Academic Profile

Statistics

Similar Authors

Papers on arXiv

We propose and analyze a Multilevel Richardson-Romberg (MLRR) estimator which combines the higher order bias cancellation of the Multistep Richardson-Romberg method introduced in [Pa07] and the vari...

We design a fully implementable scheme to compute the invariant distribution of ergodic McKean-Vlasov SDE satisfying a uniform confluence property. Under natural conditions, we prove various converg...

We investigate propagation of convexity and convex ordering on a typical stochastic optimal control problem, namely the pricing of \q{\emph{Take-or-Pay}} swing option, a financial derivative product...

We investigate the properties of the solutions of scaled Volterra equations (i.e. with an affine mean-reverting drift) in terms of stationarity at both a finite horizon and on the long run. In parti...

In this paper, we are interested in the propagation of convexity by the strong solution to a one-dimensional Brownian stochastic differential equation with coefficients Lipschitz in the spatial vari...

This article is a follow up to Cr\'epey, Frikha, and Louzi (2023), where we introduced a nested stochastic approximation algorithm and its multilevel acceleration for computing the value-at-risk and...

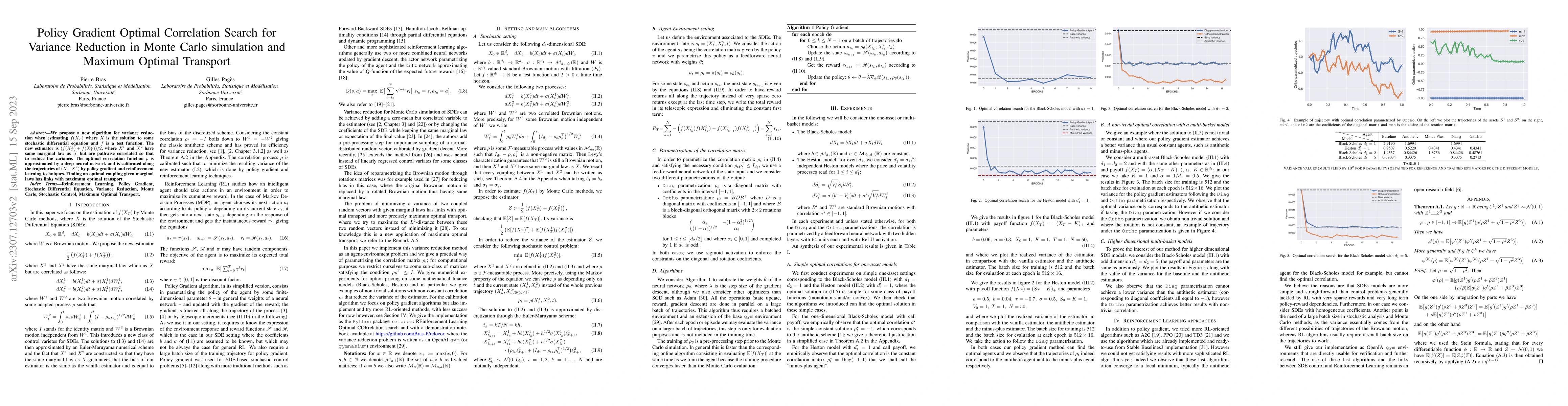

We propose a new algorithm for variance reduction when estimating $f(X_T)$ where $X$ is the solution to some stochastic differential equation and $f$ is a test function. The new estimator is $(f(X^1...

We propose two parametric approaches to evaluate swing contracts with firm constraints. Our objective is to define approximations for the optimal control, which represents the amounts of energy purc...

We propose a new theoretical framework that exploits convolution kernels to transform a Volterra path-dependent (non-Markovian) stochastic process into a standard (Markovian) diffusion process. This...

Stochastic Gradient Descent Langevin Dynamics (SGLD) algorithms, which add noise to the classic gradient descent, are known to improve the training of neural networks in some cases where the neural ...

In this paper, we are interested in comparing solutions to stochastic Volterra equations for the convex order on the space of continuous $\R^d$-valued paths and for the monotonic convex order when $...

We study the convergence of Langevin-Simulated Annealing type algorithms with multiplicative noise, i.e. for $V : \mathbb{R}^d \to \mathbb{R}$ a potential function to minimize, we consider the stoch...

We give bounds for the total variation distance between the solutions to two stochastic differential equations starting at the same point and with close coefficients, which applies in particular to ...

We study the convergence of Langevin-Simulated Annealing type algorithms with multiplicative noise, i.e. for $V : \mathbb{R}^d \to \mathbb{R}$ a potential function to minimize, we consider the stoch...

