Academic Profile

Statistics

Similar Authors

Papers on arXiv

Arctic sea ice has steadily diminished as atmospheric greenhouse gas concentrations have increased. Using observed data from 1979 to 2019, we estimate a close contemporaneous linear relationship bet...

We offer retrospective and prospective assessments of the Diebold-Yilmaz connectedness research program, combined with personal recollections of its development. Its centerpiece in many respects is ...

We suggest a new single-equation test for Uncovered Interest Parity (UIP) based on a dynamic regression approach. The method provides consistent and asymptotically efficient parameter estimates, and...

I offer reflections on adaptation to climate change, with emphasis on developing areas.

We use "glide charts" (plots of sequences of root mean squared forecast errors as the target date is approached) to evaluate and compare fixed-target forecasts of Arctic sea ice. We first use them t...

Least squares regression with heteroskedasticity consistent standard errors ("OLS-HC regression") has proved very useful in cross section environments. However, several major difficulties, which are...

Rapidly diminishing Arctic summer sea ice is a strong signal of the pace of global climate change. We provide point, interval, and density forecasts for four measures of Arctic sea ice: area, extent...

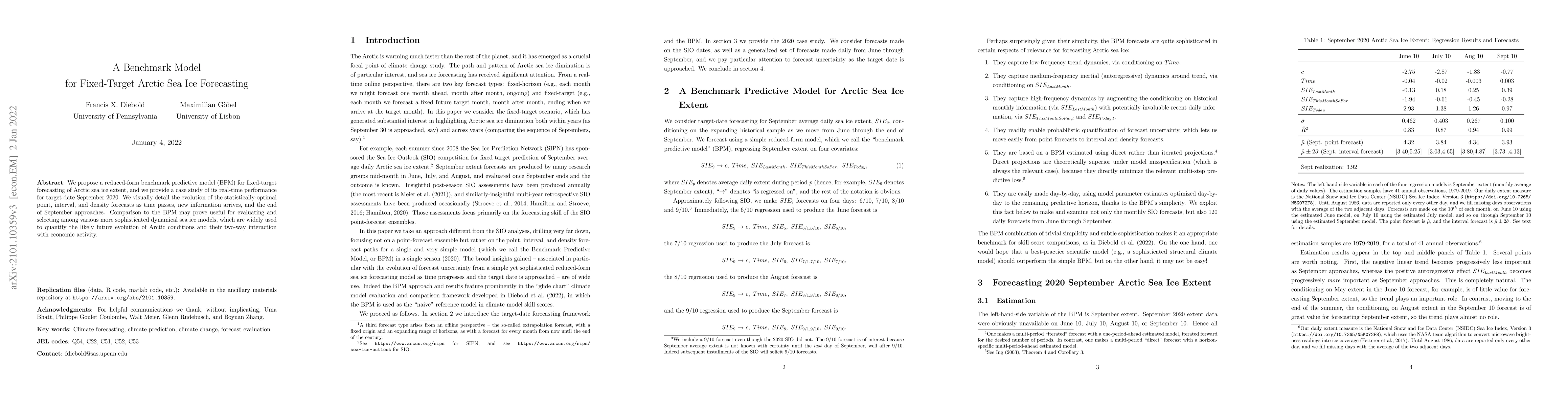

We propose a reduced-form benchmark predictive model (BPM) for fixed-target forecasting of Arctic sea ice extent, and we provide a case study of its real-time performance for target date September 2...

We propose methods for constructing regularized mixtures of density forecasts. We explore a variety of objectives and regularization penalties, and we use them in a substantive exploration of Eurozo...

Against the background of explosive growth in data volume, velocity, and variety, I investigate the origins of the term "Big Data". Its origins are a bit murky and hence intriguing, involving both a...

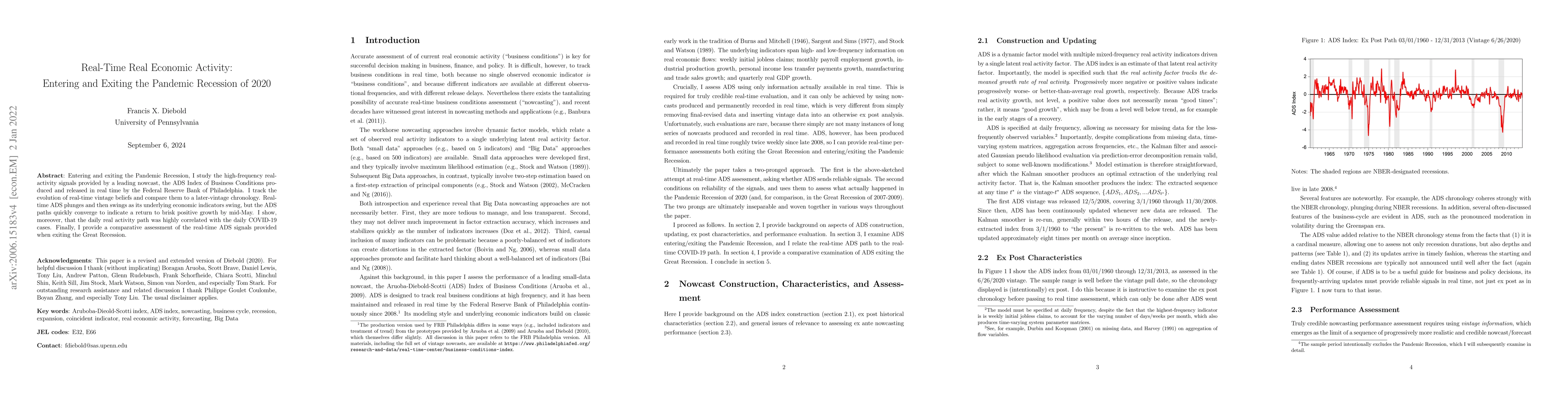

Entering and exiting the Pandemic Recession, I study the high-frequency real-activity signals provided by a leading nowcast, the ADS Index of Business Conditions produced and released in real time b...

