Academic Profile

Statistics

Similar Authors

Papers on arXiv

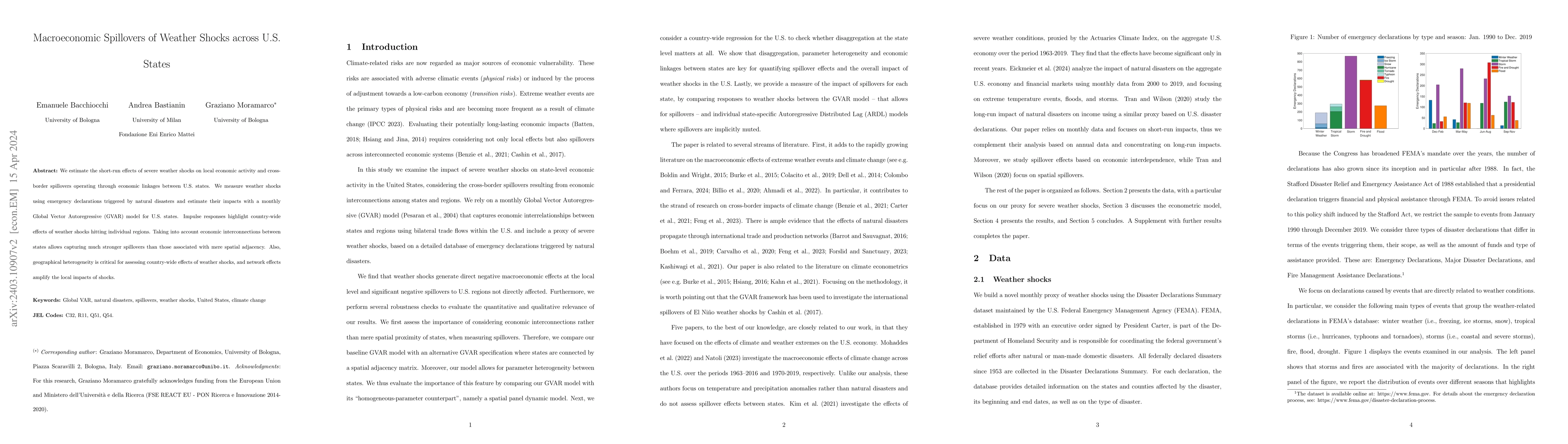

We estimate the short-run effects of severe weather shocks on local economic activity and cross-border spillovers operating through economic linkages between U.S. states. We measure weather shocks u...

We propose a factor network autoregressive (FNAR) model for time series with complex network structures. The coefficients of the model reflect many different types of connections between economic ag...

This paper investigates the transmission of funding liquidity shocks, credit risk shocks and unconventional monetary policy within the Euro area. To this aim, we estimate a financial GVAR model for ...

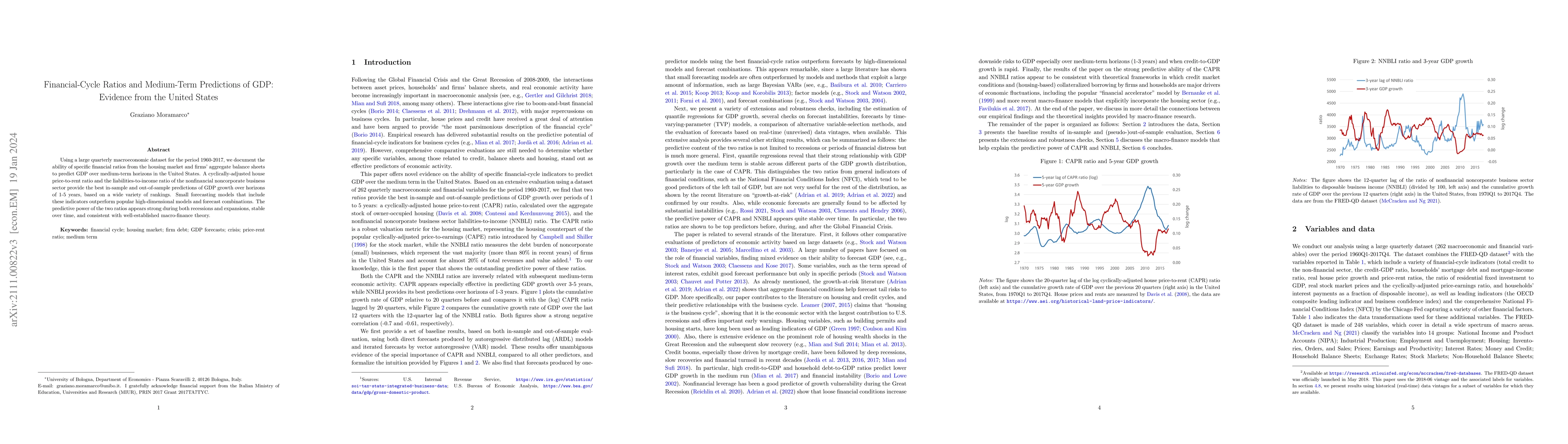

Using a large quarterly macroeconomic dataset for the period 1960-2017, we document the ability of specific financial ratios from the housing market and firms' aggregate balance sheets to predict GD...

We propose an approach for generating macroeconomic density forecasts that incorporate information on multiple scenarios defined by experts. We adopt a regime-switching framework in which sets of sc...