Fishing quotas are unpleasant but efficient to control the productivity of a fishing site. A popular model has a stochastic differential equation for the biomass on which a stochastic dynamic progra...

We propose a novel approach in the assessment of a random risk variable $X$ by introducing magnitude-propensity risk measures $(m_X,p_X)$. This bivariate measure intends to account for the dual aspe...

We establish upper bounds for the $L^p$-quantization error, p in (1, 2+d), induced by the recursive Markovian quantization of a d-dimensional diffusion discretized via the Euler scheme. We introduce...

In this paper, we establish the monotone convex order between two $\mathbb{R}$-valued McKean-Vlasov processes $X=(X_t)_{t\in [0, T]}$ and $Y=(Y_t)_{t\in [0, T]}$ defined on a filtered probability sp...

Quantization provides a very natural way to preserve the convex order when approximating two ordered probability measures by two finitely supported ones. Indeed, when the convex order dominating ori...

We establish for dual quantization the counterpart of Kieffer's uniqueness result for compactly supported one dimensional probability distributions having a $\log$-concave density (also called stron...

We establish the functional convex order results for two scaled McKean-Vlasov processes $X=(X_{t})_{t\in[0, T]}$ and $Y=(Y_{t})_{t\in[0, T]}$ defined on a filtered probability space $(\Omega, \mathc...

We extend some rate of convergence results of greedy quantization sequences already investigated in arXiv:1409.0732 [math.PR]. We show, for a more general class of distributions satisfying a certain...

This paper proposes two numerical solution based on Product Optimal Quantization for the pricing of Foreign Echange (FX) linked long term Bermudan options e.g. Bermudan Power Reverse Dual Currency o...

We are interested in proposing approximations of a sequence of probability measures in the convex order by finitely supported probability measures still in the convex order. We propose to alternate ...

We propose new weak error bounds and expansion in dimension one for optimal quantization-based cubature formula for different classes of functions, such that piecewise affine functions, Lipschitz co...

This article discusses MLMC estimators with and without weights, applied to nested expectations of the form E [f (E [F (Y, Z)|Y ])]. More precisely, we are interested on the assumptions needed to co...

In this paper, we study the discretization of the ergodic Functional Central Limit Theorem (CLT) established by Bhattacharya (see \cite{Bhattacharya_1982}) which states the following: Given a statio...

We introduce a new class of neural networks designed to be convex functions of their inputs, leveraging the principle that any convex function can be represented as the supremum of the affine function...

Motivated by the study of the propagation of convexity by semi-groups of stochastic differential equations and convex comparison between the distributions of solutions of two such equations, we study ...

In this note, we consider a Stochastic Differential Equation under a strong confluence and Lipschitz continuity assumption of the coefficients. For the unique stationary solution, we study the rate of...

We investigate a class of non-Markovian processes that hold particular relevance in the realm of mathematical finance. This family encompasses path-dependent volatility models, including those pioneer...

In this note we demonstrate that locally optimal functional quantizers for probability distributions on a Banach space lying in the support of $P$ behave exactly like globally optimal functional quant...

In this paper we revisit the exsistence theorem for $L^r$-optimal quantization, $r\ge 2$, with respect to a Bregman divergence: we establish the existence of optimal quantizaers under lighter assumpti...

Estimating risk measures such as large loss probabilities and Value-at-Risk is fundamental in financial risk management and often relies on computationally intensive nested Monte Carlo methods. While ...

This paper provide a comprehensive analysis of the finite and long time behavior of continuous-time non-Markovian dynamical systems, with a focus on the forward Stochastic Volterra Integral Equations(...

True Volterra equations are inherently non stationary and therefore do not admit $\textit{genuine stationary regimes}$ over finite horizons. This motivates the study of the finite-time behavior of the...

This paper investigates the asymptotic behavior of suitably time-modulated Hawkes processes with heavy-tailed kernels in a nearly unstable regime. We show that, under appropriate scaling, both the int...

The aim of this paper is to provide a comprehensive analysis of the path-dependent Stochastic Volterra Integral Equations (SVIEs), in which both the drift and the diffusion coefficients are allowed to...

We establish a Zador like theorem for $L^r$-optimal vector quantization when the similarity measure is a twice differentiable Bregman divergence of a strictly convex function. On our way we also prove...

We establish inequalities that compare the p-Wasserstein distance to distances which are built as suprema of box measures. More precisely, when the measures are supported on $[0,1]^d$, we obtain sharp...

N. Fournier and A. Guillin obtained in their 2015 PTRF paper some bounds of the L^p-mean rate of convergence in Wasserstein distance of empirical distributions for a class of stationary mixing process...