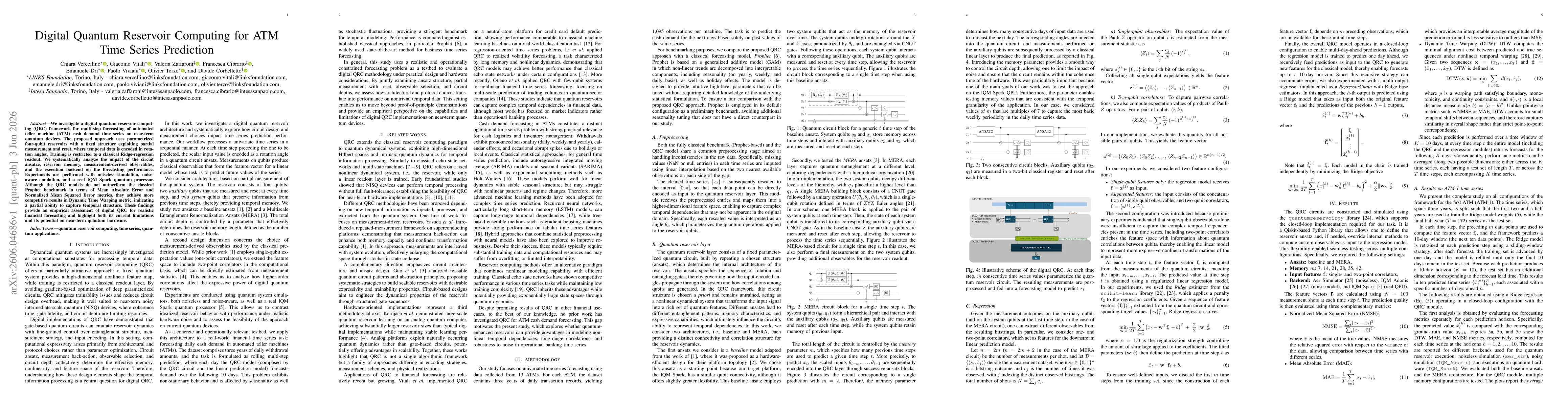

We investigate a digital quantum reservoir computing (QRC) framework for multi-step forecasting of automated teller machine (ATM) cash demand time series on near-term quantum devices. The proposed app...