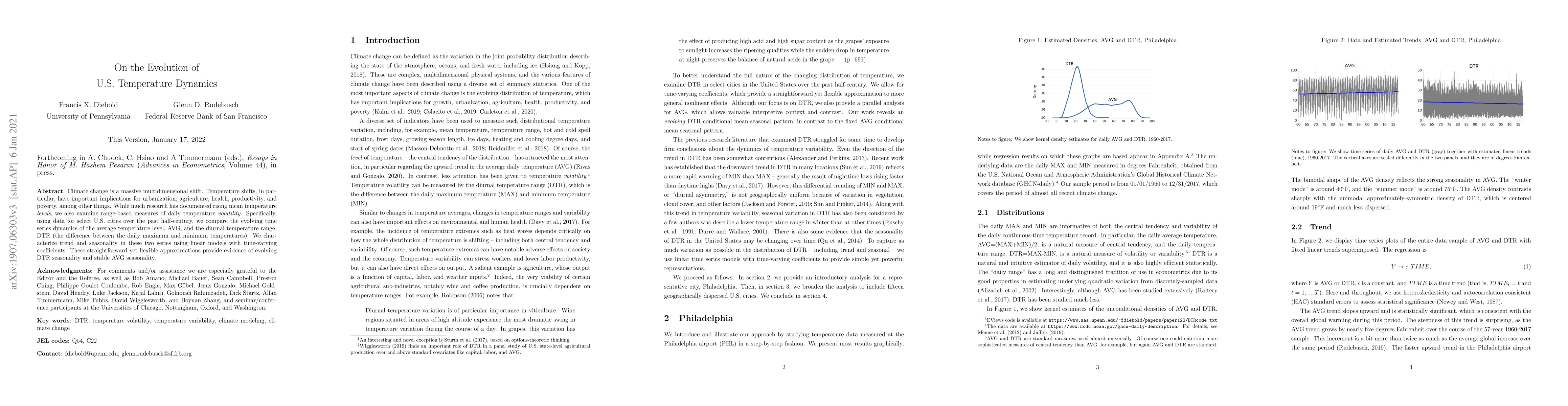

Climate change is a massive multidimensional shift. Temperature shifts, in particular, have important implications for urbanization, agriculture, health, productivity, and poverty, among other thing...

We explore tree-based macroeconomic regime-switching in the context of the dynamic Nelson-Siegel (DNS) yield-curve model. In particular, we customize the tree-growing algorithm to partition macroecono...

Network connections, both across and within markets, are central in countless economic contexts. In recent decades, a large literature has developed and applied flexible methods for measuring network ...

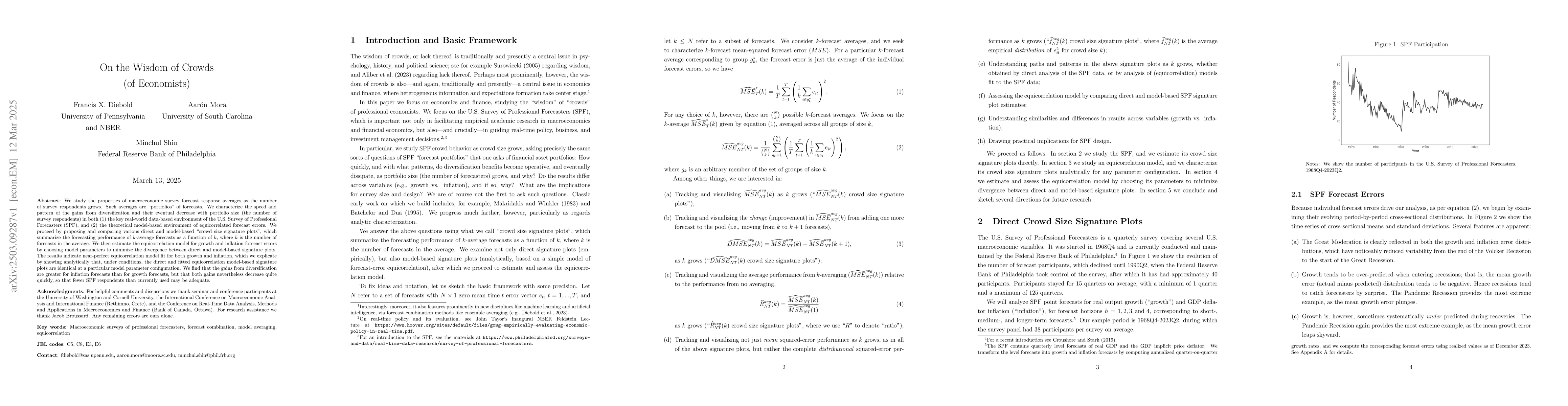

We study the properties of macroeconomic survey forecast response averages as the number of survey respondents grows. Such averages are "portfolios" of forecasts. We characterize the speed and pattern...