Statistics

Similar Authors

Papers on arXiv

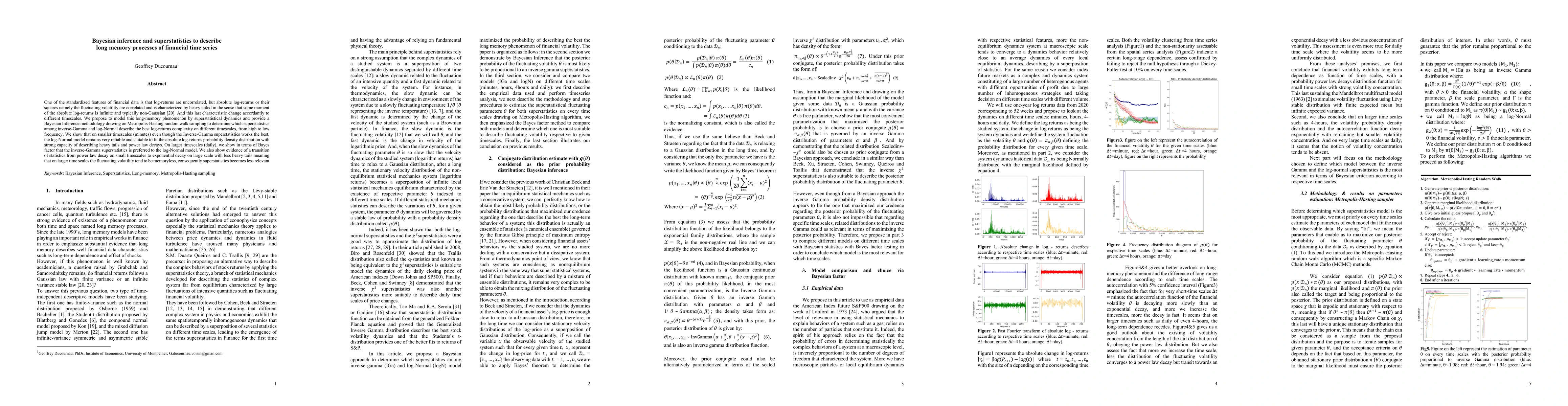

One of the standardized features of financial data is that log-returns are uncorrelated, but absolute log-returns or their squares namely the fluctuating volatility are correlated and is characteriz...

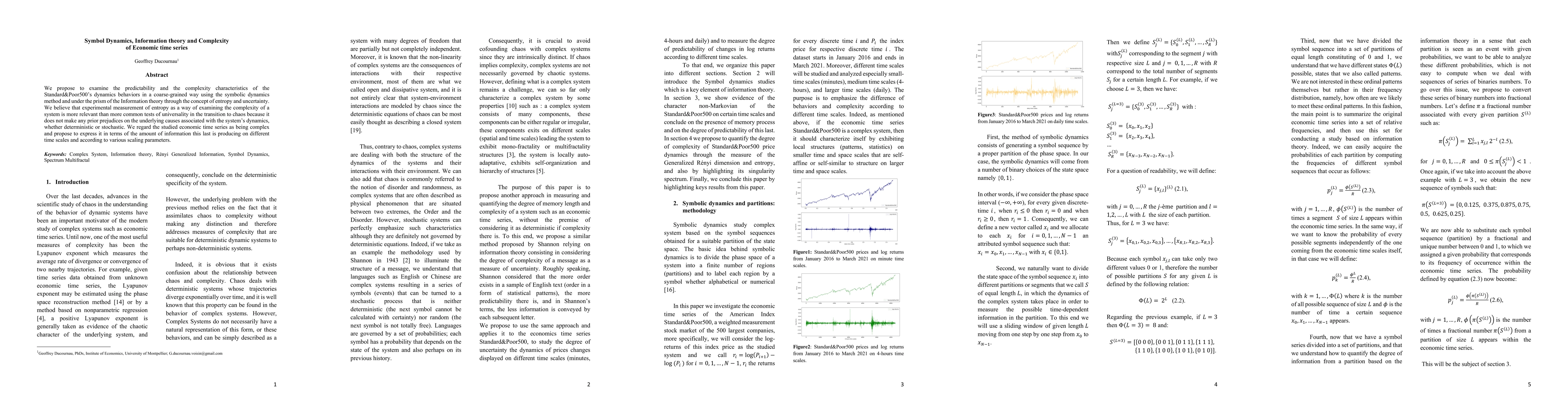

We propose to examine the predictability and the complexity characteristics of the Standard&Poor500 dynamics behaviors in a coarse-grained way using the symbolic dynamics method and under the prism ...

One of the greatest contributors of the 20th century among all academician in the field of statistical finance, M. F. M. Osborne published in 1956 [6] an essential paper and proposed to treat the qu...

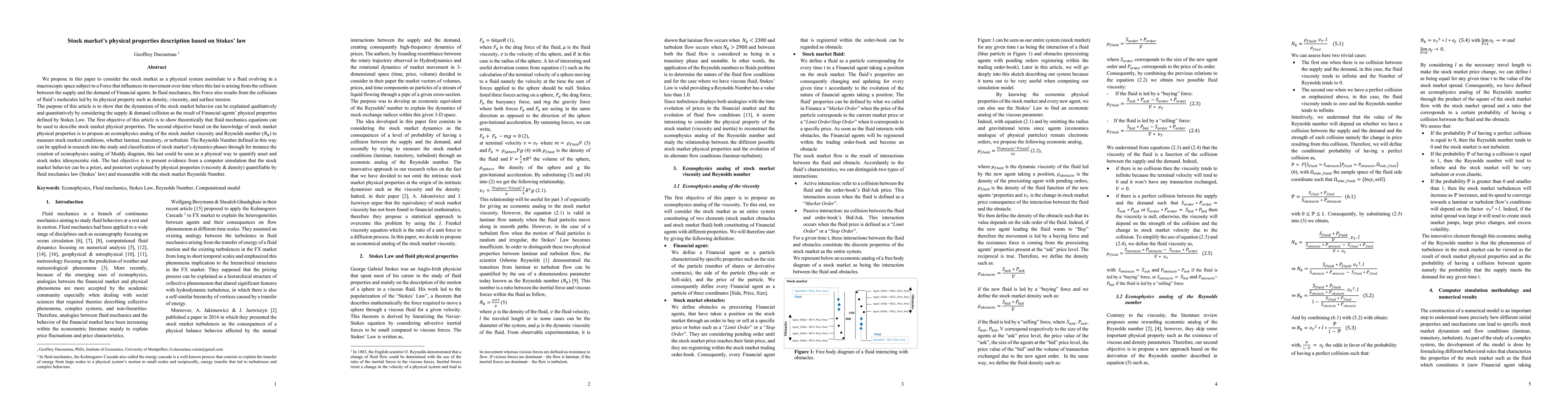

We propose in this paper to consider the stock market as a physical system assimilate to a fluid evolving in a macroscopic space subject to a Force that influences its movement over time where this ...