Academic Profile

Statistics

Similar Authors

Papers on arXiv

This paper explores and develops alternative statistical representations and estimation approaches for dynamic mortality models. The framework we adopt is to reinterpret popular mortality models suc...

Functional Isolation Forest (FIF) is a recent state-of-the-art Anomaly Detection (AD) algorithm designed for functional data. It relies on a tree partition procedure where an abnormality score is co...

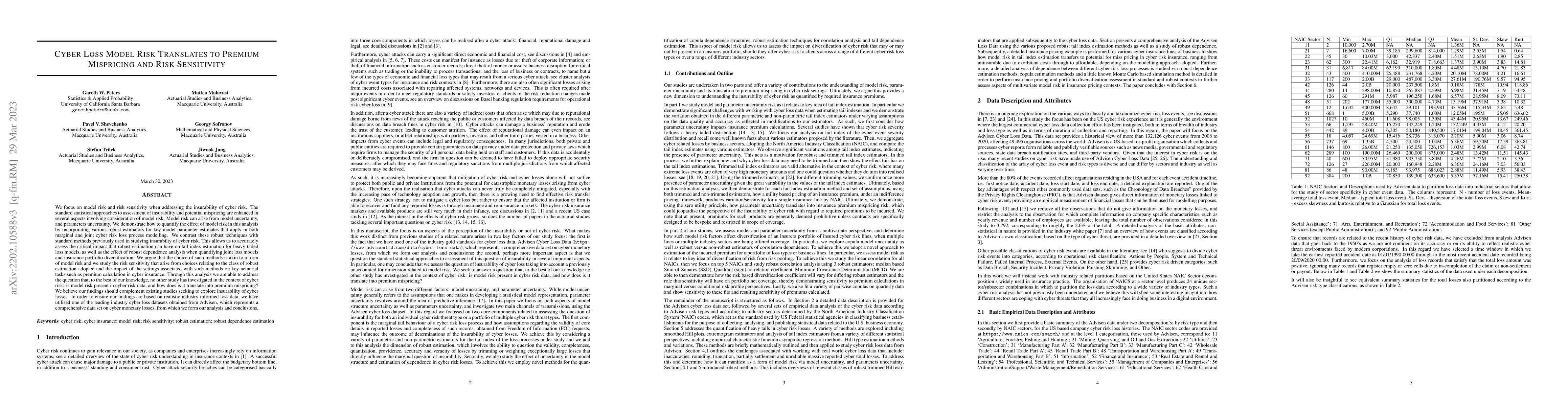

We focus on model risk and risk sensitivity when addressing the insurability of cyber risk. The standard statistical approaches to assessment of insurability and potential mispricing are enhanced in...

In this study we examine the nature of losses from cyber related events across different risk categories and business sectors. Using a leading industry dataset of cyber events, we evaluate the relat...

We develop a novel stochastic valuation and premium calculation principle based on probability measure distortions that are induced by quantile processes in continuous time. Necessary and sufficient...

In this study an exploration of insurance risk transfer is undertaken for the cyber insurance industry in the United States of America, based on the leading industry dataset of cyber events provided...

The cyber risk insurance market is at a nascent stage of its development, even as the magnitude of cyber losses is significant and the rate of cyber loss events is increasing. Existing cyber risk in...

We propose a novel generalisation to the Student-t Probabilistic Principal Component methodology which: (1) accounts for an asymmetric distribution of the observation data; (2) is a framework for gr...

Classification of IoT devices into different types is of paramount importance, from multiple perspectives, including security and privacy aspects. Recent works have explored machine learning techniq...

The statistical quantification of temperature processes for the analysis of urban heat island (UHI) effects and local heat-waves is an increasingly important application domain in smart city dynamic...

We develop a novel approach for the construction of quantile processes governing the stochastic dynamics of quantiles in continuous time. Two classes of quantile diffusions are identified: the first...

We develop a robust data fusion algorithm for field reconstruction of multiple physical phenomena. The contribution of this paper is twofold: First, we demonstrate how multi-spatial fields which can...

Motivated by the need for effectively summarising, modelling, and forecasting the distributional characteristics of intra-daily returns, as well as the recent work on forecasting histogram-valued ti...

Cyber risk classifications are widely used in the modeling of cyber event distributions, yet their effectiveness in out of sample forecasting performance remains underexplored. In this paper, we analy...

In the analysis of commodity futures, it is commonly assumed that futures prices are driven by two latent factors: short-term fluctuations and long-term equilibrium price levels. In this study, we ext...

In stochastic multi-factor commodity models, it is often the case that futures prices are explained by two latent state variables which represent the short and long term stochastic factors. In this wo...

PDSim is an R package that enables users to simulate commodity futures prices using the polynomial diffusion model introduced in Filipovic and Larsson (2016) through both a Shiny web application and R...

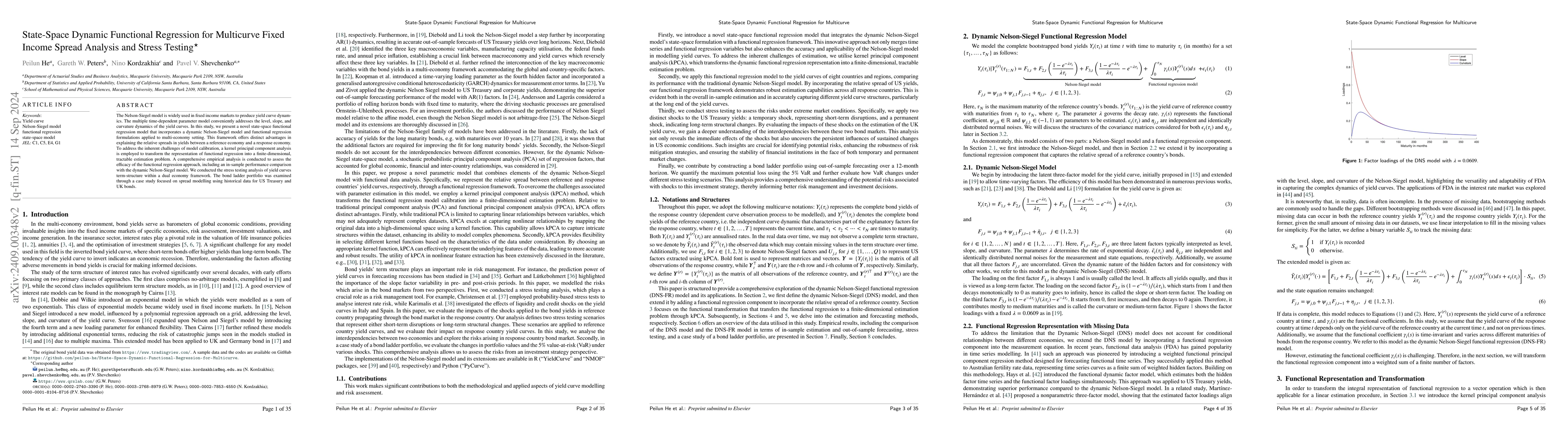

The Nelson-Siegel model is widely used in fixed income markets to produce yield curve dynamics. The multiple time-dependent parameter model conveniently addresses the level, slope, and curvature dynam...

This paper introduces a method for pricing insurance policies using market data. The approach is designed for scenarios in which the insurance company seeks to enter a new market, in our case: pet ins...